By Our Staff

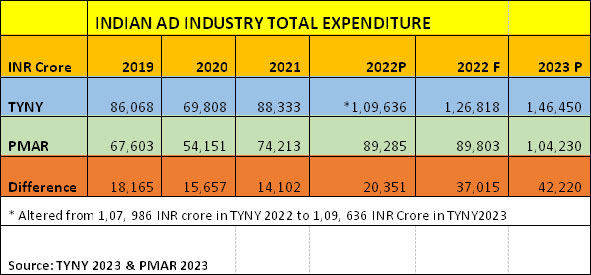

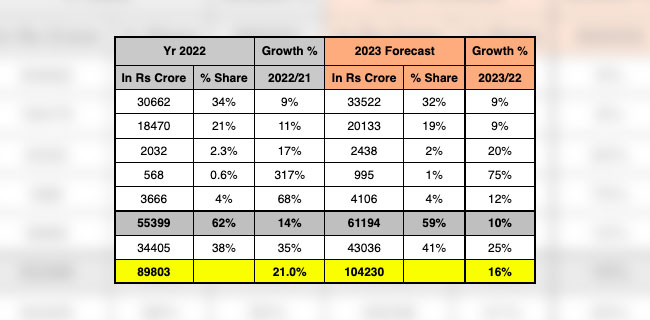

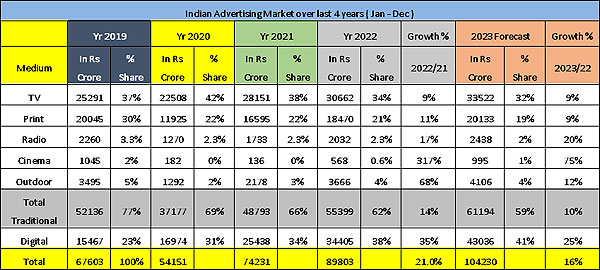

Madison Media presented its predictions for the advertising industry for 2023. The highlights of the report were released by Sam Balsara, Chairman, Madison World. According to Madison Media, AdEx has grown by 21% in 2022 to reach Rs. 89,803 crore. AdEx is expected to grow further in 2023 by 16% and will cross the landmark Rs. 1 lakh crore number to settle at Rs. 1,04,230 crores. In 2022, Digital grew by 35% to become the largest medium in AdEx with a 38% share, compared to TV’s 34%. TV grew by a modest 9% vs our projection of 14%.

Figures at a glance:

Key findings of the report:

A. Overall:

1) In 2022 total AdEx grew by 21%, Traditional AdEx by 14% and Digital AdEx by as much as 35%.

2) Compared to Indian AdEx growth rate of 21%, Global AdEx, according to WARC grew by just 8% in 2022. The Top 11 countries that account for 70% of Global AdEx grew by only 1%.

3) In absolute terms, AdEx has grown from Rs. 74,231 crore to Rs. 89,803 crore and this is the second highest gain of the last two decades.

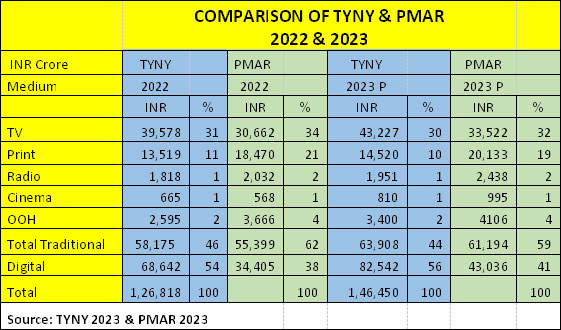

4) Traditional AdEx dominates Indian AdEx with a 62% share, whereas in Global AdEx the figure is 32%. With a growth of 14% in 2022, Traditional Media at Rs. 55,399 crore, has just crossed its 2019 figure of Rs. 52,136 crore.

5) Digital AdEx is now the largest medium with a share of 38%, followed by TV with a share of 34%.

6) The Audio Visual medium contributes to 45.6% of total AdEx. Linear TV at Rs. 30,662 crores and Digital Video at Rs. 10,314 crores, totalling to Rs. 40,976 crores.

7) FMCG continues to be the largest category, but its share has moved down from 38% in 2020 to 32% in 2022.

8) Ecommerce has now established itself as the 2nd biggest category of AdEx, growing in Share from 4.9% in 2019 to 14% in 2022.

9) The Top 5 Advertisers in AdEx are HUL, Reckitt, RIL, Dream11 and Mondelez. There are only 11 Start-Ups in the Top 50 Advertisers List vs 15 last year, confirming that VC money is drying up.

B. Digital

1) Digital grew by 35% in 2022, on top of a 50% increase in 2021, to reach Rs. 34,405 crore and has emerged the largest medium in AdEx with a 38% share, overtaking TV.

2) A 10-year review shows that Digital has grown from a mere Rs. 3,050 crores with a 9% share, to Rs. 34,405 crores with a 38% share today.

3) Inspite of all this growth, Digital AdEx in India trails behind Global AdEx. Digital share in Global AdEx is 68%.

4) Video, Social, Display, Ecommerce and Search drive Digital AdEx. Digital Video continues to dominate Digital AdEx and having grown by 40%, has further improved its Share from 29% to 30%.

5) Social grew the most at 45% and increased its Share from 20% to 22%. Display has grown more modestly at 19% and has lost 3 percentage Share points from 19% to 16%. Search has grown by 32%, but is only 16% of the market.

6) Ecommerce has registered a 35% growth and now has a share of 16% of Digital AdEx. Whilst Google and Facebook account for the lion’s share of Digital ADEX, Amazon and Flipkart account for almost 80% of Ecommerce spends.

7) Digital is going to continue to fuel growth of AdEx in 2023. It is expected to grow by 25% to reach Rs. 43,036 crore and increase its share to 41% of AdEx.

C. Television

1) TV registered a modest growth of 9%, against our forecast of 14% to reach Rs. 30,662 crore.

2) In 2022, for the first time we see signs of stress in Linear TV and its Share has come down from a high of 42% in 2020 and 38% in 2021 to a new low of 34%. With increasing spends in Digital, TV has now moved down to number 2 position in the Indian AdEx.

3) TV has also seen a 8% decline in viewership over the last year, and a 13% drop compared to pre-Covid year 2019.

4) TV has seen a marginal drop in Advertisers from almost 11,000 in 2021 to less than 10,500 in 2022.

5) FMCG continues to be the largest contributor to TV AdEx with a share of 45%. Ecommerce, the 2nd largest contributor to TV AdEx, further increased its share from 18% to 20%, followed by Auto which has maintained its share at 5%. Education has dropped its share from 6% to 4%.

6) In terms of Genres, Hindi GEC 2 has registered the highest growth of 47% followed by Sports at 22%. News, witnessed a degrowth during last year. Among the regional satellite channels, Tamil continues to rule the roost, followed by Telugu, Marathi, Bengali, Kannada and Malayalam in that order.

7) TV AdEx is expected to grow by 9% in 2023 to reach Rs. 33,522 crore.

8) FMCG, the largest category of TV Market, is likely to substantially increase its Advertising budgets, instead of reducing consumer prices because of lowering of raw material inflation.

D. Print

1) Print AdEx grew last year by 11% to reach Rs. 18,470 crores, a little short of its pre-covid figure.

2) Both Volume and Value in Print have gone up by 15% and 11% respectively.

3) H2 performed well for Print and 58% of its AdEx came from H2 vs only 46% in pre-Covid year 2019.

4) In terms of category contribution, although, Education de-grew marginally, it has emerged as the largest category in Print overtaking FMCG, which grew by as much as 8%. Two other large categories, Clothing, Fashion & Jewellery and Household Durables grew substantially by over 50%.

5) In terms of languages, Hindi Publications continue to dominate, followed by English and Marathi, the latter two having grown by 19% over 2021.

6) We expect Print AdEx to grow at 9% in 2023, to reach Rs. 20,133 crore and reach pre Covid levels.

With this growth, its Share will be 19%, compared to Global AdEx where it is a mere 4%.

E. Other Media

1) OOH AdEx has registered a high growth of 68% on the back of a growth of 69% the previous year, taking the industry to Rs. 3,666 crore and surpass its pre Covid level.

2) Digital OOH continued to be the growth driver with its big bright, colorful and moving displays.

3) Radio AdEx has grown by 17% to reach Rs. 2,032 crore, but it is still at 90% of its pre Covid level. Its Share in total AdEx is at 2%.

4) Real Estate has emerged as the largest category in both OOH and Radio, pipping FMCG.

5) Although Cinema grew by 317%, it has reached only the half way mark of its pre Covid number of Rs. 568 crore. But with new movies coming up, we expect Cinema to grow by 75% this year and reach Rs. 995 crore, almost upto its pre pandemic level.

Added Balsara: “Indian AdEx is the bright spot in a relatively dull and uncertain global environment. Our AdEx has grown by leaps and bounds in the last 3 years marked by Covid and the War, except in 2020. However, media habits of Indians are rapidly changing and this is reflected in our AdEx numbers and commentary. Advertisers who ignore these changes will do so at their own peril.”

Bharat Puri, Managing Director, Pidilite Industries Limited who launched the report said: “Experiment, innovate, know your consumer and don’t be afraid of failure”. He said, “Whilst chasing impressions, don’t forget to make an impression!”

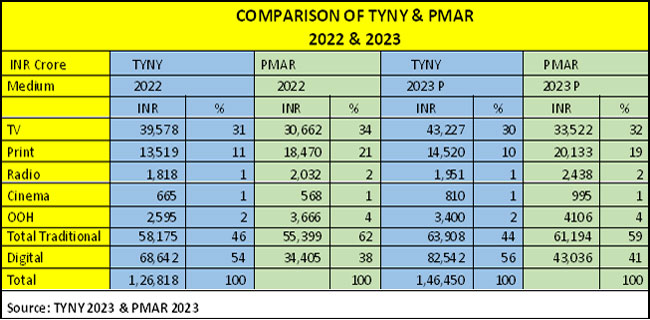

It is time to celebrate as the TYNY (This Year Next Year) 2023 report released by GroupM last week declared that the total value of Indian AdEx in 2022 has crossed the 100K crore mark touching INR 1,09,636 crore and in 2023 is estimated to grow at a healthy rate of 15.5% over 2022 towards another milestone of 150K crore (predicted as INR 146450 crore in 2023). Digital AdEx with an estimated 30% growth rate is expected to power the overall growth. India continues to be the fastest growing advertising market and as per the TYNY report has moved up from 9th position to the 8th position among the Top 10 countries with a share of 2% of the global adspend.

It is time to celebrate as the TYNY (This Year Next Year) 2023 report released by GroupM last week declared that the total value of Indian AdEx in 2022 has crossed the 100K crore mark touching INR 1,09,636 crore and in 2023 is estimated to grow at a healthy rate of 15.5% over 2022 towards another milestone of 150K crore (predicted as INR 146450 crore in 2023). Digital AdEx with an estimated 30% growth rate is expected to power the overall growth. India continues to be the fastest growing advertising market and as per the TYNY report has moved up from 9th position to the 8th position among the Top 10 countries with a share of 2% of the global adspend.