By A Correspondent

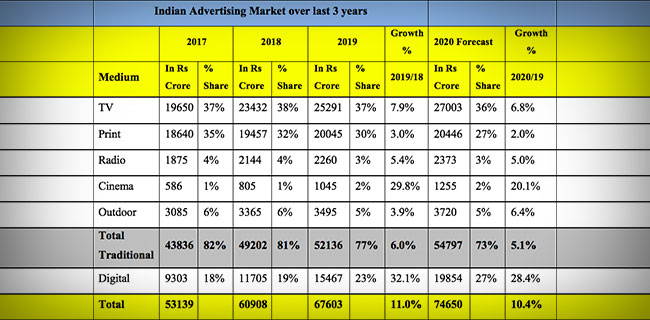

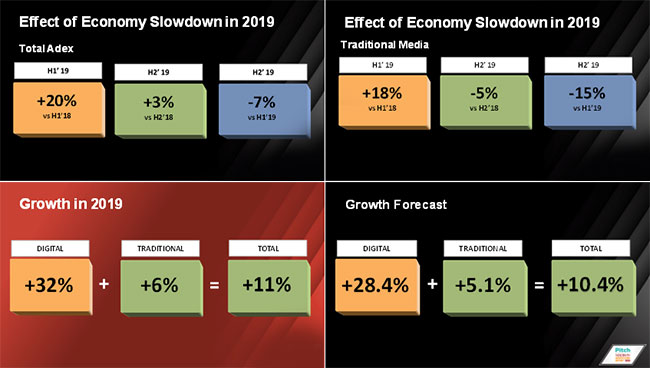

The annual Pitch Madison Advertising Report 2020 was released on Thursday in Mumbai with the message that didn’t need much spelling out: traditional media grew only 6% in 2019 and actually degrew in the third and further quarter. The forecast for growth in 2020 is down to 5.1%. But digital media is galloping ahead. It grew 32 in 2019, and the forecast for 2020 is 28.4%.

Said Sam Balsara, Chairman, Madison World: “Whilst 2019 has been a tumultuous year for AdEx, I believe Adex will grow dramatically over the next five years given that we are one of the larger growing economies of the world and already growing at twice the rate of global AdEx (11% vs 5.4%). Despite this India’s contribution to global AdEx is under 2%, which is bound to go up. Advertisers need to experiment more with media and do things differently to harness the power of media for Brands.”

Key findings of the report:

A. Overall:

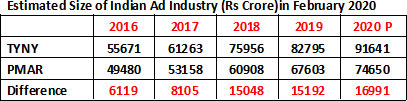

1) In absolute terms, AdEx has grown from Rs. 60,908 crore to Rs. 67,603 crores, an addition of 6,695 crores or 11%. This makes it the 2ndhighest addition to AdEx in a single year in the entire last decade.

2) The growth rate of 11% in 2019 is lower than the PMAR mid-year projection of 13.4% and last year’s growth of 15%.

3) 56% of this growth has been contributed by Digital, which has expectedly grown by as much as 32%. Traditional media has grown by mere 6%

4) TV still continues to be the largest contributor to AdEx with 37.4% share, followed by Print at 29.7%, Digital at 22.9%. Outdoor at 5.2%, Radio at 3.3% and Cinema at 1.5%. All mediums except Digital and Cinema have lost share.

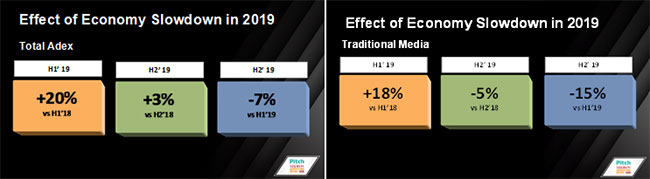

5) A quarter-wise analysis shows that unlike in most years, when Quarter 4 shows a blip because of the festive season, this year Quarter 2 showed a blip on the back of IPL, World Cup and General Elections and in fact Quarter 3 and Quarter 4 show a de-growth of 3% and 7% respectively.

B. TV:

1) After a rocking 2018 when TV AdEx grew by 19%, TV grew by only 8% in 2019.

2) TV lost 1% share point and its share in the total AdEx stands at 37%, demonstrating that it is vulnerable.

3) FMCG continues to rule the roost in TV AdEx, contributing 49% although its contribution came down by 1% share point in 2019. Telecom and Auto follow with 12% and 7% contribution respectively. Ecommerce category also gained dramatically during the year by as much as 20% and has reached Rs. 1,320 crore.

4) The main categories that have fueled the overall growth of Rs. 1,860 crore in 2019 is FMCG (Rs. 740 crore), Telecom (275 crore) and Ecommerce (Rs. 220 crore). Predictably contribution of the Auto sector to the overall growth is negative in 2019 at -4%.

5) There is a marginal decline in total FCT that has been telecast in 2019, perhaps because of disappearance of the FTA channels, unlike in most previous years when FCT has gone up year on year.

6) In terms of revenue, Sports genre has grown the highest by as much as 47% and Hindi GEC by about 7%, which leads us to conclude that despite a soft market, these two genres have been able to command a rate increase.

C. Print

1) Print grew by 3% in 2019, lower than PMAR’s mid-year projected rate of 5%. Whilst this is the 3rdconsecutive year Print has grown less than 5%, it continues to be the 2nd highest contributor after TV with a share of 30%.

2) Print share in AdEx has gone down from 42% in 2011 to 30% today.

3) FMCG, Auto, Education, Real Estate and Retail continue to be the main cash cows and contributed almost 50% to Adex in 2019. Ecommerce is fast emerging as an important category for Print and grew 14%, over 2018. Political Parties are estimated to have contributed Rs. 200 crore on account of Lok Sabha Elections.

4) Nearly 65% of Print’s growth of Rs. 588 crore is accounted for by 4 categories – Education, Ecommerce, Real Estate and Retail.

5) In terms of volume there is a 3% decline in 2019. Hindi publications continue to maintain the lead over English Publications, contributing 35% followed by English at a distant 25%.

D. Digital

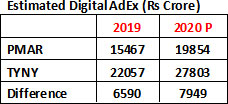

1) Digital Adex made impressive gains during the year and achieved a growth rate of 32.1% in 2019, the highest growth achieved by any medium in the year taking Digital AdEx to Rs. 15,467 crore.

2) Digital has grown at a compound annual growth rate of more than 30% over last 5 years and now contributes 23% of AdEx, an increase of 4% share points over last year.

3) Search, Social, Video & Display have all equally contributed to the growth of Digital AdEx, with each contributing between 20% to 30% to the total.

4) Consumption of video is going up year on year and in 2019 video spends grew by as much as 59% beating the Digital AdEx growth of 32%. Almost all of Digital AdEx (94%) is on mobile.

5) 52% of Digital AdEx came from “classical advertising” ie display banners (22%) and online video (30%).

6) If we were to combine TV+ Online Video, TV growth of 8% would increase to 16%.

E. Forecast

1. The PMAR Forecast for 2020 for AdEx is muted. In arriving at the projected growth figure for the whole year at 10.4%, the report is guided by the expectation that the economy should bounce back in the 2ndhalf of 2020 as indicated in the government’s Economic Survey published on January 31, 2020. PMAR therefore sees a subdued H1 for AdEx and a buoyant H2, specially Q4.

2. We also expect a wide variation of growth rates across mediums with Digital medium leading the growth at 28.4% and ending the year with 27% share of AdEx at Rs. 19,854 to be precise.

3. TV will continue to be the largest medium with a 36% share of AdEx, but will have a subdued growth rate of 6.8%.

4. Print will lose 3 percentage points in terms of share of AdEx and end up with a 27% share registering a 2% growth.

5. Radio and Outdoor are expected to grow at 5% and 6% respectively and maintain their share at 3% and 5%.

6. Cinema, amongst traditional media should grow at a high growth rate of 20.1% taking its spend to Rs. 1255 crore.

As per the Pitch Madison Advertising Report, in 2020 adspends in India are predicted to grow by 10.4%, while GroupM’s This Year Next Year predicts that in 2020 the same will grow by 10.9%. This rate of growth is the only aspect on which both the reports have shown some similarity.

As per the Pitch Madison Advertising Report, in 2020 adspends in India are predicted to grow by 10.4%, while GroupM’s This Year Next Year predicts that in 2020 the same will grow by 10.9%. This rate of growth is the only aspect on which both the reports have shown some similarity.