By Indrani Sen

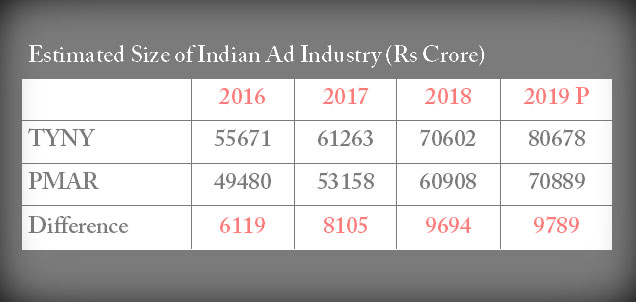

The official press release of the Pitch Madison Advertising Report (PMAR) 2016 predicting a 16.8% growth rate in advertising spends and a promise to cross the Rs 50,000 crore mark in 2016, instructed that the news should be carried only on Monday, February 15 or later. In true Indian style, the highlights of the report hit the online media on February 11! Before our Advertising & Media Industry could rejoice the prediction of “Boom Time†in 2016, on February 12, the Sensex posted biggest weekly fall in over six years with some sceptics in the industry murmuring about the possibility of a mid-year review by the authors of the report with a downward revision of the predicted trends.

It will not be surprising if our Advertising Expenditure gets on a roller coaster ride keeping in line with the predictions of PMAR 2016. Let us recall that as early as in 2003, Goldman Sachs forecasted that China and India would become the first and third largest economies by 2050, with Brazil and Russia capturing the fifth and sixth spots. It seems we have a date with the destiny if India has to live up to the forecast of Goldman Sachs. The real growth driver will be the increasing middle class population in India and their sheer numbers will absorb the shocks of falling Sensex, etc. According to Goldman Sachs, the middle class population in India is expected to grow exponentially between 2010 and 2020.

Sam Balsara’s quote in the Press Release confirms that similar factors have been considered by them– “In arriving at the numbers we are conditioned by the fact that the Indian economy has become the fastest growing economy of the world; our GDP growth rate at 7%+ is the envy of the western world, now looking at India in new light…â€.  Indian advertising market has grown consistently across last three years to achieve a growth of 60 %from 2013 to 2016, compared to the previous 3 years from 2010 – 2013, when the growth was only 28%.

In February 2015, the Pitch Madison Media Advertising Outlook 2015 first predicted a growth rate of 9.6% in advertising spend from 2014 to 2015. In September 2015, it was subsequently revised to 13. 8%. The final tally has emerged as 4 percentile point higher than their revised predictions. The year on year growth has not helped in our ranking in the global listing, which continued to be 12th with only 2% share of the global advertising pie. However, we have managed to increase our share by 1 percentile point.

| Percentage share in Global Advertising | |||

|

2013 |

2014 |

2015 |

|

| Brazil |

5% |

5% |

5% |

| Russia |

3% |

2% |

2% |

| India |

1% |

1% |

2% |

| China |

11% |

12% |

13% |

Source: WARC International AD Forecasts

We should remember that while 1 USD equals 68.13 INR, 1 USD equals only 6.53 Chinese Yuan. Like the practice of calculating normalised GRP in media planning, if we could have normalised the global advertising expenditure, then probably our ranking and share of the global advertising pie would have improved.

According to PMAR 2016, FMCG clients continued to be the largest contributor in 2015 and spent Rs. 12,364 crore or 28% in advertising across media, followed by Ecommerce players which contributed to 10% by spending Rs. 4,231crores, Auto and Telcom are next in line contributing 9% and 8% respectively. Contrary to the common belief that Ecommerce was the growth driver in 2015, organic growth from the FMCG sector played a major role in the growth of advertising expenditures. HUL topped the list of advertisers with a whopping Rs 2500 crore (approximate) spent in advertising.

In the nearly Rs.44,000 crore of Indian advertising expenditure in 2015, TV and Print continued to be the two dominant media with Digital enjoying the highest growth rate. After a gap of five years, TV has again emerged as the number one contributor in 2015 with Print loosing 3 percentile points in share which got distributed across TV (+1%), Digital (+1%), Radio (+0.5%) and Cinema (+0.5%). The projection for 2016 shows a further dip in the share of Print in spite of a 10% growth over 2015.

| Media wise share in advertising pie | |||

|

2014 |

2015 |

2016(P) |

|

| TV |

38% |

39% |

40% |

|

41% |

38% |

36% |

|

| Digital |

11% |

12% |

13% |

| OOH |

6% |

6% |

6% |

| Radio |

3.50% |

4% |

4% |

| Cinema |

0.50% |

1% |

1% |

Source: PMAR 2016 & PMAO2015

TV grew by 22% in 2015 and is expected to grow by another 20% in 2016 and add 1 percentile point in its share of the advertising pie. Â Hindi GEC channels continue to enjoy the highest share followed by News Channels (Hindi & English). All regional language channels earned additional revenue with Tamil, Kannada and Bengali channels also getting additional share of the business. Â The potential of the regional channels will be exploited by advertisers in 2016 for reaching out to rural audiences and perhaps the same has not been fully explored in the growth projections.

Print, the second largest medium, grew by 11% in 2015 and is expected to grow by 10% in 2016. However, it is projected to grow by another 10% but concede 2 more percentile point of its share to other media. In the language wise highlights presented in the presentation of PMAR 2016, newspapers and magazines have been combined while in PMAO 2015, similar analysis was presented for only dailies. However, as magazines reflected a negative growth of -3% in 2015, we can presume that most of the growth in Print in 2015 came from dailies. PMAO 2015 showed most of the languages dailies suffering negative growth rate (2013/2014) apart from dailies in Marathi. Gujrati, Kannada, Telegu and Bengali languages. In PMAR 2016 a reverse picture emerged with most of the language dailies enjoying accelerated growth rates except Gujarati which showed a negative growth. Oriya and Bengali (Dailies & Magazines) showed double digit growth rates (2014/1015) which came as a surprise.

Digital grew by 29% in 2015 and established itself as the third largest medium with a 12% share of the total ad pie in 2015. Digital is projected to grow at a 30% rate (2015/16) and increase its share in the advertising pie by 1 percentile point to 13%. Digital’s share in the advertising pie (11.6%) is more than the combined total share of Outdoor, Radio and Cinema (10.6%). However, the growth of Digital may have been underestimated considering the growth of smart phones and internet accessibility in India and the affinity of our youth with Digital and social media.

Outdoor revenues have been recast for last three years to include Digital OOH and Malls which are growing rapidly. Total OOH revenue including transit was Rs.2665crores in 2015 and is expected to grow to Rs. 3010crores in 2016.

Radio is predicted to grow to 1823crores in 2016 from 1545croers in 2015 and maintain its share of 4% in the advertising pie. While it grew by 20% in 2015, the above prediction means only 18% growth in 2016 when we are expecting the new bunch of radio stations to be operative before the year end. Again, the predicted growth of Radio seems to be conservative rather than bullish.

Cinema estimates have been revised to include advertising from various Government Agencies as well as local/ retail advertisers in 2015 as well as in the previous years. In 2015 Cinema contributed Rs. 465crores to the total advertising expenditure and is expected to grow to Rs.535crores in 2016.

As always, the Pitch Madison Advertising Report 2016 is a very useful document which will be used as a reference in the industry till the next report comes out. When we look at the ups and downs from 2007 to 2012 (chart above “A 10 Year Reviewâ€), we find it difficult to believe in the upward swing which we are witnessing over the last three years. Can the growth in 2016 be actually higher than 17.6% which we achieved in 2015? A million dollar question only time will tell.

Indrani Sen is a media services veteran, having worked with JWT, later Mindshare and then with Emami. In recent years, she is an independent consultant and academic. She is Adjunct Professor in charge of the Media Management programme at the Symbiosis Institute of Media & Communication, Pune. The views expressed here are her own.

By Indrani Sen

By Indrani Sen

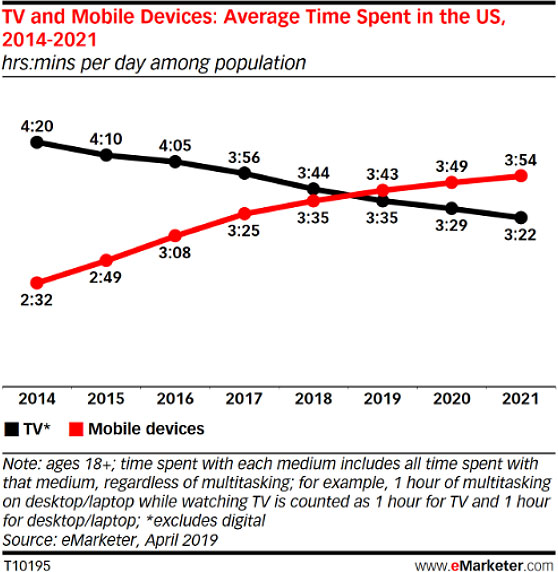

Recently, eMarketer conduced a global survey of the time consumers in different countries spent on media consumption per day. Adult consumers in India will spend 70.1% (3 hours, 30 minutes) of their daily media time on traditional media and remaining 29.9%, or 1 hour and 29 minutes on digital media in 2019 (https://www.emarketer.com/content/india-time-spent-with-media-2019).

Recently, eMarketer conduced a global survey of the time consumers in different countries spent on media consumption per day. Adult consumers in India will spend 70.1% (3 hours, 30 minutes) of their daily media time on traditional media and remaining 29.9%, or 1 hour and 29 minutes on digital media in 2019 (https://www.emarketer.com/content/india-time-spent-with-media-2019).