By Indrani Sen

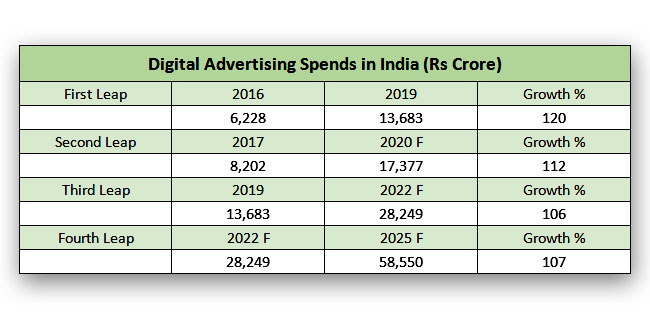

According to the DAN Digital Advertising Reports, spends on digital advertising in India is increasing by 100%+ every three years and is poised to cross the 50,000 crore milestone before 2025. It was only in the second half of the last decade, the Indian advertising industry crossed the milestone of 50,000 crores, so it seems strange that the newest and youngest competitor for the share of the advertising pie will be crossing that same milestone by middle of this decade! We have already witnessed the first giant leap from 2016 to 2019 and it seems quite possible that in three more giant leaps digital advertising will achieve this fantastic growth.

According to the DAN Digital Advertising Reports, spends on digital advertising in India is increasing by 100%+ every three years and is poised to cross the 50,000 crore milestone before 2025. It was only in the second half of the last decade, the Indian advertising industry crossed the milestone of 50,000 crores, so it seems strange that the newest and youngest competitor for the share of the advertising pie will be crossing that same milestone by middle of this decade! We have already witnessed the first giant leap from 2016 to 2019 and it seems quite possible that in three more giant leaps digital advertising will achieve this fantastic growth.

| Digital Advertising Spends in India (Rs Crore) | |||

| First Leap | 2016 | 2019 | Growth % |

| 6,228 | 13,683 | 120 | |

| Second Leap | 2017 | 2020 F | Growth % |

| 8,202 | 17,377 | 112 | |

| Third Leap | 2019 | 2022 F | Growth % |

| 13,683 | 28,249 | 106 | |

| Fourth Leap | 2022 F | 2025 F | Growth % |

| 28,249 | 58,550 | 107 | |

Source: DAN Digital Advertising Reports

The question which comes up next is which industry verticals are contributing to this spectacular growth of digital advertising? An analysis of the DAN Digital Advertising Reports show that almost across all industry verticals, advertisers have been increasing their spends across various platforms of digital advertising. The following table shows the comparative weightage on digital advertising by industry verticals in their total advertising budget in 2017 and 2019. Except Media & Entertainment where the weightage has remained 23% and miscellaneous small categories grouped under “others” where the weightage has gone down, across all other industry verticals, advertisers stepped up their expenditure on digital media. Digital media is no longer a myth; it is a reality now competing for share of the advertising pie and propelling the growth of advertising in India.

| Weightage on Digital Advertising | ||

| 2017 | 2019 | |

| FMCG | 7% | 19% |

| Auto | 12% | 16% |

| E Commerce | 30% | 37% |

| Retail | 16% | 20% |

| Telecom | 28% | 35% |

| BFSI | 24% | 42% |

| M&E | 23% | 23% |

| Consumer Dur | 19% | 38% |

| Others | 9% | 4% |

Source: DAN Digital Advertising Reports

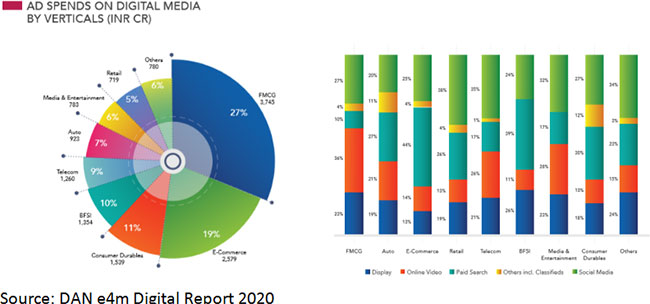

Though FMCG as a category spends 19% of their advertising budget on digital media, it contributes 27% of the total digital advertising pie, followed by E Commerce 19%, Consumer Durable 11%, BFSI 10% and Telecom 9%, followed by others as shown in the chart below on the left. So, across all industry verticals, advertisers have got into the Indian digital bandwagon.

The next chart on the right shows that based on the target audience and their use of different digital media, the various industry verticals use the different digital formats for advertising; while E Commerce and BFSI rely more on paid search, Retail and Telecom rely on Social Media. However, a comparison of 2017 and 2019 shows that the share of formats in digital advertising have hardly changed except video increasing at the cost of classified and paid search.

| 2017 | 2019 | |

| % | % | |

| Social | 28 | 28 |

| Paid Search | 26 | 25 |

| Display | 21 | 21 |

| Video | 19 | 22 |

| Classified | 6 | 4 |

Source: DAN Digital Advertising Reports

In 2017, 43% of the digital advertising was through mobile, which increased to 47% in 2019 and is expected to grow to 53% in 2020. Clearly, the mobile revolution in India has contributed in a large way to the growth of digital advertising. By the time digital advertising crosses the 50,000 crore mark mobile will have 60% + share in that revenue. Programmatic buying has also been growing year on year and by 2020 direct buying will be 44% with programmatic buying going up to 56%.

The digital media industry still faces many challenges, but apart from a detail discussion on ROI for digital advertising, the current report does not touch on the other issues like ad fraud, ad blocking software, lack of metric for measurement etc. On the whole, the DAN e4m Digital Report 2020 is an informative and excellent resource and the advertising and marketing industry should be thankful to the leadership of Dentsu Agies Network for sharing it free with all concerned.