By Indrani Sen

By Indrani Sen

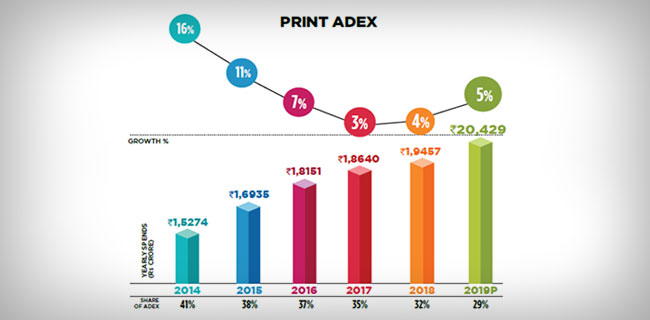

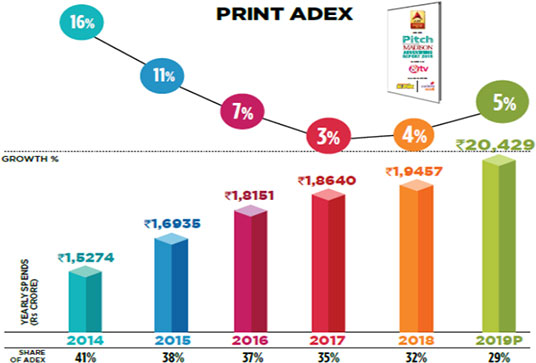

In his recent digital pitch with media bosses in New York, our Prime Minister claimed that unlike manufacturing, in the world of media, India is almost as evolved as any other country. Does his observation hold good for our print industry on which the sun continues to shine? The print majors are basking in the comfort of the findings of FICCI-KPMG and other such industry reports which are predicting growth, but a comparison of the CAGR percentages projected over the years reflects erosion.

| Projections of Print CAGR |

CAGR 2011 to 2015 |

CAGR 2011 to 2016 |

CAGR 2012 to 2017 |

CAGR 2013 to 2018 |

CAGR 2014 to 2019 |

| Total Print Market |

10%

|

9.10%

|

8.70%

|

9%

|

8%

|

| Source: FICCI-KPMG Reports |

2011

|

2012

|

2013

|

2014

|

2015

|

So, it is obvious that slowly but steadily the global trends have started to creep into Indian print industry. Accelerated penetration of mobiles in smaller towns and rural areas will support the growth of digital and social media and may result in faster erosion of CAGR in the print market and the CAGR 2020 to 2025 may come down drastically.

Instead of strengthening their arsenal with readership currency for protecting their share in the total advertising revenue, currently the Indian print industry seems to have taken up a negative stance against the IRS. Agreeably, many publications had genuine grievances against the findings of IRS 2013, but that should not be a legitimate reason for withdrawing their support from the readership survey. When the TV Industry has got a brand new currency from BARC which uses superior technology than its predecessor, the print Industry needs to rally around MRUC to ensure that IRS can also claim similar upgradation by introducing improved methodology.

In a large scale ongoing quantitative survey, teething problems and relative errors are quite normal. Perhaps the magnitude of the errors in IRS 2013 crossed the tolerance level of some print majors, but they should recollect that initially NRS findings also had many issues which got corrected over the years. We saw emergence of MRUC and IRS as a protest against the methodology and findings of NRS and subsequently the merger of the two surveys. We are witnessing now a dark period of three years in print currency as IRS 2013 was rejected by the print Industry, IRS 2014 (based only on fieldwork of one quarter) has not been taken seriously by the advertisers and agencies, and the field work for IRS 2015 has not yet commenced. In a developed country, such a gap in a media currency is unheard of. The sooner all the stakeholders of MRUC resolve their differences and kickstart the field work, the better it would be for second and third line publications who are likely to suffer more due to lack of readership data. The media planners and buyers cannot determine the incremental reach/ OTS/ CPT for adding more than one publication in the plan and are likely to limit their print campaigns to only the established market leaders.

Indian newspapers need to take up two challenges at two ends of the audience market. Firstly, they must try to reduce the gap between the literate population and the number of newspaper readers. Secondly, they must improve and promote their web editions and convert the internet savvy Indians to online readers. The concept of “Integrated Newsroomâ€, which is being advocated by many researchers and industry observers, is essential for achieving these two diverse tasks.

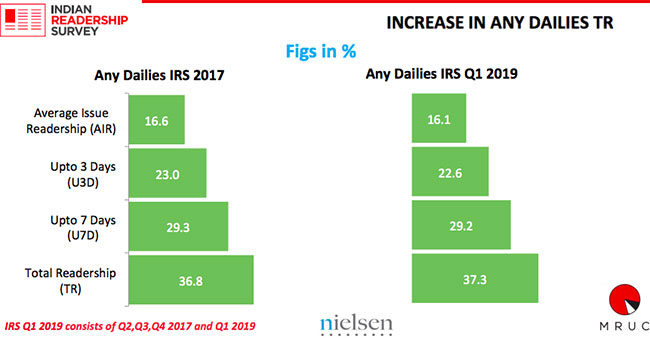

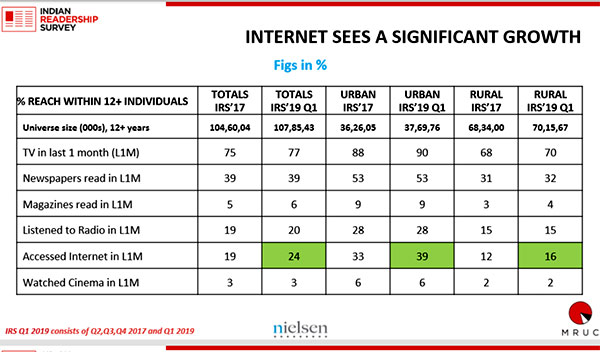

According to IRS 2012, approximately 44 percent of literate Indians do not read any newspaper. This average percentage decreases as one climbs up the SEC ladder and increases in small towns and rural areas. It is obvious that the current combination of regional, national and international news dished out by most newspapers is not acceptable reading material by a large chunk of Indian population. Special, smaller editions with more emphasis on hyper-local news may be more acceptable in the small towns and rural areas.

Most Indian newspapers have launched their e-editions, but there is lack of efforts in promoting as well as making them user friendly and interactive, perhaps due to the apprehension that the growth of online readership will cannibalize readership of the hard copies. There is a huge scope of growth for web editions of regional newspapers if they plan to ride on the growth of computer literacy in secondary schools in small towns and villages. Innovative marketing tie-ups with mobile manufacturers and service providers can increase the initial trial and subsequent conversion rate of the e-editions.

In this connection, it will be pertinent to note the new trends in readership surveys in developed countries, particularly in UK, as we have traditionally followed the example of UK for setting up our media infrastructure, media regulations, etc. In the 1970s, Indian National Readership Survey was also modeled largely on the Readership Survey of UK. NRS PADD was introduced in UK in September2012 to provide a unique measure of combined print and online audiences to cater to the demand of a dynamic and changing digital media age. It is a fusion of data by RSMB from two independent surveys, print readership survey by Ipsos MORI and comScore digital survey. It provides a single database for planning across print and digital platforms of NRS publisher brands. (Source: http://www.nrs.co.uk). Apart from full NRS demographic and classification data for profiling and targeting, the NRS PADD provides the unduplicated reach of a print publication and its website, duplication of print titles and websites – which websites do a publication’s readers visit, and vice versa. NRS PADD: Mobile was launched in September 2014. The future lies in combining readership research across the print and digital platforms. The opinion leaders in the print Industry must realise that the digital trends are irreversible and steer the industry in that direction.

The Global Media Report 2014 by Mckinsey & Co. predicted “Digital advertising is becoming a dominant force in the global media advertising market. Excluding the online and mobile components of TV advertising, in 2017 digital advertising will overtake TV, which for decades has been the largest advertising medium……….We project digital advertising to continue to increase at double-digit rates, growing 15.1 percent compounded annually to 2018 and accounting for 65 percent of the total increase in global advertising over the next five years. Most of that gain will come as advertisers substitute away from print media.†In India, the above trends are not likely to set in before at least another 5 years. Indian Print Industry needs to utilise this time period from 2016 to 2020 for protecting their future by ensuring immediate availability of print media currency, developing and promoting the websites and last but not the least, effectively converting more literates into readers.

Indrani Sen is a veteran media agency and marketing services professional. She is currently an Independent Consultant and Adjunct Faculty, Media Management at Symbiosis Institute of Media & Communication, Pune. This column will appear fortnightly. The views expressed here are her own.

The second wave of the pandemic is spreading all across the country and we are seeing state after state imposing various restrictions like night or weekend curfews, conditional lockdowns etc. The central government has decided not to impose a nationwide lockdown like last year which paralysed the entire Indian economy. The decision to impose restrictions for curbing the spread of the second wave has been left to the state governments. As the pandemic situation stands now in the second month of the April-June quarter, our economy is likely to see a contraction in this quarter which will have a cascading effect on M&E industry as advertisers will spend less on promoting their products and brands.

The second wave of the pandemic is spreading all across the country and we are seeing state after state imposing various restrictions like night or weekend curfews, conditional lockdowns etc. The central government has decided not to impose a nationwide lockdown like last year which paralysed the entire Indian economy. The decision to impose restrictions for curbing the spread of the second wave has been left to the state governments. As the pandemic situation stands now in the second month of the April-June quarter, our economy is likely to see a contraction in this quarter which will have a cascading effect on M&E industry as advertisers will spend less on promoting their products and brands.

Have you ever used any of the short video apps that sprung up after the ban on Tik Tok?

Have you ever used any of the short video apps that sprung up after the ban on Tik Tok?