By Indrani Sen

Indian Pay TV market is highly fragmented due to the multi-lingual distribution of TV content through many regional distributors along with national distributors covering the HSM and all major regional markets. As per different available research, 50% + share of the subscribers of Pay TV are currently being held by several small regional players. None of the available estimates except the FICCI EY reports takes into account the subscribers of DD Free Dish while estimating the total TV households in India. DD Free Dish subscribers do not have to pay for the TV content so do not contribute to the pay TV market revenue.

Indian Pay TV market is highly fragmented due to the multi-lingual distribution of TV content through many regional distributors along with national distributors covering the HSM and all major regional markets. As per different available research, 50% + share of the subscribers of Pay TV are currently being held by several small regional players. None of the available estimates except the FICCI EY reports takes into account the subscribers of DD Free Dish while estimating the total TV households in India. DD Free Dish subscribers do not have to pay for the TV content so do not contribute to the pay TV market revenue.

Media Partners Asia (MPA) has recently published a report titled “Indian Pay TV Distribution 2021” which predicts that by 2025, the Indian Pay TV industry will reach revenue of USD 12.3 billion and total Pay TV subscribers will increase to 134 million in 2025 from 127 million in 2020. According to the same research, DTH homes in India will grow from 58 million in 2020 to 68 million in 2025 at the cost of the cable TV homes during the same period. Compared to estimates published by various other research organisations, the total pay TV subscribers’ base in India seem to have been underestimated while the revenue may have been overestimated by MPA.

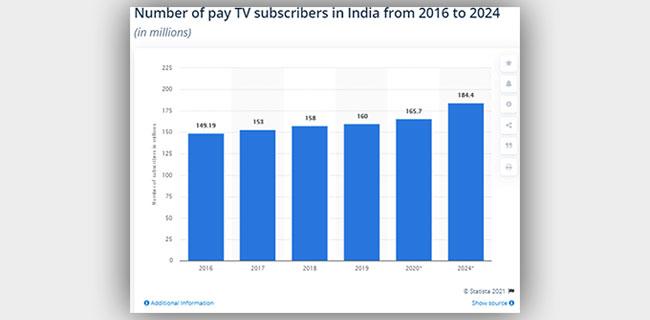

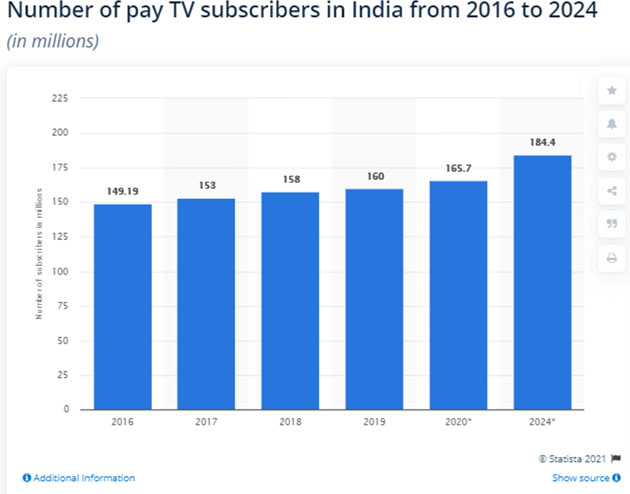

According to an estimate published by Statista Research Department on March 19, 2021, “India had over 160 million subscribers of pay TV in the year 2019. This figure was around 149 million subscribers in 2016 and was estimated to go up to over 184 million Pay TV subscribers by 2024.” These estimates are higher than the estimates made by the FICCI EY in their report on the Indian M&E industry 2020.

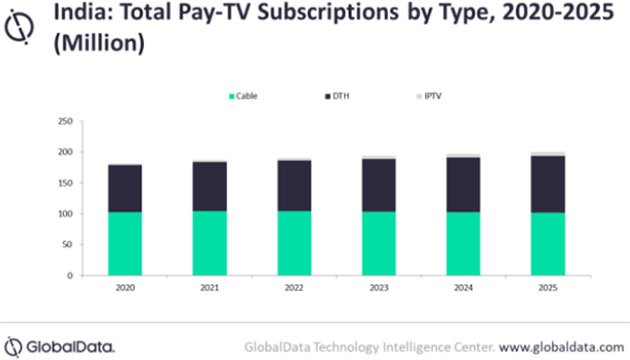

Another report India Telecom Operators Country Intelligence report published by www.globaldata.com in 2020 supports the estimates of Statista. As per this report, Cable will be the leading Pay TV technology in India throughout the forecast period, followed by DTH with a small presence IPTV which is expected to grow in India at a very fast rate during the next 4 years. As per www.globaldata.com the total Pay TV revenue in India is expected to grow at an annual growth rate (CAGR) of 0.7 percent from USD 3.19 billion in 2020 to USD 3.30 billion in 2025, which is much lower than the FICCI EY estimates.

The above picture reflects the trends in TV distribution by technology in the global market, though the pandemic has reduced the share of the cable TV subscribers in India. IPTV is expected to grow at a CAGR of 19.4% in India during the next 4 years riding on the fixed broadband penetration in India as well as smart TV sets.

According to the report published in www.grandviewresearch.com: “The global Pay TV market size was valued at USD 225.9 billion in 2019, registering a CAGR of more than 1.5% from 2020 to 2027.” This report spoke about the growth in penetration of Pay TV in rural households in China, India and Indonesia creating overall growth in the Pay TV industry.

Source: FICCI EY Indian M&E Industry Report 2020

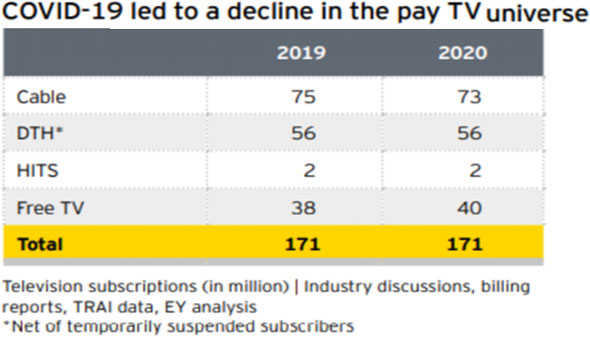

As per the FICCI EY report on the Indian M&E industry 2020, there are 171 million TV households in India of which 40 million are Free TV households. The report estimates distribution revenue of the Indian TV Industry to reach INR 502 billion (USD 6.72 billion) in 2023 from the current level of INR 434 billion (USD 5.80 billion). The FICCI EY estimates seem to be the best one available currently for the size as well as the revenue of the Pay TV market in India.