By A Correspondent

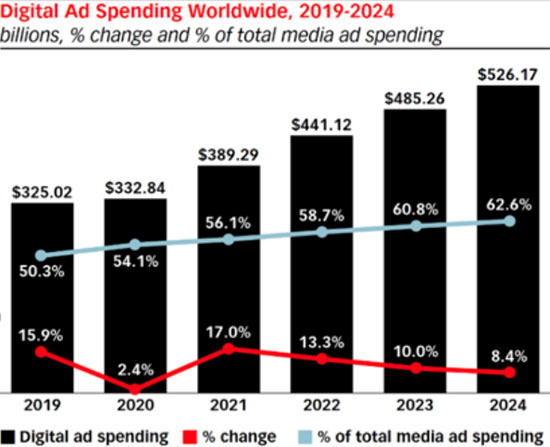

According to PwC’s Global Entertainment & Media Outlook 2020-2024, the Indian M&E industry’s long-term outlook remains robust as it is expected to grow at 10.1% CAGR to reach 55 billion USD by 2024. A K-shaped bifurcated recovery is on the horizon in which sectors like OTT, internet advertising, video/games/e-sports, and music and podcasts are expected to spearhead growth in the industry. Globally, Digital revenue is expected to contribute 60% to the total E&M revenue by 2020, alone.

In terms of individual segment market size as a percentage of total E&M revenue, OTT video in India is expected to see the largest gain and reach 5.2% by 2024, closely followed by internet advertising. Segments like advertising and those dependent on physical locations are likely to be further impacted in a negative manner whereas digital E&M spending will increasingly be regarded as a non-discretionary expense. While globally, newspapers and magazines are dropping the free online model and starting to ask readers to pay for quality content online, digital paywalls are yet to become commonplace in India. Furthermore, while India will remain the world’s biggest cinema market in admission terms, cinema revenue in India will contract at a -2.6% CAGR to total US$1.5bn over the next 5 years.

Said Rajib Basu, Partner & Leader – Entertainment & Media, PwC India: “We find ourselves in extraordinary times, and the pandemic has accelerated ongoing shifts in consumers’ behaviour, pulling forward digital disruption and reaching industry tipping points that wouldn’t otherwise have been reached in the next few years. Our research shows that India will be the fastest growing entertainment and media market globally in terms of pure consumer revenue. Coming out of Covid-19, a K-shaped bifurcated recovery is expected in which some sectors rise while others fall. Over the next five years, the outlook remains highly positive for digital led segments such as OTT, Internet Advertising, Online Gaming and Music & Podcasts that were perfectly positioned to meet consumers where they are in 2020 – predominantly at home and online,” adding: “However, companies simultaneously have to prepare to meet them where they will be two years from now. They will need to build and maintain direct-to-consumer relationships, offer enough differentiation or scale to compete, and unlock greater value using the right technologies. This is a unique window of opportunity for E&M businesses to transform and make themselves more resilient and relevant for the future.”

Top 4 segments to advance rapidly:

1. OTT Video: India holds the most potential of any market in the world and its breakneck rate of growth will see total OTT video revenue overtake South Korea, Germany and Australia to jump to being the sixth-largest market in 2024. Subscription video on demand will be the prime driver of revenue, increasing at a 30.7% CAGR from US$708mn in 2019 to US$2.7bn in 2024. OTT video growth is coming from both inside and outside the home as Internet-connected devices proliferate as the new ‘at-home’ environment has led to the rise of direct-to-consumer apps, local ‘bite-sized’ entertainment platforms and user-generated content (UGC) formats

2. Internet Advertising: India is now the sixth-largest Internet advertising market in the Asia Pacific region. Mobile will be the primary driver of revenue in the Internet advertising market revenue due to increased data affordability, new mobile-first formats, ability to measure, and strategic targeting. Nonetheless, from a global perspective, Internet advertising in India remains underdeveloped and has massive headroom for growth

3. Video, Games & E-sports: Gaming and e-sports are capitalizing on the need to bring live experiences into the home in more personalized and more engaging ways. E-sports represented less than 1% of overall market in 2019, but has become one of the fastest growing segments today with a projected 33% CAGR by 2024. However, despite surging growth and enormous potential, the sector tackles with the biggest challenge of low levels of app monetisation

4. Music, Radio & Podcasts: Podcast industry was already experiencing rapid growth prior to the COVID-19 outbreak. Fuelled by the uptake of music-streaming brands, the overall space is expected to grow at a 13.5% CAGR, to total revenue of nearly US$1.7bn in 2024. India will also see strong increase at a 30.4% CAGR in its monthly podcast listener base over the next five years, supported by entry of foreign players and original content on topics including news, society and culture

As the industry navigates into the post-pandemic world, one can witness new opportunities for capturing growth:

> Players bolster subscription offerings – With consumers increasingly paying a monthly fee to access a library of entertainment content, such as films, music, content, fitness etc., media and entertainment industry players are catching on to the value of subscription based models to bring in business. Optimising revenue mix or pricing models to emerge more resilient and capture a bigger share of the wallet will be the focus

> Physical events look for digital alternatives – Another opportunity made more compelling by the pandemic is bringing live experiences into the home in a more personalized and engaging manner. Digital spaces—e-commerce platforms, virtual event spaces, gaming channels, podcasts—are evolving into powerful new platforms for marketing. Creating new content propositions will help realise new revenue streams

> OTT will thrive in 2020 as cinema and traditional TV degrow – OTT sector will directly benefit from the closure of cinemas, as some film studios choose to fast-track new releases to home video platforms. Since OTT platforms offer convenience and accessibility to consumers who are likely to hold on to their new habits of streaming ‘at home’, global SVOD revenue may overtake box office spend very soon

> Landmark acquisitions are out; buying growth and cash flows are in. – As companies look for ways to navigate barriers, strategic investments & alliances in search of scale and growth will be crucial to determine success in the E&M media industry

The last few weeks have seen eruption of a fresh debate around television ratings. Before the formation of BARC India, ratings-related controversies in the TAM era were frequent, and different broadcasters, at different times, expressed their discontentment privately and publically, with some like NDTV even taking the legal route. When the currency shifted to BARC India in 2015, these debates expectedly became less frequent. The key difference, of course, was that BARC India is an industry body, and not a private organisation like TAM.

The last few weeks have seen eruption of a fresh debate around television ratings. Before the formation of BARC India, ratings-related controversies in the TAM era were frequent, and different broadcasters, at different times, expressed their discontentment privately and publically, with some like NDTV even taking the legal route. When the currency shifted to BARC India in 2015, these debates expectedly became less frequent. The key difference, of course, was that BARC India is an industry body, and not a private organisation like TAM.

Yes, there’s another OTT app. Kolkata-based Mojoplex promises a “renaissance in the industry”. Along with movies, web series and short films, viewers will also be served stand-Up comedy, travel and adventure vlogs and music jamming sessions. Inhouse production will start in December 2020.

Yes, there’s another OTT app. Kolkata-based Mojoplex promises a “renaissance in the industry”. Along with movies, web series and short films, viewers will also be served stand-Up comedy, travel and adventure vlogs and music jamming sessions. Inhouse production will start in December 2020.

Ever since IPL 13 began on September 19, 2020 with a massive 20 crore viewers on Star India Network and Disney + Hotstar, the tournament has been delivering high ratings on TV and OTT platforms.

Ever since IPL 13 began on September 19, 2020 with a massive 20 crore viewers on Star India Network and Disney + Hotstar, the tournament has been delivering high ratings on TV and OTT platforms.

On Friday, October 9 SonyLIV will unveil ‘Scam 1992 – The Harshad Mehta Story’, an original around the stockmarket operator Harshad Mehta and the securities scandal of the early 1990s.

On Friday, October 9 SonyLIV will unveil ‘Scam 1992 – The Harshad Mehta Story’, an original around the stockmarket operator Harshad Mehta and the securities scandal of the early 1990s.