Category: RESEARCH

-

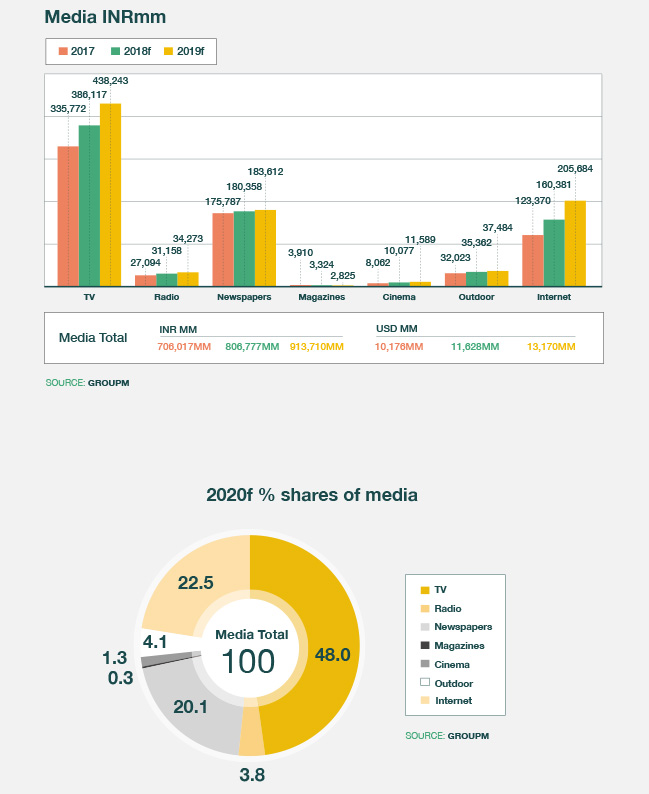

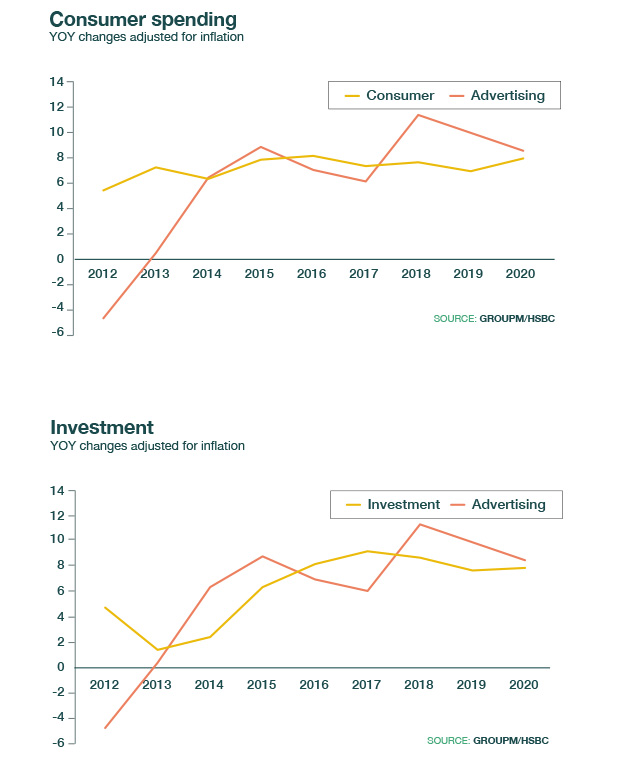

… but TV will have good adspend growth across key categories Digital spends may overtake print in 2019: GroupM report

From GroupM’s This Year Next Year report for June 2019 published on June 13:

Economy Recent downward revisions notwithstanding, India is expected to grow 7.1% – 7.5% in FY 2020–2021 (Fitch/IMF), with an investment cycle revival and sustained consumption being the key drivers. Downside risks remain: rising protectionism, a possible slowdown in global economy, and bad debt on bank balance sheets continue to hamper domestic investment. Inflation and deficits will, we think, remain largely under control, as public investment will grow only modestly.

Auto: modest-to-high adspend growth Recovery is expected in 2020 after a slowdown in 2019. Clearance of old stocks before new emission standards come into effect (April 2020) will boost sales in Q1. As usual, demand for motorcycles and tractors will be linked to a normal monsoon, improvement in farm/rural incomes and job creation – all of which remain uncertain at this point. Passenger vehicle, scooter and commercial vehicle advertising should see modest to high growth.

FMCG: high adspend growth FMCG will see robust volume growth as demand will remain broad-based. Rural demand will grow much faster than urban demand, aided by direct benefit transfers, farm support prices and other government schemes that increase household income. Urban demand will remain steady as a growing preference for premium and natural/ chemical-free products boosts volume.

E-commerce: very high adspend growth Robust double-digit growth is likely as e-commerce expands to smaller towns, more millennials/GenZ go online and consumers adapt to digital payments. Internet and smartphone penetration growth will continue at a fast pace, leading to huge opportunities for e-comm players.

Retail: high adspend growth Consumer trends of experiential shopping and the need for wellness and premium products will drive good volume growth. Foreign brands entering India, consolidation among established players and e-commerce buying stakes in established names are all likely to support growth in retail advertising investment.

Services: modest-to-high adspend growth Services have been driving the economy over the last few years and will continue to do so in 2020. The major segments of health, travel & tourism and transport will see good growth as consumers’ aspiration to travel and gain new experience rises with income.

Telecom: modest adspend growth Telecom will remain mixed: Handsets will see tremendous volume growth (especially low-to-mid-priced handsets), but incumbent service providers will see low-to-moderate revenue growth as they fight to retain market share.

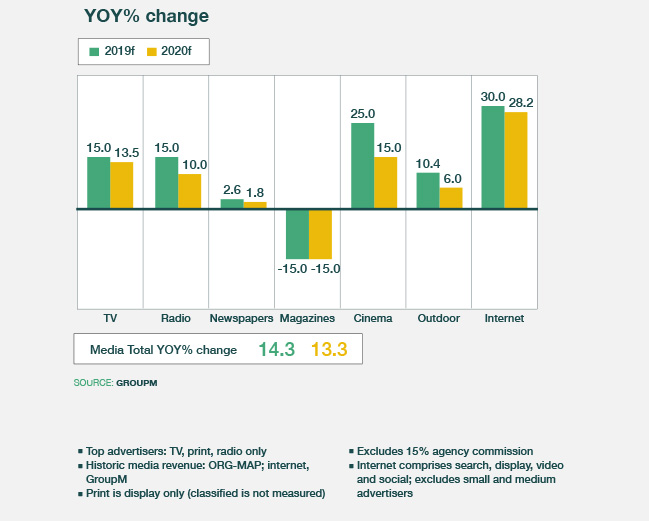

Media: TV will have good adspend growth across key categories; the T20 cricket World Cup will be a fillip. Print will record minimal growth on the back of Hindi and regional language dailies; English will decline. Radio will remain a key medium for localized, tactical advertising and will be driven by auto, retail and FMCG. Cinema and outdoor will see robust growth as more people flock to cinema screens, the number of multiplexes increases and theatre owners use better AV tech to attract audiences. As for digital, strong double-digit growth driven by video and e-commerce display may result in digital spends overtaking print at some point in 2019.

-

An EY global report notes that India represents a massive market for M&E A Billion Opportunities

By A Correspondent

The world is keenly looking at the Indian media and entertainment (M&E) market given the potential of growth. There is of course fair reason: According to consulting firm EY (aka Ernst & Young), with a “population of more than a 1.3 billion people, India represents a massive market for media and entertainment (M&E) companies, with very positive growth fundamentals across virtually every type of media.”

Said John Harrison, EY Global Media & Entertainment Leader: International expansion is critical for global media and entertainment (M&E) companies seeking to build scale, tap new audiences and enhance competitive positioning. Those looking to seize the upside of growth should set their sights on India. With more than a billion consumers and a favourable macro backdrop, India offers a massive opportunity across almost every type of media.

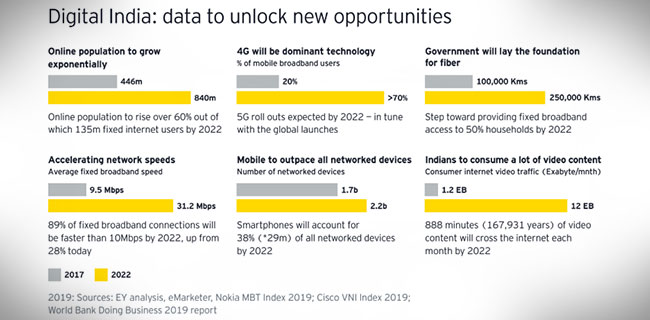

In a report released globally in late June 2019 titled ‘How a billion screens can turn India into a media and entertainment powerhouse’, the EY M&E team has reflected on the state and potential of M&E in India. “India’s M&E market is strategically interesting to global players seeking to monetize content and capture growth upside, either as a participant via licensing or other commercial arrangements, or as an outright owner through an in-bound acquisition or organic investment approach. Advertising, the lifeline of India’s M&E industry, remains among the lowest in terms of spend as a percentage of GDP, signaling upside potential. In addition to a myriad of digital outlets, India has more than 850 TV channels and over 17,000 newspapers, making it one of the most diverse and vibrant media markets globally. The country is also at an inflection point in wireless broadband connectivity and infrastructure that, combined with its GDP growth and young demographics, offer new opportunities.”

Click here for the full report

-

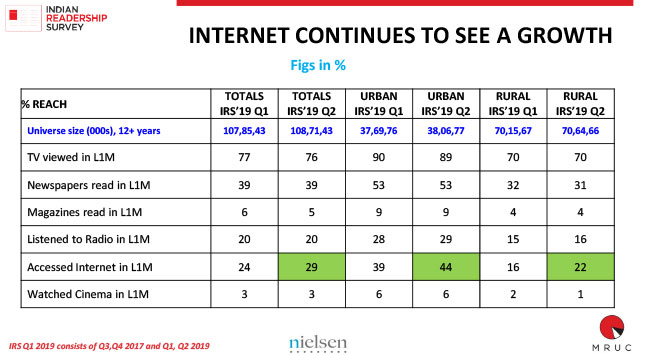

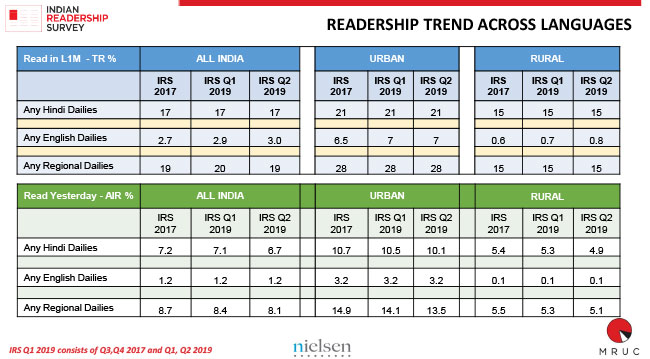

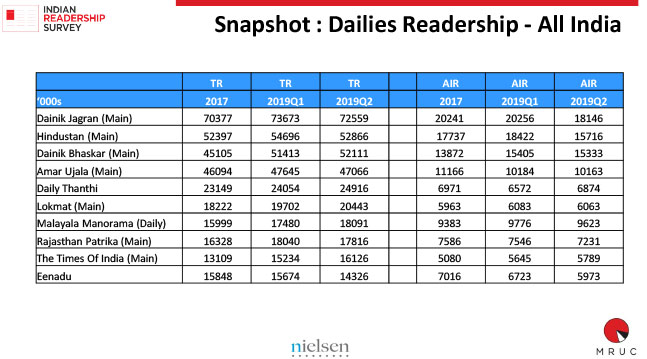

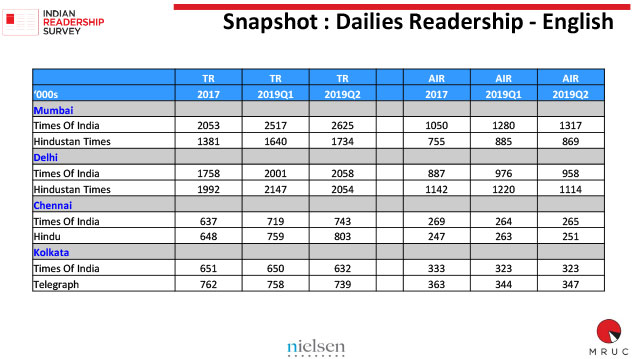

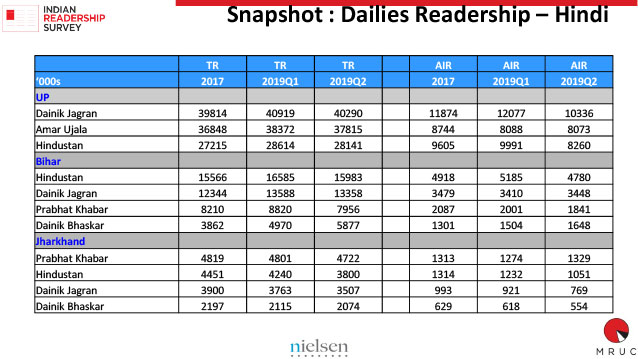

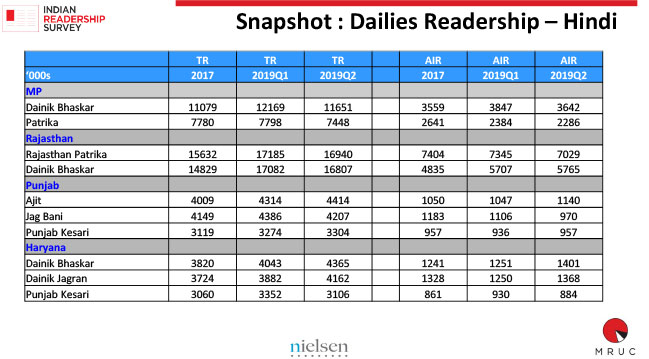

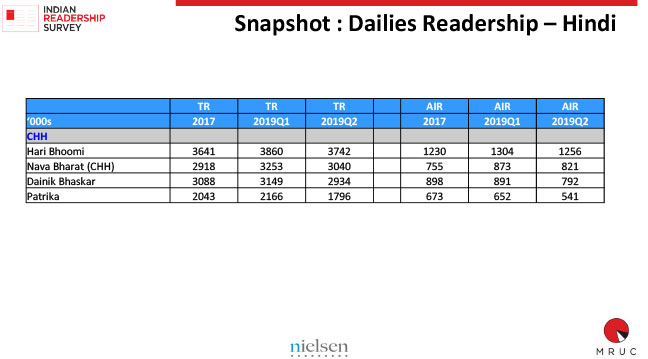

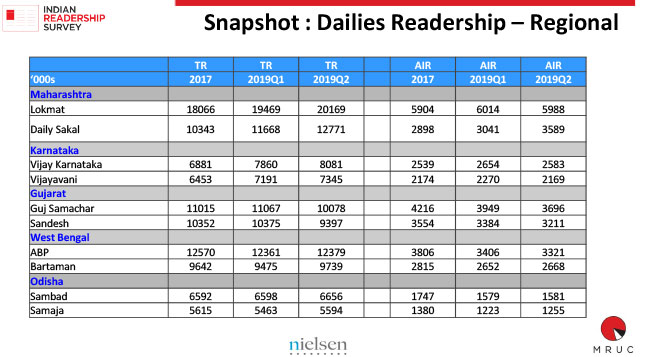

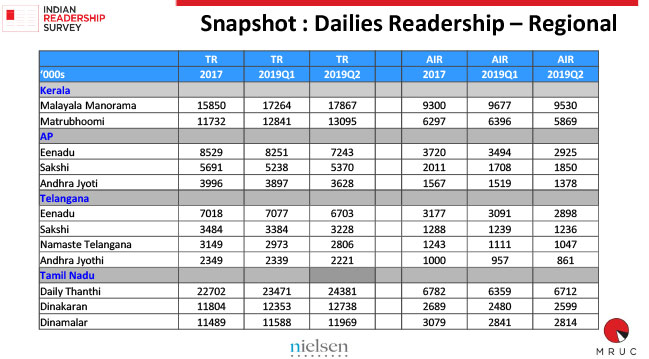

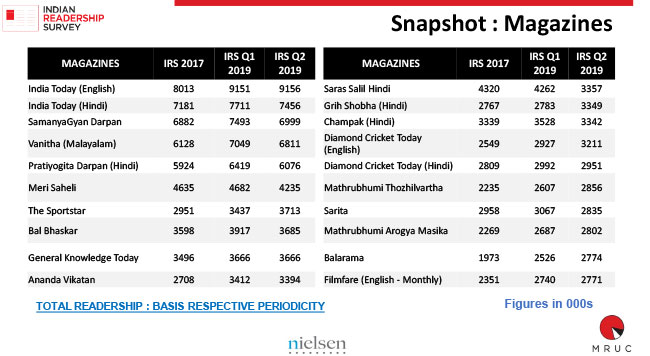

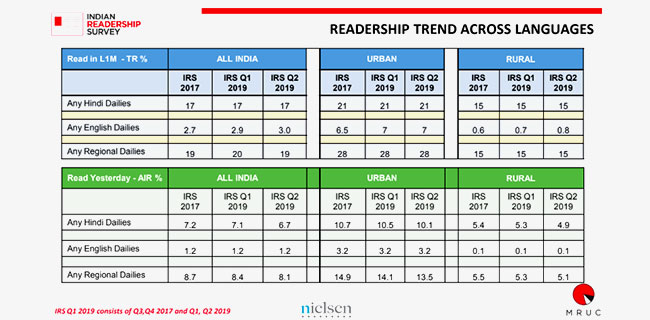

While Total Readership (TR) of publication remains steady, Average Issue Readership (AIR) has seen a marginal decline MRUC releases IRS 2019Q2 data

By A Correspondent

For many this week given the number of public holidays meant an opportunity to take a few extra leaves and go for a quick holiday. Yes, there are some part of the country which have been impacted badly by rains – especially for Mumbaikars wanting a quick getaway around Maharashtra, Gujarat or Goa or even coastal Karnataka.

For a weeks now, the industry is buzzing with rumours that the release of Quarter 2 of the Indian Readership Survey will be released in the second week of August. The MRUC Board and management would’ve reviewed the broad direction and identified the booboos, if any, if given the go-ahead.

Now the decision to release it: by doing so on August 14, a day before the national holiday of Independence Day, ensures that the backrooms in newspaper offices and their consultants can work unhindered by the daily grind. But, also, if there’s some angst about the survey results, time works as the best healer.

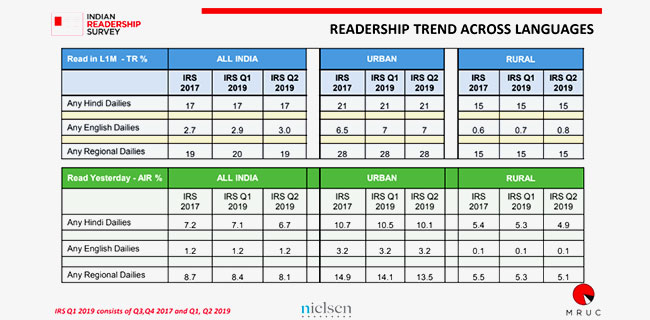

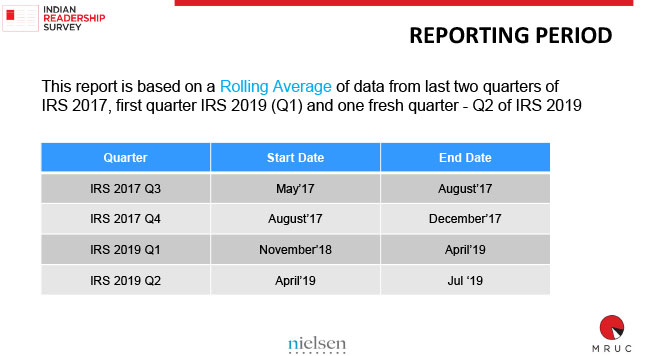

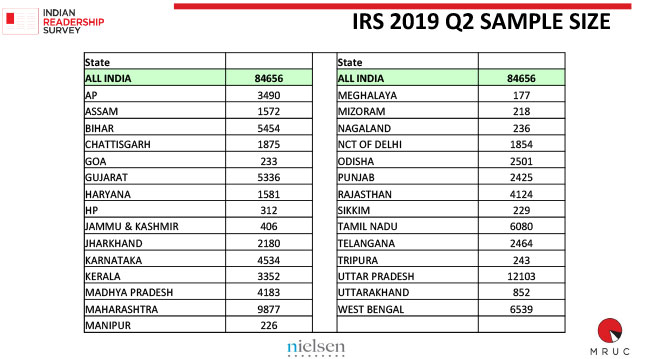

What reached our inboxes on August 14 afternoon was news of the release of IRS 2019Q2 data. The 2019Q2 data is a rolling average of the last two quarters of IRS 2017 (Q3+Q4) and the first two quarters of IRS 2019 (Q1+Q2). IRS 2019Q2 fieldwork covers April 2019 through July 2019. The reporting sample size for this data is 3.36 Lakh households.

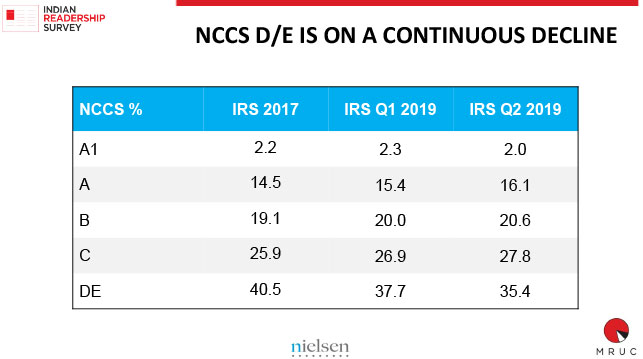

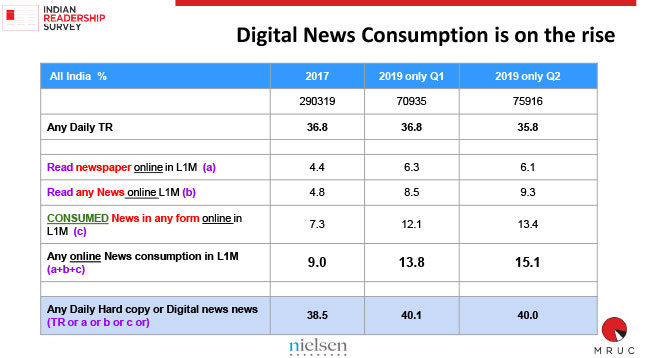

Here’s the bottomline, in the words used by the MRUC communique, not by us: The reach of print, television, radio and cinema vis-à-vis the previous IRS quarter, largely remains unchanged. Internet as a notable exception continues to grow. Consumption of news on digital platforms is on the rise. And whilst Total Readership (TR) of publication remains steady, Average Issue Readership (AIR) has seen a marginal decline.

Commenting on the release of IRS 2019Q2 data, Ashish Bhasin, CEO – Greater South and Chairman & CEO – India, Dentsu Aegis Network and Chairman, MRUC, said: “Firstly I must thank the MRUC Board and the IRS TechCom for their steadfast dedication in providing the industry with a timely and robust study. The findings of IRS 2019Q2 gives us a clear picture of the reality we all know – that digital is on a roll and continues to grow at a faster pace. Print readership remains healthy and I firmly believe the future lies in the power of two and not just one. I am very pleased to see IRS release every quarter. Not only is the IRS back on track, but has emerged much stronger and is being universally accepted as the currency for readership in India.”

Added Vikram Sakhuja, Group CEO Madison Media & OOH, Madison World and IRS Technical Committee Chairman: “We are very pleased with the quality of data that is being released this quarter. India is consuming more media than ever before. Internet is now fast catching up with Print and these two along with TV are the dominant mediums that can be used to reach consumers.”

The numbers you see here are just the toplines – these are the ones shared by MRUC. For the real thing, one needs to subscribe to the data. Valid point.

So there’s no real point in us analysing anything. Even the marginal decrease in AIR is an overall number… one needs to look at how the AIR number of a particular genre or publication is to make an informed decision.

INDIAN READERSHIP SURVEY Q2 2019 HIGHLIGHTS

-

Sanjeev Kotnala does a Kabuliwala take-off post the release IRSwala Aaya, IRSwala Aaya, IRSwala Aaya Re

By Sanjeev Kotnala

The latest round of IRS report is out. The reported readership figures have given soulless Print Rudalies a chance to cry in mourning or smartly find ways to celebrate minor victories.

The comparative game has begun. Everyone is flogging the tired horse. The fight to sliced the data continues. Everyone is wishing for that somewhat relevant claim which can help them fight the festive season battle. And there will be some lazy advertising for these claims. The biggest game in print is on.

It reminds me of the Kabuliwala poem that one has read and sung many times. A bit of a twist and a tweak somewhere and the bhands in newspaper title get to sing a new IRS song.

IRSwala, IRSwala, IRSwala,

English Newspaper kyun kumhlaya tera mukhda pyara

Hindi Paper kyun kumhlaya tera mukhda pyara

Kya khoyi hai Readership teri ya kisi ne circulation me mara,

Roonth gaya kya tera reader, toot gaya kya hawker,

Roonth gaya kyat tera reader, toot gaya kya hawker,

Ya phir tujhse bichhad gaya tera koyi advertiser,

IRSwala ha ha, kya wo quarterly report wala,

Abhi mila dey tumko use, dekho khel nirala,

Chalo readership ke paar jaha engagement ki hai war,

Kabhi Number 1 boley koi innovative kahani,

Chalo readership ke paar jaha loyalty ki hai war,

Kabhi Number 1 boley koi innovative kahani,

Jaane sabka wo haal, usse sabka hi khayal,

Badi sachchi hai, Readership ki badalti wo syani,Everyone wants just that slice of data to help claim a share of advertiser wallet. No one is bothered about its relevance. There is no question about how the numbers match? What do the numbers mean? Will they engage the uninterested advertisers and immune media buyers?

No one in the print media is willing to change. Something inside has broken. The sales team soul is not into the business. Everyone is looking at the brightness towards the end of rainbow called digital. Is it time to give up? I am not sure.

There is a strong inertia to change. No one wants to invest in understanding the root cause of the audience behaviour. Everyone has theories which have been strengthened by the multiple nods of heads inside boardroom presentations. Everything is directed towards boosting numbers. It’s different that IRS is a huge (scientific) extrapolation of a robust but limited data. Here is where the print industry has gone wrong. It cannot be the start and end of everything good or bad.

They have explanations. They have scapegoats. The undeniable truth keeps circulating in the corridors of print powerhouses. The enhanced availability, accessibility and affordability of data. The decreasing concentration of audiences. The fragmentation or multicity of interest.

In all of this the voice that calls spade a spade is ost. It is print’s inability to continue giving a differentiated, relevant and not necessarily impactful content. Play on its strength of Trust and Faith, which itself is under threat. However, there is high inertia in thinking and ideation. No one wants to move and take a call proactively. Everyone wants safety first. The choice of failing and falling is not acceptable to print stalwarts, and that is the reason they are failing their audience.

Nothing will change. IRS report will keep coming out. The changes will stop surprising the inert advertisers, media planners/buyers and the print saviours. We will find the IRSWALA and sing the last part of the song.

Tara rum, tara rum,

Readers se punchhenge hum, kyu roota hai who

Tara rum, tara rum,

Advertiser se punchhenge hum, Kyu badti TV digital se uski doosti.

Pal pal chhin chhin kum hota jaye,

Social linkage tode jayePal pal chhin chhin involvement kum hota jaye,

change ke pankh lagaye,

TV jhoome Digital ghoome, har dam chakkar chalta jaye,

TV jhoome Digital ghoome, har dam chakkar chalta jaye,

Pal pal chhin chhin reader segment jaye,

samay hawa ke pankh lagaye,IRSwala aaya, IRSwala aaya, IRSwala aaya.

-

Automotive, drinks, financial services, FMCG, food and retail Warc reveals the ‘Best of the Best’ across six key categories

By A Correspondent

Warc has released a ‘Best of the Best’ ranking of campaigns, agencies and brands showcasing the best all-round performances in the automotive, drinks, financial services, FMCG, food and retail sectors.

The six separate product category reports are based on the analysis of the combined data of the three annual Warc Rankings — the Creative 100, Effective 100 and Media 100 rankings — compiled from the results of the most prestigious and rigorous award shows of 2018.

Said Amy Rodgers, Managing Editor, Research & Rankings, Warc: “These sector analyses, the last of a series of reports produced based on the results of the Warc Rankings, provide category intelligence and an industry benchmark showcasing the top all-round sector performers across creativity, effectiveness and media excellence.”

Automotive category highlights:

With Audi topping two of the three automotive rankings, it is no surprise that Audi not only ranked #1 as a brand, but its owner Volkswagen Group came out as top automotive advertiser.

This success is reflected through the companies who worked with Audi, with BBH London ranked as the #1 agency with its campaign ‘Clowns’ topping the automotive creative ranking. Strong performances from PHD Worldwide agencies drove the network to the number one spot.

#1 campaign for creativity: Clowns, Audi, BBH London

#1 campaign for media: Lead Generation, Kia, Havas Media Madrid

#1 campaign for effectiveness: Beauty and Brains, Audi, BBH London / Salmon London / MediaCom London / PHD London

#1 agency: BBH London

#1 agency network: PHD Worldwide

#1 brand: Audi

#1 advertiser: Volkswagen Group

Drinks category highlights:

In the top ten agencies for drinks, there is a three-way split between Auckland (3 agencies), London (3 agencies) and Latin America (3 agencies), with MediaCom Mexico City taking first place and Africa São Paulo second. Touché! Montreal is the only agency representing North America.

With campaigns featuring in two of the three drinks rankings, Coca-Cola has topped the brands list and is ranked #2 in the drinks advertisers list. Anheuser-Busch InBev is in first place.

In the drinks category, MediaCom Mexico City tops the agency list and its network, MediaCom, ranks #4. BBDO Worldwide leads through the contribution of a range of agencies including AMV BBDO London (#7) and Colenso BBDO Auckland (#8).

#1 campaign for creativity: Tagwords, Budweiser, Africa São Paulo

#1 campaign for media: The Awesome Is Here, Cerveza Victoria, MediaCom Mexico City

#1 campaign for effectiveness: No More Excuses, Heineken, Publicis Milan / POKE London / Starcom Amsterdam / Publicis London

#1 agency: MediaCom Mexico City

#1 agency network: BBDO Worldwide

#1 brand: Coca-Cola

#1 advertiser: Anheuser-Busch InBev

Financial Services category highlights:

Due to the long-term success of Fearless Girl, which topped both the Creative and Effective 100 for financial services, State Street Global Advisors ranks #1 for brands and its owner State Street Corporation leads the advertiser rankings in the financial services sector.

Following on from this success, McCann New York, which worked on the campaign, tops the agency ranking and McCann Worldgroup is ranked #1 network with its agencies in Sydney, New Delhi and Mumbai also contributing to its success

#1 campaign for creativity: Fearless Girl, State Street Global Advisors, McCann New York

#1 campaign for media: The Animals’ Own Emergency Number, DNB, TRY/APT Oslo

#1 campaign for effectiveness: The Impact of Fearless Girl, State Street Global Advisors, McCann New York

#1 agency: McCann New York

#1 agency network: McCann Worldgroup

#1 brand: State Street Global Advisors

#1 advertiser: State Street Corporation

FMCG category highlights:

With Colenso BBDO and AMV BBDO London taking first and second place in the FMCG sector agencies’ ranking, it is no surprise that BBDO Worldwide is the top network, ahead of MediaCom in second.

Whilst Pedigree topped the FMCG brands list, this performance could only drive its owner Mars to #3 advertiser with Procter & Gamble ranked #1 through the performance of brands including Gillette, Procter & Gamble and Tide.

#1 campaign for creativity: #Bloodnormal, Bodyform/Libresse, AMV BBDO London

#1 campaign for media: I Don’t Roll On Shabbos, Gillette, MediaCom Connections Tel Aviv

#1 campaign for effectiveness: Healthy Hands Chalk Sticks, Savlon, Ogilvy Mumbai

#1 agency: Colenso BBDO Auckland

#1 agency network: BBDO Worldwide

#1 brand: Pedigree

#1 advertiser: Procter & Gamble

Food category highlights:

Skittles is the top brand with campaigns featuring across all three food rankings: Exclusive The Rainbow #1 for creative, Let Out The Sour #1 for media and Breaking Conventions With Pride joint #4 for effectiveness.

The agencies that worked on the winning Skittles campaigns all feature in the top ten agencies’ league table. The highest ranked is adam&eve DDB London, with work for Skittles as well as Marmite. DDB Chicago, which worked on the Exclusive The Rainbow is ranked #2. The success of these agencies alongside DDB’s offices in Paris, Johannesburg, Mexico and Moscow propelled DDB Worldwide to top network.

#1 campaign for creativity: Exclusive The Rainbow, Skittles, DDB Chicago

#1 campaign for media: Let Out The Sour, Skittles, MediaCom Dubai

#1 campaign for effectiveness: Cheetos Museum, Cheetos, Goodby Silverstein & Partners San Francisco / OMD New York

#1 agency: adam&eveDDB London

#1 agency network: DDB Worldwide

#1 brand: Skittles

#1 advertiser: Mars

Retail category highlights:

Mindshare Shanghai tops the agency list for retail having contributed to three of the top ten campaigns in the category in the Media 100 ranking, driving Mindshare Worldwide to #2 network.

Ogilvy is ranked #1 retail network, in part due to DAVID Miami’s work on Google Home of the Whopper, which came second in both the retail Creative 100 and Effective 100. This, along with Scary Clown Night (#1 creative campaign) meant that Burger King topped the retail brand list, with its owner Restaurant Brands International leading the retail advertisers table.

#1 campaign for creativity: Scary Clown Night, Burger King, LOLA MullenLowe Madrid

#1 campaign for media: Turning KFC Into Gamers Playground, KFC, Mindshare Shanghai

#1 campaign for effectiveness: How Lidl Grew A Lot, Lidl, TBWA\London / Starcom London

#1 agency: Mindshare Shanghai

#1 agency network: Ogilvy

#1 brand: Burger King

#1 advertiser: Restaurant Brands International