By Indrani Sen

During the last two or three weeks, we saw many reports on how the AdEx has improved in June 2020 ensuring us that not only digital, but TV and print are also on the path of recovery after Covid-19. TAM AdEx for June has shown that TV advertising volumes increased by 74 per cent per day in June compared to April, when adspends declined sharply due to decline in demand during the nationwide lockdown. TV ad volumes saw 46% growth in June compared to May.

During the last two or three weeks, we saw many reports on how the AdEx has improved in June 2020 ensuring us that not only digital, but TV and print are also on the path of recovery after Covid-19. TAM AdEx for June has shown that TV advertising volumes increased by 74 per cent per day in June compared to April, when adspends declined sharply due to decline in demand during the nationwide lockdown. TV ad volumes saw 46% growth in June compared to May.

Print, which suffered a bigger hit in terms of revenue due to distribution problems during lockdown, has recorded a higher increase of 325% in average ad volume per day in June 2020 when compared to April 2020. Most of the business newspapers and industry websites reported on the recovery of digital and TV media. None of the articles highlighted the comparison between the first quarter and the second quarter of 2020 which could have given a better idea about the recovery of ad volumes in digital and TV media.

I saw only one article in details on Print AdEx on the recovery of Print AdEx which also did not have any such comparison (https://www.financialexpress.com/brandwagon/print-advertising-on-the-road-to-recovery-as-average-ad-volumes-per-day-rose-325-in-june-2020-tam-adex/2032701/). This trend of lack of reporting on print clearly indicates that the medium has lost its position to digital not just in terms of share of the advertising pie, but also in the share of mind map of the audience, the advertisers and agencies.

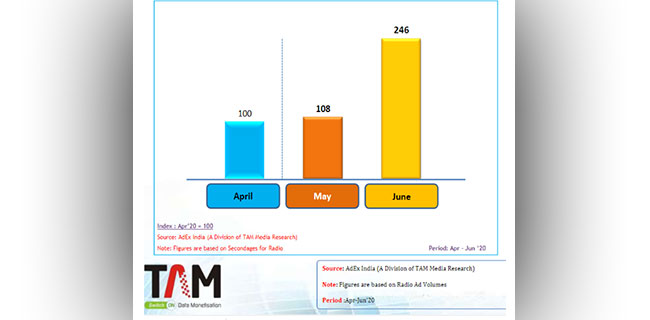

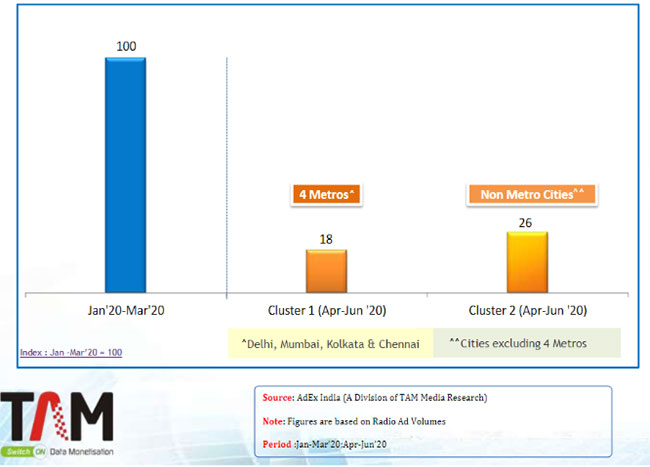

The Advertising Report on Radio – April-June 2020 published by TAM shows that average ad volume per day increased by more than two-fold in June compared to April and May. However, a comparison with the first quarter of the year (Jan-March) shows that the ad volumes in radio are still much below the pre-Covid-19 phase. It is interesting to note that FM Radio ad volumes in Non-metro cities have recovered better than metro cities.

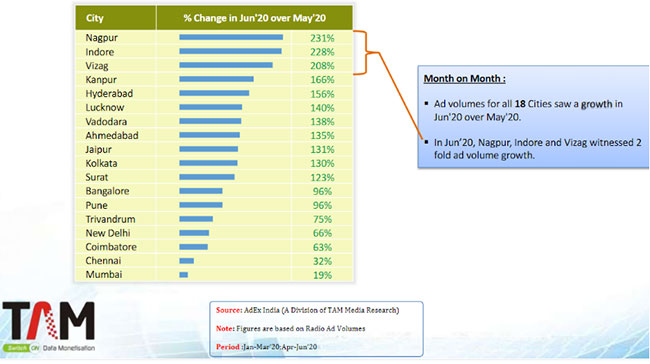

The ad volumes of radio advertising in all 18 cities grew in June 2020 over May 2020. The chat below shows that the eight non-metro cities, Nagpur, Indore, Vizag, Kanpur, Hyderabad, Lucknow, Vadodara and Ahmedabad have shown much better growth in June 2020 compared the four metro cities. Kanpur, Indore and Vizag led the chart with each accounting for two-fold growth in ad volumes. Among the four metro cities, Kolkata has shown the highest percentage change in June 2020 over May 2020 with Mumbai showing the least percentage change. The listenership of FM radio increased during the period of lockdown and has retained the level, but advertisers across different cities are investing in the medium in different way.

The report has detail analysis of radio advertising by categories, advertisers and brands as well as city wise analysis of the performance of radio AdEx. It also presents comparative analysis of TV and radio and digital and radio advertising during Jan-June 2020. The Top 10 common categories, advertisers and brands between TV and radio shows that during the first six months of 2020, Top 10 common categories, advertisers and brands added 33%, 14% and 4% on TV while they added 10%, 7% and 4% on radio. Similarly, the Top 10 common categories, advertisers and brands between digital and radio shows that during the first six months of 2020, Top 10 common categories, advertisers and brands added 47%, 18% and 12% on digital while they added 19%, 2% and 1% on radio. The role of radio in the media mix needs to be reassessed by advertisers and agencies for the growth and survival of the FM radio industry during this period of unlocking and subsequent return to normalcy.