By Our Staff

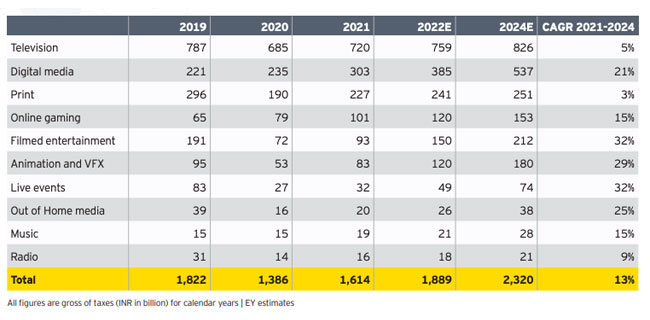

The Indian Media and Entertainment (M&E) sector grew 16.4% INR1.61 trillion (US$21.5 billion) in 2021, according to the EY-FICCI report ‘Tuning into consumer – Indian M&E rebounds with a customer-centric approach’ launched on Monday. Assuming no further impact of the pandemic, it is expected to grow 17% in 2022 to reach INR1.89 trillion (US$25.2 billion) and recover its 2019 pre-pandemic levels, then grow at a CAGR of 11% to reach INR2.32 trillion (US$30.9 billion) by 2024.

Digital media has firmly established itself as the second-largest segment. It grew by INR68 billion in 2021. Share of traditional media stood at 68% of sector revenues.

Said Ashish Pherwani, EY India Media & Entertainment Leader: “India has always been a different kind of media and entertainment market. High on volume and low on ARPU, yet up top with the rest on technology and ahead of the pack when it comes to digital adoption.” He added “Technology has led to the democratization of M&E in India – content is now created for the people, by the people and of the people. The flow of consumer data provides rich and real-time insights on what the consumer likes and dislikes, when where and how it is being consumed, and whether the price-points are appropriate.”

Added Sanjay Gupta, Chairman, FICCI Media and Entertainment Committee: “The massive disruption of COVID-19 in 2020 was a seminal event for all industries and more so for M&E as more people relied on it to educate, inform and comfort them during these challenging and complex times. I am pleased to see that, in 2021, the industry and consumers have embraced the choices that have emerged wholeheartedly, and a recovery is well underway with digital serving a pivotal role in it. In particular, the growing animation and VFX segment sets India up well to become the preferred content creator for studios globally.”

Said Jyoti Deshpande, Co-Chairman, FICCI Media and Entertainment Committee: “India is back post pandemic with a 16% growth in the M&E sector, helping us reach INR1.6 Trillion. After a difficult year and half, we have adapted and evolved with new ways of storytelling and innovation at every step. The creator market has exploded, we have hyper local content meeting cross border collaborations, all of it being leveraged by India’s unique ‘and’ market where the TV, Digital, Print, Radio and OOH not only coexist but complement each other. It’s an exciting time in the media & entertainment industry and I’m eager to see what new horizons we uncover.”

Here are excerpts from the report as shared by EY:

Advertising to reach INR1 trillion by 2024:

In 2021, when India’s nominal GDP grew 19%, advertising growth outperformed and grew 25%. The highest growth was in television advertising of INR62 billion, followed by digital advertising of INR55 billion and then of INR29 billion from a resilient print. By 2024, India’s advertising market should reach INR1 lakh crores (INR1 trillion).

Digital infrastructure – towards a billion screens by 2024:

India is getting connected – it now has 795 million broadband connections, over 500 million smartphones and 10 million connected TVs, apart from170 million active TV connections. 390 million Indians played online games, 150 billion streams of online music were consumed, 40 million Indian households paid for 80 million online video subscriptions and 400 million subscribers consumed bundled content in 2021. We expect the number of screens in India to reach 1 billion by 2024-25.

The great Indian content factory goes global:

India is amongst the largest content producers in the world – with 150k hours of TV content, 2,500 hours of premium OTT content and 2,000 hours of filmed content produced in 2021. India has over 950 animation and VFX studios, 185k electronic artists and 139 universities – and is fast becoming the content back office of the world.

There were over 100 M&E mergers and acquisitions in 2021:

The massive pace of change in M&E led to over 100 deals in 2021 – 86% of which were in new media and gaming. In 2021, many internet companies were listed on Indian stock exchanges. Unicorns in the M&E sector are expected to enter capital markets through a listing on Indian stock exchanges or through a SPAC listing in the United States in the next 2-3 years.

M&E sector will reach INR2.32 trillion by 2024:

The Indian M&E sector is expected to grow at a CAGR of 13% and add INR707 billion in three years to reach INR2.32 trillion by 2024. The key contributors to this growth will be digital, films and television (together adding 65% of the growth), followed by animation and VFX (14%) and online gaming (7%).

Segmental findings

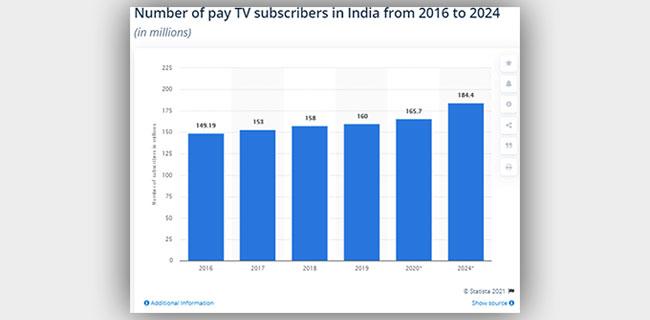

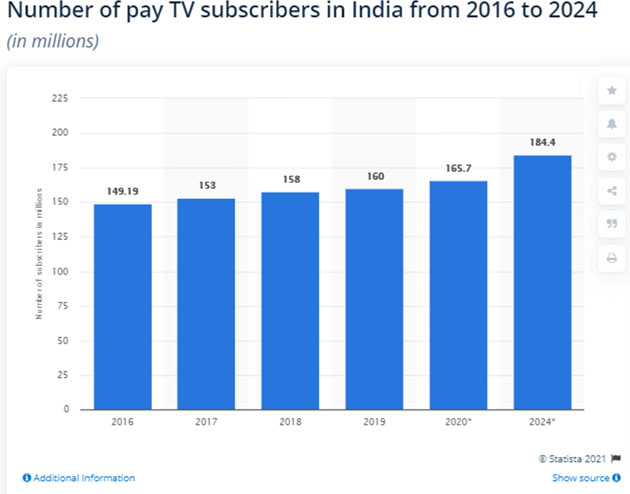

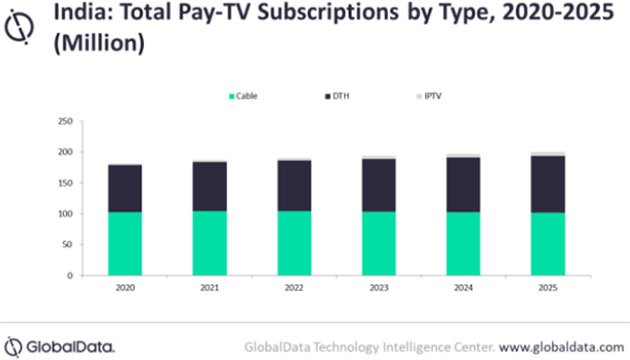

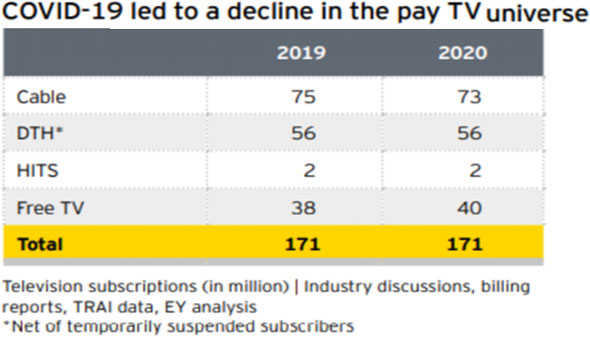

- Television– Television advertising grew 25% to end 2021 just 2% short of 2019 levels. Subscription revenue continued to fall for the second year in a row; experiencing a 6.2% de-growth due to a reduction in pay TV homes and a fall in consumer-end ARPUs. Connected TV sets, however, increased to 10 million

- Digitaladvertising – Digital advertising grew 29% to reach INR246 billion. In addition, advertising by SME and long-tail advertisers reached INR117 billion. Included in these revenues is advertising earned by e-commerce platforms of INR55 billion, which is now 16% of total digital advertising

- Digital subscription – Digital subscription also grew 29% to reach INR56 billion. 80 million paid video subscriptions across almost 40 million Indian households generated INR54 billion, an amount which is around 50% of broadcasters’ share of TV subscription revenues. Due to a plethora of free audio options, just three million consumers bought music subscriptions, generating INR1.6 billion

- Print– Advertising revenues grew 24% in 2021 as supply chains opened and circulation recovered. Print provides access to a large base of top-end consumers and remains an integral part of marketers’ brand launch and impact campaigns. Subscription revenues saw a growth of 12% on the back of recovery in direct to home and newsstand sales as well as rising cover prices. Print should continue on its growth trajectory in 2022 driven by hyper-local and regional news products

- Online gaming – Despite people going back to work as the effects of the pandemic receded, and regulatory uncertainty, the online gaming segment grew 28% in 2021 to reach INR101 billion. Online gamers grew 8% from 360 million in 2020 to 390 million. Real money gaming comprised over 70% of segment revenues. The segment will continue to grow and reach 500 million gamers by 2025 to become the fourth largest segment of the Indian M&E sector.

- Film– Despite capacity restrictions during the year, over 750 films were released in 2021, as compared to just 441 releases in 2020. Over 100 films released directly on streaming platforms, too. The segment grew 28% but remained at half its 2019 levels. The segment should recover to pre-pandemic levels by 2023

- Animation and VFX – At 57%, it was the fastest growing segment in 2021, as content production resumed, service exports increased, and the sector adopted virtual production

- Live events– The segment grew 20% over an extremely depleted base, primarily due to the relaxation of event curbs in a few states and increase in vaccination rates; however, revenues were just 40% of 2019 revenues. It should recover its 2019 levels by end 2024

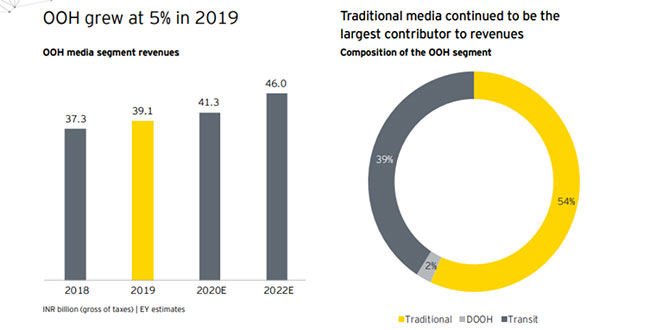

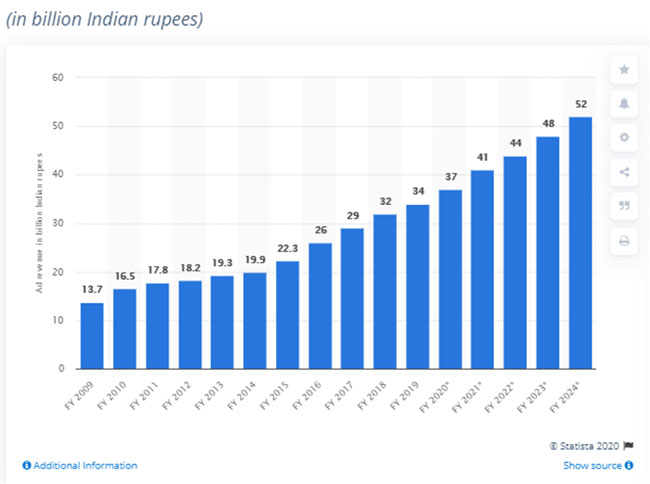

- OOH – OOH media grew 27% but remained at 50% of 2019 levels. Capacity utilization improved towards the end of 2021, but rates remained challenged. We expect it to regain 2019 levels not before 2024

- Music – The Indian music segment grew by 24% in 2021. 90% of revenues were earned through digital means, though most of it was advertising led, there being around only 3 million paying subscribers due to the presence of a plethora of free listening alternatives

- Radio– Ad volumes recovered 29% over 2020 but are still 6% behind 2019 volumes. Ad rates fell 13% on average and recovery will only be seen once daily travel resumes fully and the retail sector recovers. Many radio companies are looking at alternate revenue streams to make good the differential

In more than 25 years of observing the Indian media and entertainment industry closely, there has never been a period like the one we are in currently. Every mainline sector of the industry is going through a phase of stagnancy or descendancy. It is difficult to say if any of this will change anytime in a hurry.

In more than 25 years of observing the Indian media and entertainment industry closely, there has never been a period like the one we are in currently. Every mainline sector of the industry is going through a phase of stagnancy or descendancy. It is difficult to say if any of this will change anytime in a hurry.

The Indian newspaper industry faced an unprecedented crisis last year after the National Lockdown was declared at a very short notice. Circulation fell drastically when many subscribers, particularly housing societies, shut their doors for the newspaper delivery persons for the fear of the contagious virus being carried by the newspapers or the delivery folk, leading to change is consumption pattern of newspapers. Lack of local transport also prevented the distributors and hawkers from reporting for work. This was followed by withdrawal of commercial advertising as advertisers were worried about a fall in circulation and readership and were themselves affected by choking of distribution pipelines and economic slowdown leading to loss in their sales. The FICCI EY Report on Indian M&E industry 2021 showed that ad revenue of Print came down from INR 206 billion in 2019 to INR 122 billion in 2020.

The Indian newspaper industry faced an unprecedented crisis last year after the National Lockdown was declared at a very short notice. Circulation fell drastically when many subscribers, particularly housing societies, shut their doors for the newspaper delivery persons for the fear of the contagious virus being carried by the newspapers or the delivery folk, leading to change is consumption pattern of newspapers. Lack of local transport also prevented the distributors and hawkers from reporting for work. This was followed by withdrawal of commercial advertising as advertisers were worried about a fall in circulation and readership and were themselves affected by choking of distribution pipelines and economic slowdown leading to loss in their sales. The FICCI EY Report on Indian M&E industry 2021 showed that ad revenue of Print came down from INR 206 billion in 2019 to INR 122 billion in 2020.