It’s still a few days before the first of the India forecasts are released by IPG Mediabrands and Publicis Media. And perhaps some India numbers from GroupM. But here’s GroupM’s review of 2019 and the forecast for 2020. Shape of things to come?

U.S. advertising will grow +6.2% in 2019 to $244 billion. This will mark a fourth consecutive year of solid mid-single-digit growth for the industry on an underlying basis. Taking out directories and direct mail makes the health of the industry look even stronger, with a +7.6% underlying growth rate for 2019, although including political advertising in all years brings growth down a few notches to +3.8% all in. However we look at it, growth has been robust relative to the general economy, which is generally decelerating on an underlying basis.

2020 still looks solid; we are forecasting +4.0% growth next year. We expect some softening next year as the economy reverts toward normalcy after a period of growth likely supported by factors including the 2017 domestic tax cut, an expanding federal deficit and low interest rates. As the effects of these fade, heightened trade barriers should concurrently become a drag on the overall economy. The 2020 Olympics also likely provide some marginal benefits, although we note that it can be difficult to identify the degree to which Olympic activity captures spending that would already have occurred or if it causes incremental spending to flow into the advertising market.

In more tangible terms, the key variables driving our model are personal consumption expenditures (PCE) and industrial production (IP), which combined have a solid 0.8 R2 correlation with normalised (excluding political) advertising. PCE will likely decelerate versus 2019 levels, while IP might go slightly negative. Using these inputs without adjustment would yield a zero-growth domestic advertising market next year, although it would be hard to imagine a three to four percent nominal GDP/PCE growth economy not producing a similar rate of growth in advertising. Further, we know that a range of factors implicitly not contemplated by our model are holding up advertising growth.

Digital-first marketers are likely driving much of the industry’s recent growth. We have previously written about the emergence of massively scaled digital brand owners whose businesses are endemic to the internet. We can point to Facebook, Amazon, Netflix,Alphabet, eBay, IAC, Uber and Booking.com as eight companies that are likely to spend more than $30 billion on advertising globally this year. Most of this spending will go into their home market, the U.S., adding billions of incremental spending every year into the domestic advertising economy. If we add in the next tier of digital endemics that may not have existed even a decade ago at anything like their current scale—think Wayfair, Chewy.com or any of the dozens of other digitally oriented companies spending hundreds of millions of dollars on advertising annually at this point in time—it’s not hard to imagine additional percentage points of growth emerging from these types of marketers.

Such rapid growth from these marketers as we have seen in recent years should abate, and eventually they should normalise their growth rates. This would contribute to industry-wide ad spend deceleration. However, the U.S. is more likely to produce more of these kinds of marketers in years ahead than are most other economies, and so there is some reason for a degree of optimism around these figures. For example, we expect the new and existing streaming video services to account for multiple billions of dollars in domestic advertising spending by the time these services are all operating at scale.

Overall, our best “feel” for the advertising market is to forecast a lower growth rate beyond 2021, and we incorporate a +3.0% expectation for subsequent years.

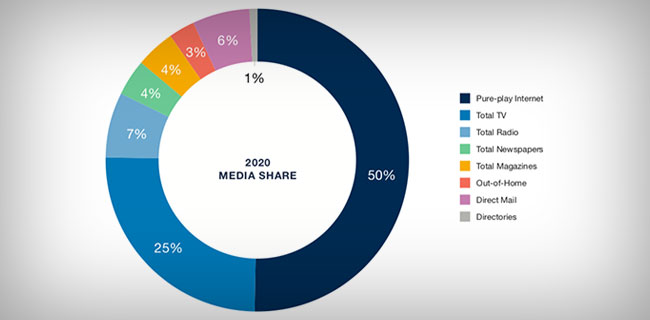

Advertising revenue to pure-play internet-based companies should grow by double digits next year to reach $127 billion in revenue, representing a 50% share of industry revenue. We forecast digital pure-play media (i.e., excluding digital revenues associated with traditional media owners) will end 2019 with a +20% increase. Growth is still expected to be resilient next year, rising by +13% in our forecast and accounting for 50% of all media we track here. There is undoubtedly still room to grow. We can certainly point to other developed economies that currently see digital advertising accounting for higher shares of industry-wide spending, but we think the aforementioned digital endemic marketers will increasingly replace traditional companies that came before them. As those marketers necessarily skew their spending toward digital advertising, spending shares shift in the aggregate toward digital media.

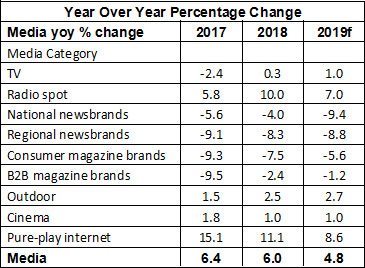

TV advertising is soft as we close 2019 and will end the year with a -7.0% decline (-2.0% excl. political), falling to $65 billion in ad revenue. Of course, many of the digital-first brands we’ve been discussing will also spend on traditional media, especially television. While defining a “digital brand” is highly subjective, those marketers are undoubtedly making up for most of the cuts in spending that other marketers appear to be making. Excluding political, underlying television advertising is trending toward a low-single-digit reduction during 2019. National TV advertising will be closer to zero, or even up very slightly, while local is down by low-single-digits. We expect this declining trend to persist, even with new forms of premium TV advertising regularly emerging. Certainly the ad-supported SVOD services will be attractive environments and their enhanced targeting capabilities will also appeal to advertisers. They will partially offset the ongoing erosion of traditional TV’s reach and frequency, but the core set of advertisers that have historically driven TV spending are likely to reduce the budgets they allocate to the medium.

Outdoor should be the fastest growing “traditional” medium, up by +8.0% to reach $8.3 billion. Among other media, outdoor remains a standout for its capacity to sustain growth. This is supported by ongoing innovation, especially in digital out-of-home and OOH’s relatively unique capacity to generate, capture and sustain attention. These advantages are more apparent to many marketers as traditional television continues to weaken. Digital formats are increasingly important, now accounting for half of spending on OOH, with further share gains still to come especially as more automation takes root, including the emergence of performance-based targeting and data-driven trading. At a category level, digital brands and luxury marketers have provided the industry’s recent boost, and much of this has been concentrated in the largest urban markets. These factors have enabled the medium to grow by +8.0% this year, a level that is not likely to be sustained. We expect more modest +4.0 to +5.0% growth levels over each of the next five years. Notably, this represents a gradual increase in the share of spending in the overall advertising economy, which presently amounts to 3.4%.

Radio is likely to be flat going forward. Radio appears set to hold on to its revenue base this year and is not likely to grow by much any time soon. While there is growing interest in the medium from national advertisers—especially supported by the likes of Pandora and Spotify as well as the emerging category of podcasting—the traditional base of geographically constrained advertisers that should be optimally positioned to support locally oriented media like radio has weakened over time.

Print will continue to be weak, although it retains value as a niche medium. Unsurprisingly and despite improvements in measurement and its capacity to engage deeply with consumers, overall, the medium is still set to decline on an ongoing basis. Double-digit declines are likely to persist for newspapers and magazines, even including digital extensions. Directories will likely look worse, with -20% or greater declines going forward. By declining in only low single digits, direct mail looks somewhat more positive.

U.S. political fundraising is approaching $16–20 billion for 2020; political advertising is expected to be $10 billion or more. So far, our forecasts have excluded politics from media spending because the scale of such activity meaningfully distorts year-over-year growth trends. Disclosures from the Federal Election Commission (FEC) covering the first half of 2019 indicate that total federal election fundraising was approximately $2 billion, up around +45% versus 2018 levels and +46% versus 2016 levels. During the prior two-year cycle, the first half-year accounted for only 15% of fundraising, and during the two-year cycle before that, the first half accounted for 16%. This indicates that fundraising through the end of 2020 will exceed $10 billion and could approach $12 billion for federal races, of which somewhere between 60–70% ($7–8 billion) would likely be disbursed during 2020. Local, nonfederal races are tracked separately and via different sources, but data from FollowTheMoney.org indicates that in 2018, there was a total of $8.7 billion in fundraising during that calendar year alone. Assuming that number rises next year, we could expect $16–20 billion in total political spending on all activities in the U.S. in 2020.

How much of this will turn into media spending? Our understanding is that in a typical campaign, 60% of funds raised may be deployed into media spending, which would translate into $9.6–12 billion in total activity during 2020, which places our $9.8 billion estimate on the low end of this range. Consequently, we recognise that the current political cycle could lead to higher levels of spending than we currently incorporate into our forecast. As our estimates currently stand, and including political advertising in all years, we forecast 2020 advertising growth of +7.1% on a broadly defined basis (including directories and direct mail) or +8.1% on a narrowly defined basis (excluding directories and direct mail).

Media is a means to an end; the marketer’s goal should be to optimise the mix of external and internal resources available to drive business growth. Putting all of this into some context, we are mindful that marketers can look at the data included here to gain a sense of the health of their media partners now and over the next several years. However, even a media owner in decline may still be investing in new and better ways to connect with audiences. At the same time, other media owners may be healthy in terms of revenue growth but may be neglecting to invest in everything they can to make their ad inventory more effective. As marketers continue to view media as a means to an end, investments in internal marketing infrastructure, marketing technology software and external services are among the other ways to support marketing excellence. We encourage marketers to put processes in place to optimise the balance between all of these elements. This will ultimately be more impactful than the choice to invest or stay away from any one type of media as it grows or declines in the years ahead.

Said Shashi Sinha CEO, IPG Mediabrands: “The Republic team has worked hard to deliver a reach of 73 million in its week of launch. They have given a repeat performance on their launch strategy by delivering big/ breaking stories and delivering massive reach. It’s a very good start and will give them an opportunity to build reach and market share in the coming weeks as the news genre sampling is very high in the run up to Elections. The Hindi genre is seeing an entry of another strong brand after a long gap of six years.â€

Said Shashi Sinha CEO, IPG Mediabrands: “The Republic team has worked hard to deliver a reach of 73 million in its week of launch. They have given a repeat performance on their launch strategy by delivering big/ breaking stories and delivering massive reach. It’s a very good start and will give them an opportunity to build reach and market share in the coming weeks as the news genre sampling is very high in the run up to Elections. The Hindi genre is seeing an entry of another strong brand after a long gap of six years.â€