![]()

By A Correspondent

The Covid-19 pandemic has caused shockwaves across the globe with major economies falling into a recession like no other in recent history.

As the advertising industry considers how to proceed, WARC, the global authority on marketing effectiveness, has released a comprehensive, evidenced-based report: The WARC Guide to Marketing in the COVID-19 Recession.

The guide includes learnings from past recessions, how the COVID-19 recession is different, lessons from China, key actions that brands can take now, and growth opportunities beyond the lockdown.

Said David Tiltman, VP Content, WARC: “A global recession is now highly likely, and the shape of the recovery is difficult to predict and will vary by sector. With many brands unable to distribute products and services, the usual advice to “keep advertising” may not apply in all cases, and marketers need to take a nuanced approach based on their brand’s situation.”

Added Lena Roland, Managing Editor, WARC Knowledge: “This WARC Guide to Marketing in a Recession pulls together the best thinking from across the industry on navigating the post-lockdown period. It presents advertisers, agencies and media owners with relevant frameworks, actionable ideas, and offers examples of how major marketers are already putting plans into practice.”

The five chapters covered in the WARC Guide to Marketing in the COVID-19 Recession are:

• The playbook for ‘normal’ recessions

A large body of research studies suggest that significantly reducing adspend in a recession has negative long-term impact on brands in terms of sales, market share, growth and return on investment. Companies that maintained investment recovered more quickly.

WARC has identified five marketing lessons from previous recessions:

(1) In a recession, media costs decline. (2) Defend your share of voice – cutting ad spend risks damaging market share. (3) Investing in adspend brings long-term advantage. (4) Decline in share can be hard to reverse. (5) “Going dark” beyond six months can weaken brands.

• Recession 2020: What we know so far

The COVID-19 recession is the first pandemic-driven downturn of the modern era. It is a healthcare crisis, leading to a severe economic slump. That also makes the shape of the recovery hard to predict, as consequences of the lockdown become apparent and there is risk of further outbreaks.

Sir Martin Sorrell predicts a “reverse square root” recession – a sharp downturn, a partial bounceback then a plateau.

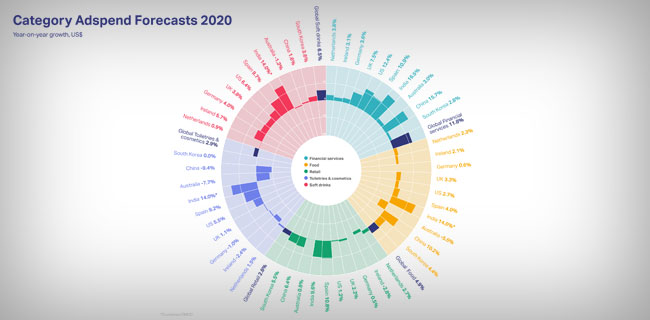

Cuts in media spend have been immediate and sharp. According to the latest Advertising Association/WARC Expenditure Report, the COVID-19 outbreak will wipe more than £4bn from the total UK ad spend for the current year, across all channels.

The 2020 downturn is set to be a demand and supply-side shock, caused first by lockdown and then by critical value chain components breaking down, particularly in China, leading to disruption in product and service delivery.

In a recent interview with WARC, Sir Martin Sorrell, Executive Chairman, S4 Capital, said: “You can’t say to a client spend your way through this. If you don’t have distribution, what’s the point?”

In a recent GlobalWebindex survey across 17 markets, 83% of consumers say they have delayed a purchase. But the impact of recession varies by brand and category.

In a new paper, exclusive for WARC, Les Binet, Group Head of Effectiveness, adam&eveDDB, said: “Different businesses face very different problems, and those problems will change as the crisis proceeds. There is no one-size-fits-all solution. Your strategy should be tailored to your business, and it should evolve as your crisis unfolds.”

• Recession 2020: Actions to take now

As lockdown measures are lifted and the recession takes hold, WARC offers key actions to help brands rebound. They vary depending on a company’s resources, and if operating in a boom or bust category. Brands should:

(1) Review their lockdown playbook. (2) Keep advertising if they can. (3) If a brand has to reduce adspend, use other levers to remain visible. (4) Maintain creative where possible. (5) Tailor the approach to brand-building and activation. (6) Kill or cut back on ‘dwarf’ brands. (7) Look for signs of new habit formation. (8) Audit e-commerce capability. (9) Build strategic alliances. (10) Review pricing but try to avoid discounting.

• Early lessons from China

As lockdown is lifted, Chinese consumers remain cautious and media habits are changing again, meaning marketers should retain a degree of flexibility in their media plans.

According to Publicis Groupe China, online video, social, and news content will be key during normalization. For outdoor ads, the rebound will be primarily in commuting routes, residential areas, and elevator areas.

Brands are also starting to reconfigure digital initiatives around e-commerce. For example, Friso China registered new customers into its CRM program through e-commerce incentives (discount coupons).

Restoring consumer confidence is proving a key challenge in China – and many brands are finding that packaging innovations can help resolve this. Meituan, an online-to-offline service launched contactless shields that protect customers from infection when eating.

The travel sector, one of the hardest hit by the first wave of the pandemic, should prioritise domestic demand based on the experience in China and North Asia.

The crisis has broadened the role of the big online platforms, such as Chinese retail giant JD; and China’s wide-ranging apps and digital services, which played an important role in the lockdown, are now doing so in the normalisation period, but data privacy is increasingly a concern.

• Opportunities for future growth

While the return will be gradual and tentative, and the playbook will vary by region and sector, downturns are an opportunity to initiate and accelerate change. WARC highlights opportunities to help brands on the road to recovery:

1) Supporting small and local businesses is a powerful strategy: SMEs will be among the hardest hit. Consumers may support initiatives that help rebuild local business and communities.

2) Finance brands can go beyond communications to support hard-hit consumers: According to Google, online searches for “financial help” recently grew 203% in just one week, as unemployment jumps.

3) Consumer goods brands can play with pack size to meet consumer needs: For brands seeking to defend market share from private-label, adding value through formats, innovation or value-on pack is going to be critical.

4) Develop a ‘close-to-home’ strategy: People will be eager to leave their homes, but the potential of a further outbreak – combined with economic hardship – means many will prepare their homes as a safe place of sanctuary and safety. Trend forecasting company WGSN (WARC’s sister brand) predicts home health and hygiene will be a key investment category.

5) Close-to-home means food stockpiling habits may persist: Conagra, the CPG company, says increased trial of frozen food during the lockdown offers a long-term opportunity for the category. Food companies may benefit from range extension and new product development in frozen and long-life products.

6) The ‘health economy’ will create new opportunities: The pandemic may be the catalyst for radical and lasting transformation of how health and wellness is experienced and delivered. Brands in categories outside health and wellness may be affected too, and should review opportunities to form partnerships that can reassure or help health-focused consumers.

7) COVID-19 is accelerating the need for digital transformation: Many of the trends caused or accelerated by the COVID-19 require the rewiring of companies around data and digital services. At a time of significant consumer change, there is an opportunity for CMOs to play a leading role in interpreting those changes and acting as ‘superconnectors’ between internal functions.

Added Jodi Harris, Global VP for Marketing, Culture and Capabilities, Anheuser-Busch InBev: “Marketing is swiftly moving beyond branding and communications to providing business solutions that address people’s needs… We’re taking on a new leadership role, connecting multiple disciplines within the organization to accelerate programs that make a difference in our communities and people’s lives.”