By Indrani Sen

Over the last couple of months, we have seen many surveys which have looked at the current level of global and local media revenue and its recovery path over the next two to three years. Most of these surveys have highlighted the bright picture looming at the end of the tunnel. Last week, I came across a survey released by www.emarketer.com which has focussed on three key media trends sweeping the pandemic hit world, providing the advertising and media industry with deep insights.

Over the last couple of months, we have seen many surveys which have looked at the current level of global and local media revenue and its recovery path over the next two to three years. Most of these surveys have highlighted the bright picture looming at the end of the tunnel. Last week, I came across a survey released by www.emarketer.com which has focussed on three key media trends sweeping the pandemic hit world, providing the advertising and media industry with deep insights.

On October 23, 2020 eMarketer released Global Media Intelligence Report for 2020, produced in collaboration with Starcom and GlobalWebIndex covering 42 major markets in the world with a focus on internet users’ engagement with digital and traditional media.

The first trend observed in the study indicates that ownership of PCs and tablets are declining in many countries including India. “Between H1 2019 and H1 2020, ownership of desktops, laptops, and/or tablets declined most sharply in developing markets, including Brazil, China, Egypt, and India—all countries where the focus has long been on mobile devices and services. But the same trend appeared to a lesser degree in several other countries too, including France, Russia, Sweden, and the US.” This trend indicates that smartphones are consolidating their position as the primary screen across the pandemic hit world both in the developed as well as in the developing countries among the internet users. (https://www.emarketer.com/content/3-key-trends-shaping-media-landscape-this-year?ecid=NL1009)

We already know that in India mobile phones are playing a crucial role in spreading digital media communication with more and more mobile-first internet users coming to the market. This study shows that while there has been hardly any change in the ownership of smartphones from HI2019 to H12020 as it is already near saturation level, the time spend on the device has gone up marginally. “96.0% of internet users ages 16 to 64 owned a smartphone in H1 2020—a figure unchanged since H1 2019. In addition, one in 10 respondents had a feature phone. Time spent with mobile devices averaged 3 hours, 37 minutes (3:37) per day, 1 minute more than in 2019.” Compared to 2019 the ownership percentage of PCs and tablets have come down from 72% to 54.2%, showing a significant decline. Comparatively, ownership of tablets was less affected with only a drop from 24.5% to 22.3%. Time spent by Indians with their PCs and tablets declined sharply from by 45 minutes per day (https://www.emarketer.com/content/global-media-intelligence-2020-india).

The second trend emphasises on digital video which continues to close its gap with broadcast TV. In the western countries the share of internet users watching free or paid for digital video have already surpassed the share watching live TV or are almost equal to it. In India, it will take a longer time for a similar trend to set in, but the warning signs should not be ignored by the TV channels who have not yet invested in OTT business.

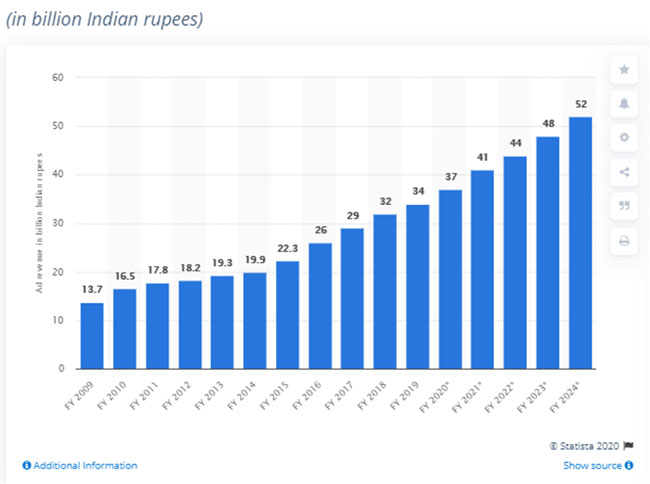

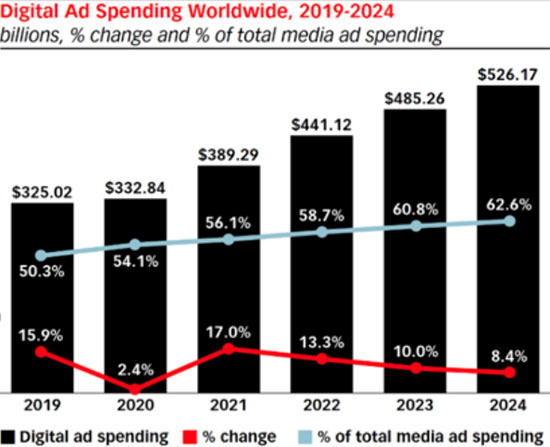

Based on the various trend of digital media consumption among the internet users, the study predicts that by 2024, digital ad spending worldwide will become $526.17 billion and will account for 62.6% of the total media ad spending. The growth rate of digital ad spend will fall sharply during 2020, but will rise equally sharply in 2021. Over 2022 to 2024. The growth rate of digital ad spending is expected to fall gradually, but its share in the total media ad revenue will continue to grow year on year as shown in the chart below.

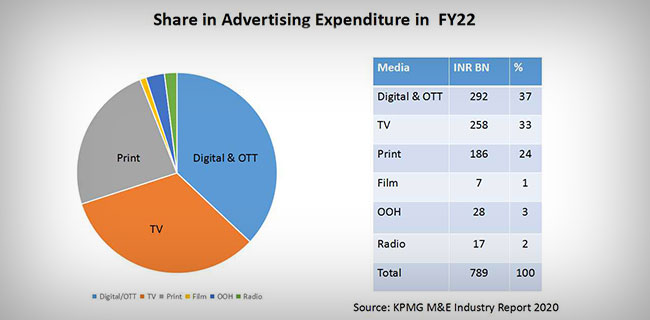

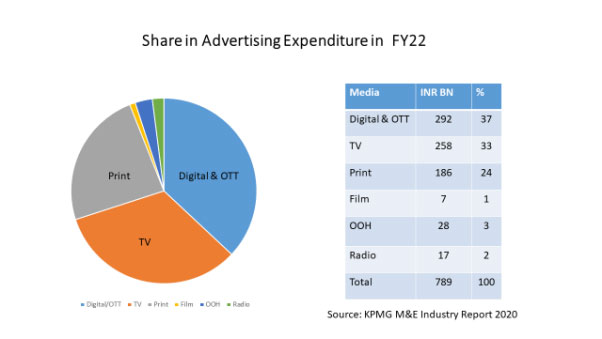

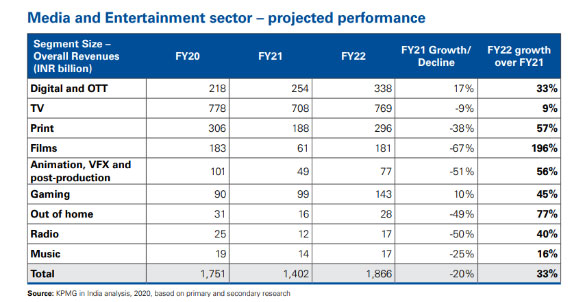

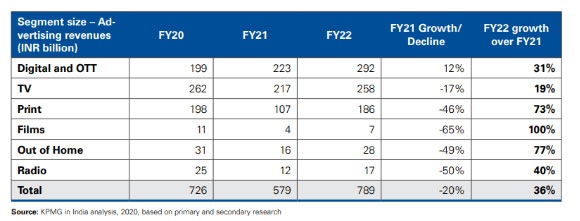

In India, it will take many years before the digital ad spending crosses 50% of the total media ad spending. However, as shown in the recently published M&E industry Report 20202 by KPMG, the trend of ad spending on digital and OTT crossing the ad spending on TV media, is expected to set in by FY 2022 (https://www.mxmindia.com/2020/10/the-great-churning-of-the-media-cauldron/).

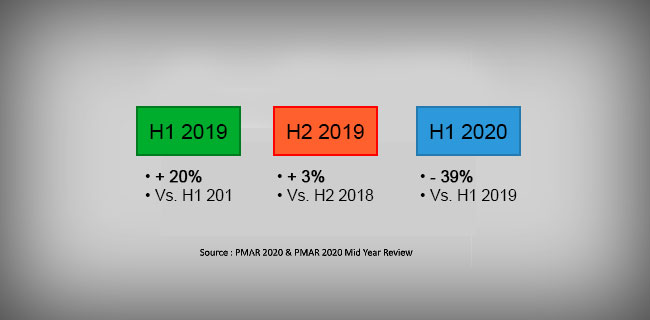

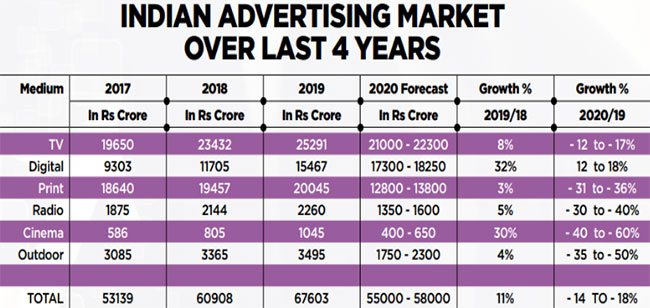

The third trend observed in the study indicates that the pandemic is probably hastening the decline of print media: “Print audiences aren’t shrinking everywhere, but print newspapers and magazines did register many of the most dramatic decreases in media engagement this year.” In India, traditional print industry seems to be in a buoyant and positive mood during the current festive season. Some large newspaper houses have also posted good growth during the third quarter of 2020. But, the Pitch Madison Advertising Midyear Review 2020 released in August, 2020 estimated a loss of 31% to 36% in print ad expenditure from 2019 to 2020 (https://www.mxmindia.com/2020/08/dramatic-changes-in-indian-ad-industry/). Only time will tell if COVID 19 will hasten the process of decline of the print media in India.

Earlier this year, DK published his autobiography “Life Unstoppable: Making Challenges Work for you” with Adite Banerjee as an e-book on Amazon. The link is available on his website www.dkbose.com. The introduction on the back cover says: “Bose’s story is an inspiring tale of grit and determination, rejection and success. In narrating his life’s journey, the social communication strategist and behaviour change mentor goes beyond the tried and tested route of offering ‘success strategies’ but shares his own learnings and reveals how challenges can be made to work for you.” Young aspirants in advertising and social marketing must read this book for invaluable learnings.

Earlier this year, DK published his autobiography “Life Unstoppable: Making Challenges Work for you” with Adite Banerjee as an e-book on Amazon. The link is available on his website www.dkbose.com. The introduction on the back cover says: “Bose’s story is an inspiring tale of grit and determination, rejection and success. In narrating his life’s journey, the social communication strategist and behaviour change mentor goes beyond the tried and tested route of offering ‘success strategies’ but shares his own learnings and reveals how challenges can be made to work for you.” Young aspirants in advertising and social marketing must read this book for invaluable learnings.