By Indrani Sen

The recent TAM Axis report on TV advertising trends in India in 2018 published in ET Brand Equity (https://brandequity.economictimes.indiatimes.com/slide-shows/tv-advertising-at-a-glance-tam-report/68096082) on February 22, 2019 shows that contrary to the popular belief TV advertising revenue did not suffer in 2017 after introduction of GST. Demonetisation in 2016 was a big blow which crippled the growth rate, but the advertising revenue was back on its growth track in 2017 which accelerated in 2018.

Indexed growth rate of TV ad revenue 2014-2018: Source TAM Axis (AdEx India)

N.B. The number of channels covered by AdEx is shown under each year in the green line.

The above table shows that from 2014 to 2015 the index rose by 16 points and after adding only 1 point in 2016, it jumped by another 16 points in 2017 followed by 20 points in 2018. Over the last five years, from 2014 to 2018 there has been an overall growth of 53% in TV advertising revenue.

Top 10 sectors in TV advertising in 2018:Â Source TAM Axis (AdEx India)

The Top 10 sectors and the Top 5 sectors respectively account for 81% and 61% of total TV advertising revenue in 2018. While the Top 2 sectors retained their positions, household products rose from rank 7 to rank 5 with 43% growth in TV advertising in 2018 over 2017. Hair Care and Auto ranked lower in 2018 as compared to 2017 while Laundry, Personal Accessories and Durables held on to their ranks.

It is interesting to note that of the Top 10 categories, 3 (Toilet Soap, Tooth Paste & Perfume /Deodorant) belong to Personal Care/ Personal Hygiene sector; 2 (Washing Powder/ Liquids & Toilet/ Floor Cleaner) belong to Household Product sector; 2 (Milk Beverages & Chocolates) belong to Food & Beverage sector; 2 (Two Wheeler and Cars/ Jeeps) belong to Auto sector and 1 (Shampoo) belongs to Hair Care sector. Though Services and Personal Healthcare hold the 3rd and 4th ranks among the top 10 sectors, no category from the two sectors feature in the list of top 10 categories which collectively account for more than 25% of the total TV advertising revenue.

Top Ten advertisers accounted for 30% while top 50 advertisers accounted for 56% of the total TV advertising revenue in 2918. Hindustan Unilever topped the list with 10% share, followed by Reckitt Benckiser (India) and ITC who rose from 8th rank in 2017 to 3rd rank in 2018. Wipro and Amazon Online were new entrants among top 10 advertisers in 2018.

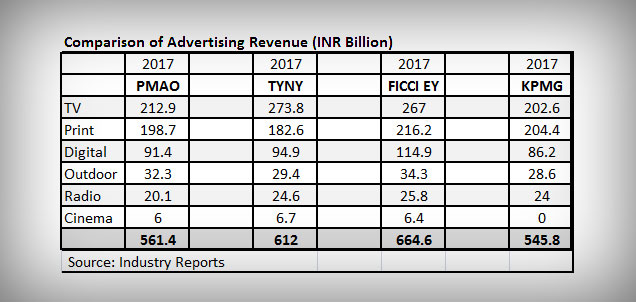

The 2017-18 Annual Report of the Telecom Regulatory Authority of India (TRAI), published last week, indicates that the subscription revenues accounted for 59.5% of the overall TV industry revenue as it rose from Rs 38,7007 crore in 2016-17 to Rs 39,3007 crore in 2017-18. The report quoted the FICCI-EY Report 2018 which indicated that TV advertising revenues rose from Rs 20,1007 crore in 2016-17 to Rs 26,7007 crore in 2017-18, at a much higher rate of 32.8Â per cent than reflected in the analysis of TAM Adex data for 2018, albeit referring to a different time period.

Regardless of different reports based on different time periods, it is a reality that with close to 200 million TV households and 836 million TV viewers In India (Source: BARC Establishment Survey 2018), the Indian advertisers will continue to invest in TV medium for reaching out to the masses. The detailed analysis of TV AdEx data of 2018 by TAM Axis seems to indicate that Indian TV advertising revenue is all set for a roller coaster ride in 2019.

By Indrani Sen

By Indrani Sen