By Indrani Sen

The second wave of the pandemic is spreading all across the country and we are seeing state after state imposing various restrictions like night or weekend curfews, conditional lockdowns etc. The central government has decided not to impose a nationwide lockdown like last year which paralysed the entire Indian economy. The decision to impose restrictions for curbing the spread of the second wave has been left to the state governments. As the pandemic situation stands now in the second month of the April-June quarter, our economy is likely to see a contraction in this quarter which will have a cascading effect on M&E industry as advertisers will spend less on promoting their products and brands.

The second wave of the pandemic is spreading all across the country and we are seeing state after state imposing various restrictions like night or weekend curfews, conditional lockdowns etc. The central government has decided not to impose a nationwide lockdown like last year which paralysed the entire Indian economy. The decision to impose restrictions for curbing the spread of the second wave has been left to the state governments. As the pandemic situation stands now in the second month of the April-June quarter, our economy is likely to see a contraction in this quarter which will have a cascading effect on M&E industry as advertisers will spend less on promoting their products and brands.

Till now, most economists have predicted that the effect of the second wave of COVID 19 will be less on India Inc. than the effects of the first wave when we had a national lockdown for 70 days. However, it is too early to be assured about that prediction. The outbreak of Covid-19 is no longer concentrated in urban areas, it has been spreading virulently across villages, particularly in the Hindi hinterland of Uttarakhand, UP, MP, Bihar and Chhattisgarh. The rural areas of other states, particularly the states which recently held Assembly elections, are also experiencing a surge of the pandemic.

Urban India contributes to 60%-65% of the sales of FMCG companies while rural India accounts for the balance 35% to 40. In certain FMCG categories the share of urban and rural is 50%: 50% or even tilted a bit more to the rural sector. Last year, when the lockdown had affected the sales of FMCG industry in urban areas due to restricted consumer spends, Bharat or Rural India spurred the growth of FMCG companies. An article published on February 28, 2021 in www.livemint.com said: “To be sure, companies are betting on large swathes of consumers in rural India switching from unbranded, loose products to branded ones over the next few years. This gives them room to push their soaps, shampoos, biscuits, beverages and packaged staples in India’s villages, albeit at lower price points. Demand in rural markets has outstripped sales growth witnessed by companies in urban markets over the last several quarters. Companies expect India’s smaller cities and villages to continue driving growth.” (https://www.livemint.com/companies/news/why-are-fmcg-majors-chasing-growth-in-rural-india-11614504243913.html). At the beginning of 2021, most economic analysts expected the momentum of sales in rural areas to continue. However, the ground realities have already turned out to be different which will affect not just the sales of FMCG products in rural areas, but also the production of Argo industries.

The controversies over vaccination between the Centre and the states coupled with shortage of oxygen supply and inadequate health infrastructure have given a different dimension to the Covid-19 crisis induced by the second wave. Middle class urban families are spending their live savings, begging and borrowing to try and save their near and dear ones, in the process reducing their subsequent purchasing power. Upper class affluent urban families have realised suddenly that the big fat medical insurance in which they invested are not of any use to them if they cannot get their relatives admitted to any hospital or nursing home. Many insurance companies are refusing to give coverage for Covid treatment. These rich people are feeling the need of having large amount of cash in hand for emergency treatment of Covid, which will reduce their disposable income and affect the sales of consumer durables.

The pandemic has already managed to disrupt our cricket calendar by postponing the IPL 2021 indefinitely to another venue in another country and it is unlikely that T20 World Cup will be held in India in 2021 which has affected the tourism and hospitality industry, the on-ground display, etc. The advertisers having peak season during summer months are putting a brake on their TV expenditures due to state level lockdowns, restricted movement of transport for delivering of goods and reduction in consumer spends due to very small windows of time available for daily shopping.

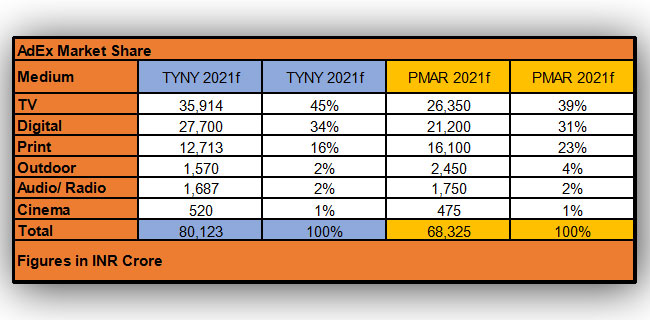

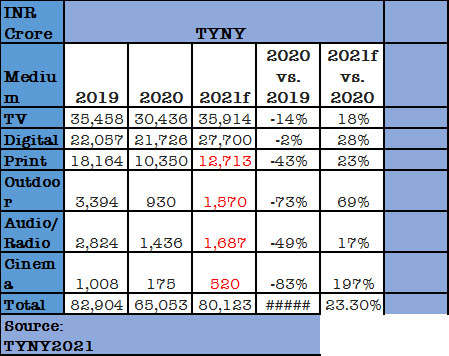

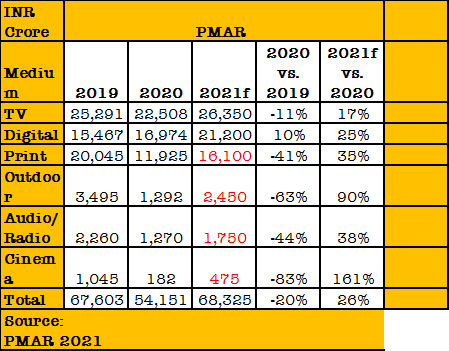

Medical experts are predicting a third wave of the pandemic around September, 2021 which may result in further contraction of the economy in the October-December quarters, in spite of the festive season. Lack of economic recovery in the next two quarters will result in further loss of business for the M&E industry. As per the Pitch Madison Advertising Report 2021, overall AdEx de-grew by 20% and traditional media AdEx degrew by 29% in 2020 with only digital media growing by 10% during the same period. The PMAR 2021 predicted that in 2021 overall AdEx will grow by 26% touching the 2019 level. In the second month of the second quarter of 2021, it is too early to predict the overall effect of Covid-19 on the M&E industry over the entire year. The current signs indicate that it will be difficult for the AdEx to jump back to the 2019 level in 2021.