By Indrani Sen

The Media & Entertainment Industry has got another report which was released last week by KPMG, the longstanding partner of FICCI whose tie-upended in 2017 when FICCI awarded its M&E report mandate to EY. So, the Advertising and Media industry has now several reports to refer to for estimating the size and the growth of Indian Advertising Industry. KPMG has reported the following estimates and predictions for Indian Advertising Industry:

The Media & Entertainment Industry has got another report which was released last week by KPMG, the longstanding partner of FICCI whose tie-upended in 2017 when FICCI awarded its M&E report mandate to EY. So, the Advertising and Media industry has now several reports to refer to for estimating the size and the growth of Indian Advertising Industry. KPMG has reported the following estimates and predictions for Indian Advertising Industry:

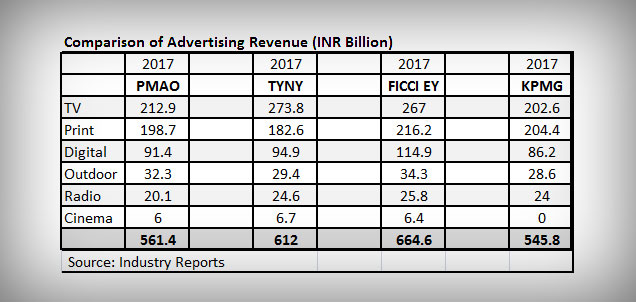

How do these reports compare when it comes to estimating the total advertising expenditure in India? The following table will give the top line information:

| Comparison of Advertising Revenue (INR Billion) | Â | |||

| Â | 2017 | 2017 | 2017 | 2017 |

| Â | PMAO | TYNY | FICCI EY | KPMG |

| TV | 212.9 | 273.8 | 267 | 202.6 |

| 198.7 | 182.6 | 216.2 | 204.4 | |

| Digital | 91.4 | 94.9 | 114.9 | 86.2 |

| Outdoor | 32.3 | 29.4 | 34.3 | 28.6 |

| Radio | 20.1 | 24.6 | 25.8 | 24 |

| Cinema | 6 | 6.7 | 6.4 | 0 |

| Â | 561.4 | 612 | 664.6 | 545.8 |

| Â Source: Industry Reports | Â | Â | ||

The above analysis shows us that TYNY and FICCI reports estimates are in one bracket with PMAO and KPMG reports in another bracket with a large gap in estimates between the two brackets. For two consecutive years, the TYNY and PMAO reports were released during the same week in January. TYNY closed the estimate for total ADEX 2017 at Rs 61,263 crore with a growth rate of 10% over 2016and PMAO showed a growth rate of 7.4% in 2017 over 2016 and estimated the total ADEX as Rs 53,138 crore in 2017.

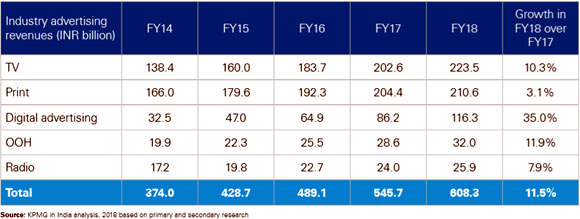

Digital is going to have the highest growth in ADEX as perthe two studies, 30% according to TYNY and 25% according to PMAO. KPMG has pegged the Digital growth rate even higher at 35%. Both reports predict 13% growth in TV AdEx and 4% (TYNY) and 5% (PMAO)in Print AdEx. KPMG has reported lower growth rates for both TV (10%) and Print (3%).

PMAO and TINY both agree that the highest growth after Digital will be achieved by Cinema (20% TYNY & 14% PMAO) which has the smallest share of the advertising pie. The FICCI EY 2018 report shows statistics for cinema industry revenue from domestic theatrical, overseas theatrical, cable and satellite rights, digital/OTT rights, in cinema advertising and home video. KPMG has not been reporting in cinema advertising in FICCI reports over the last few years as they have been clubbing it with digital/OTT rights and home video as ancillary revenue stream and they have continued with that trend in their own report. As the FICCI EY report 2018 has shown the detail break ups and I have taken the liberty of using the in cinema advertising revenue as a part of FICCI-EY total advertising projection. However, the growth rate cannot be estimated without access to KPMG’s research data.

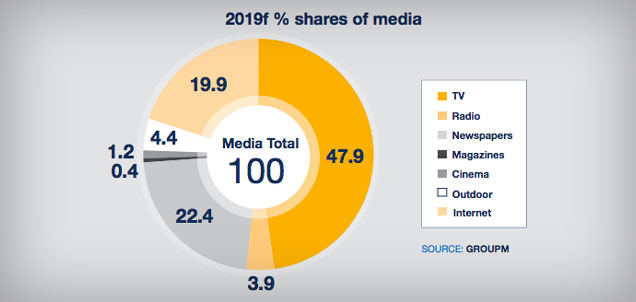

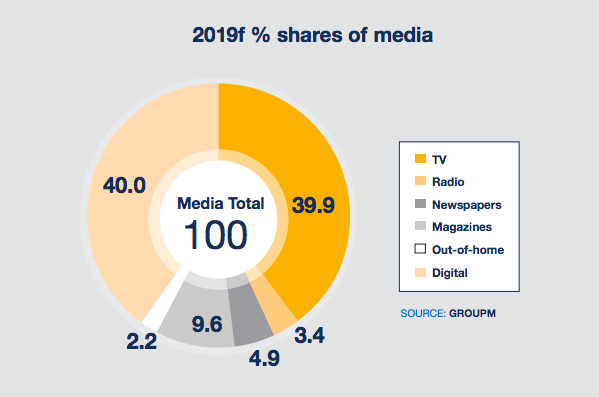

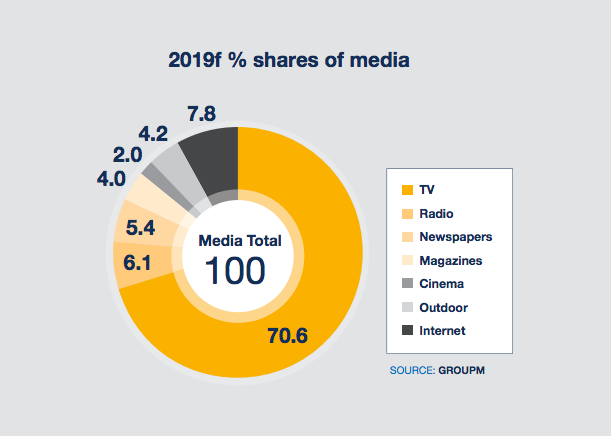

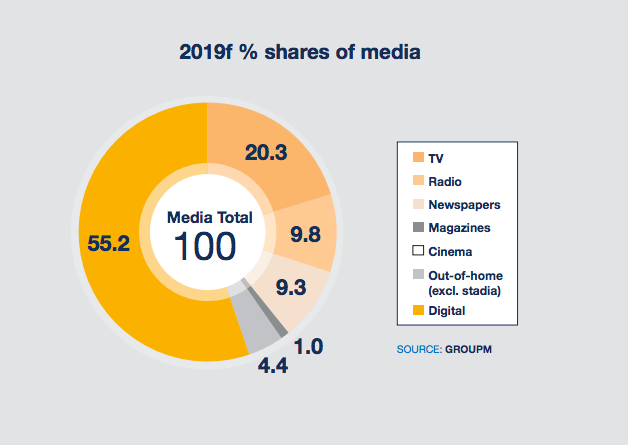

Both have shown similar percentile growth rates for OOH and Radio (15% TYNY & 10% PMAO). The KPMG report also predicts good growth rate for OOH (12%) and Radio (8%). The FICCI report and the Group M report are closer in terms of overall projections, but they differ in details but more or less agree about trend of growth in digital media.

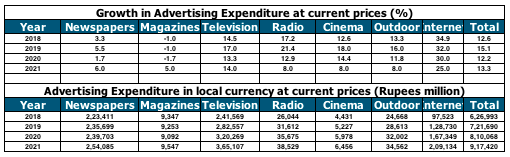

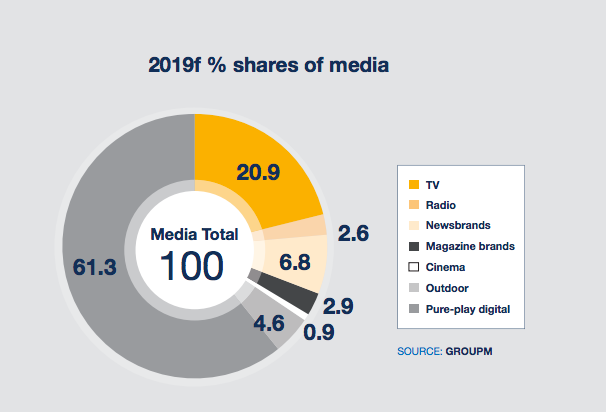

Before KPMG, we also had the DAN Report with estimates closer to PMAO and now KPMG. The Pitch Madison report and the DAN report are closer in terms of overall projections, though they differ in details, particularly in case of digital media

Source: DAN Report 2018

The gem of an insight which KPMG has been able to mine and share with the Advertising & Media Industry is reflected in the following quote: “This year, we saw telecom-media-technology (TMT)convergence take centrestage and the emergence of media ecosystems…. media companies need to take a relook at their strategies and business models to successfully operate and thrive in the new paradigm.â€

This insight adds a tremendous value to the KPMG 2018 report and warns the industry about the significant changes which we are going to experience about how media is created, distributed and consumed by Indian consumers. We will not be able to borrow a business model from another country, as the Indian model will be unique. Our law makers, particularly TRAI needs to tighten their belts and churn out rules and regulations capable of dealing with the changes in media consumption along with the ongoing changes at a pace which will keep pace with the TMT convergence.

The KPMG report and executive summary can be accessed at :https://home.kpmg.com/in/en/home/insights/2018/09/india-media-entertainment-convergence-report.html

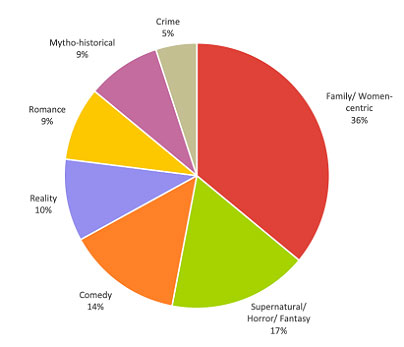

While all eyes this year have been on the OTT/ digital space, the Hindi GEC category too is silently, but surely, going through a shift this year. One doesn’t need to look much beyond the evolution of the programming mix on the category to understand this.

While all eyes this year have been on the OTT/ digital space, the Hindi GEC category too is silently, but surely, going through a shift this year. One doesn’t need to look much beyond the evolution of the programming mix on the category to understand this.