By Our Staff

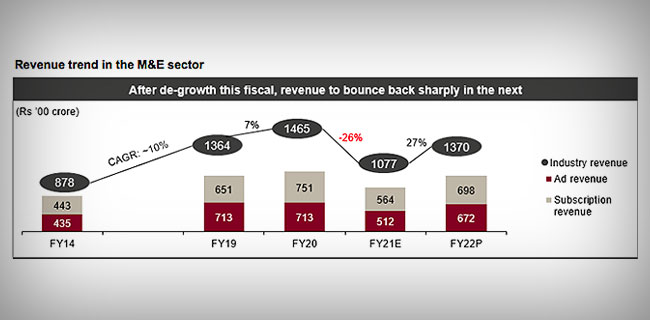

Revenue of India’s media and entertainment (M&E) sector should script a strong 27% rebound to ~Rs 1.37 lakh crore in fiscal 2022, after contracting ~26% this fiscal. Optically, the de-growth this fiscal and growth expectation next fiscal may sum up to a full rebound. But that won’t be true because the 27% growth will be on a much lower base. Industry revenue next fiscal will still be lower than that in fiscal 2020 (refer to Chart above).

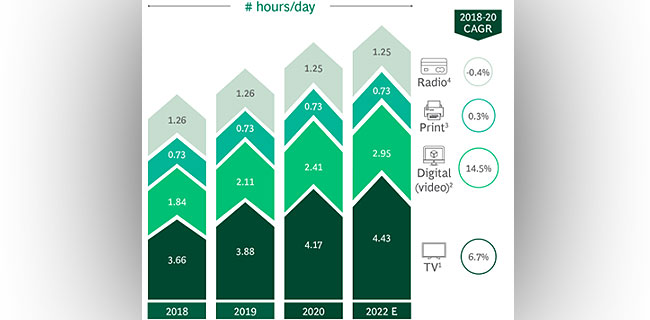

The time to bounce-back to pre-pandemic levels will be relatively shorter for segments such as digital and television (TV), while print, films, outdoor, and radio would take longer

Credit profiles of large media companies would be unaffected due to strong balance sheets, liquidity and the revenue rebound, while mid-sized and small ones could see stress, an analysis of over 80 of them rated by Crisil Ratings shows.

Said Nitesh Jain, Director, Crisil qually to the overall M&E sector’s topline, but since the former correlates strongly with economic growth, the pandemic has had a bigger impact on it. Next fiscal, with strong economic rebound on the cards, ad revenue should grow 31% on-year and subscription revenue ~24%.”

The TV segment – contributing around half of the sector’s topline – has recovered fully and will report healthy growth next fiscal. Ad revenue saw a sharp contraction initially, but recovered swiftly thereafter, aided by airing of new content, sports events such as the Indian Premier League and a buoyant festive season.

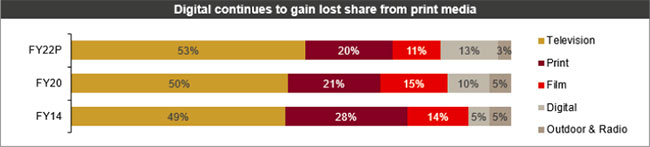

As for subscriptions, TV was resilient even during the peak of pandemic as people remained indoors. The print segment – contributing a fifth of the M&E sector topline – is recovering, though at a much slower pace, and should be able to rebound fully only by the end of next fiscal. Print is losing share in ad revenue mainly to the digital segment (refer to chart 2. Circulation too, especially for English language, could see a loss of 8-10%, because of increased preference for e-papers in metros.

However, print companies are rebooting their cost structure and accelerating digital adoption to stay relevant. Films – contributing a sixth to the sector topline – is one of the most impacted segment. But occupancies in theatres should improve with the vaccination rollout and a strong pipeline of content. However, this segment is likely to remain impacted even next fiscal due to social distancing norms and fear of closed spaces.

Other traditional media – radio and outdoor – are seeing persisting pain, and will likely take much longer to recover (Radio and outdoor segments don’t have any subscription revenue). This is because commuting as well as ad budgets for micro, small and medium enterprises – the key drivers for these segments – will remain restricted even in fiscal 2022.

Added Rakshit Kachhal, Associate Director, Crisil Ratings Ltd: “Digital has emerged as the medium of choice. The pandemic accelerated adoption of over-the-top (OTT) platforms, online gaming, e-commerce, e-learning, e-papers and online news platforms. This has meant the focus of advertisers has shifted from traditional to digital media. We expect the digital segment revenue to grow 14-16% annually over the medium term. Its share of M&E sector revenue is expected to double to ~20% by fiscal 2024 compared with last fiscal.”

Given the sharp impact on revenue, cash accruals this fiscal will weaken for all M&E companies except TV distributors. Credit profiles of the large companies are cushioned by strong balance sheets (with most of them net debt-free), while those of small and mid-sized media companies have weakened. More downgrades among the latter led to the Crisil Ratings’ credit ratio (upgrades to downgrades) for the sector sliding to 0.33 in the first nine months of the current fiscal from 0.75 in fiscal 2020.

Liquidity pressure may intensify for them if recovery in ad revenue is delayed. That said, there is a silver lining to this cloud, too. M&E companies have adopted aggressive cost rationalisation initiatives. Besides, the pandemic-led change in consumer behaviour has accelerated monetisation opportunities for these players through integration of digital media into their traditional businesses. Some of these aspects can lead to structural changes in business models of the M&E sector over the longer term.

Simplification is always tempting, and generally a good thing too. But increasingly, the world around us is showing a tendency to over-simplify narratives. With attention spans reducing, nuance is becoming an elusive idea too. And a direct offshoot of this socio-political trend is the emergence of false binaries: a debate that’s framed as either-or, with no room in the middle.

Simplification is always tempting, and generally a good thing too. But increasingly, the world around us is showing a tendency to over-simplify narratives. With attention spans reducing, nuance is becoming an elusive idea too. And a direct offshoot of this socio-political trend is the emergence of false binaries: a debate that’s framed as either-or, with no room in the middle. Bigg Boss, India’s biggest reality show, will first air on Voot, not the GEC where it’s grown into the phenomenon that it has been.

Bigg Boss, India’s biggest reality show, will first air on Voot, not the GEC where it’s grown into the phenomenon that it has been.

Explaining the content strategy behind Bigg Boss OTT, Manisha Sharma, Chief Content Officer, Hindi Mass Entertainment, Viacom18, said: “Bigg Boss, over the years, has grown to become a phenomenon that drives conversations across the country. With the launch of Bigg Boss OTT, our digital audiences are in for a treat. The new digital exclusive format will take the show’s fandom to its next level through active engagement with viewers being able to play a part in the show’s progress. The beauty of this show lies in the versatility of format and the massive popularity it commands – both aspects helping us in customizing the show as two different content offerings for the two different platforms while maintaining its core ethos.”

Explaining the content strategy behind Bigg Boss OTT, Manisha Sharma, Chief Content Officer, Hindi Mass Entertainment, Viacom18, said: “Bigg Boss, over the years, has grown to become a phenomenon that drives conversations across the country. With the launch of Bigg Boss OTT, our digital audiences are in for a treat. The new digital exclusive format will take the show’s fandom to its next level through active engagement with viewers being able to play a part in the show’s progress. The beauty of this show lies in the versatility of format and the massive popularity it commands – both aspects helping us in customizing the show as two different content offerings for the two different platforms while maintaining its core ethos.”

On February 25, 2021, the Electronics and Information Technology ministry notified the Information Technology (Intermediary Guidelines and Digital Media Ethics Code) Rules, 2021 for news publishers and OTT platforms giving a three-month deadline to websites to comply with the same.

On February 25, 2021, the Electronics and Information Technology ministry notified the Information Technology (Intermediary Guidelines and Digital Media Ethics Code) Rules, 2021 for news publishers and OTT platforms giving a three-month deadline to websites to comply with the same.

The devastating second wave of Covid-19 in India has brought with it various lockdowns, being managed by the various state governments individually. A direct impact of lockdown-like restrictions is the inability to produce video content, such as TV shows and films. In any case, the fear of the second wave is real and palpable, and many actors and technicians are wary of being on sets. The much-touted IPL bio-bubble bursting last week does not inspire confidence either.

The devastating second wave of Covid-19 in India has brought with it various lockdowns, being managed by the various state governments individually. A direct impact of lockdown-like restrictions is the inability to produce video content, such as TV shows and films. In any case, the fear of the second wave is real and palpable, and many actors and technicians are wary of being on sets. The much-touted IPL bio-bubble bursting last week does not inspire confidence either.