Jaquar Group has appointed Leo Burnett India to handle the creative mandate for Artize, the luxury bath brand from its stable. The mandate will be handled by the Leo Burnett Gurugram office.

Said Ranbir Mehra – Director, Jaquar Group: “Artize, the luxury bath brand from Jaquar Group is witnessing a metamorphosis. As a team, we are all set to take this brand to the next level of consumer experience. I am very happy to have Leo Burnett as our communication partner in this journey,”

Added Sandeep Shukla – Global Marcom Head, Jaquar Group: “Advertising agency is a crucial link between company and customer. We are glad to have Leo Burnett on board as our communication partner for brand Artize. I am sure industry is all set to see some superlative and out of the box brand ideas for the bathroom industry.”

Said Samir Gangahar, President – North, Leo Burnett: “It is special to partner a home grown legacy brand that has made very strong inroads in the premium and luxury segment. We look forward to working with the team to build on the success of Artize and take it to the next level of growth.”

The Advertising Standards Council of India has reported that during the months of August and September 2019, it investigated complaints against 564 advertisements, of which 179 advertisements were promptly withdrawn by the advertisers on receipt of communication from ASCI. The independent Consumer Complaints Council (CCC) of ASCI evaluated 385 advertisements, of which complaints against 344 advertisements were upheld. Of these 344 advertisements, 259 belonged to the education sector, 50 belonged to the healthcare sector, eight to personal care, eight to the food & beverages sector, and 19 were from the ‘others’ category.

There were several prominent brands in the Food and Beverage sector making comparative claims regarding the product composition, taste preferences, health benefits or market leadership. Many of the claims were not adequately substantiated. The CCC also considered the comparisons to be unfairly denigrating the entire category in which the advertiser brands were competing in. A leading dairy brand presented their butter cookies to be superior due to presence of 25 per cent butter and 0 per cent vegetable oil. However they made a sweeping statement that “other” butter cookies contain only 0.3 to 3 per cent butter and 20 to 22 per cent vegetable oil without presenting any verifiable evidence. Another snack brand, endorsed by a prominent cricket celebrity claimed that up to 60 per cent of people said that their baked snack was tastier than other fried snack brands. However, this claim was not conclusively proven. The same celebrity also endorsed a leadership claim for a food supplement brand ‘No. 1 Supplement for Men’. As this ranking was achieved in the UK and not in India, the claim was considered to be misleading.

Rohit Gupta

Said Rohit Gupta, Chairman, ASCI: “Recently as per media reports, Food Safety and Standards Authority of India (FSSAI) issued a statement that that the advertisers must desist from making misleading claims and that the food companies could be liable to pay a fine of up to INR 10 lakhs. Consequences of misleading advertising are grave, not only for the public but also for advertisers as it damages their reputation and breaks consumers’ trust in their products. ASCI encourages advertisers to follow the ASCI Code for self-regulation in advertising and Guidelines for Food and Beverages sector in particular so that all stakeholder interests are taken care of.”

EDUCATION: – 259 advertisements complained against

Direct Complaints (8 advertisements)

Suo Motu Surveillance by ASCI (251 advertisements)

HEALTHCARE: – 50 advertisements complained against

Direct Complaints (17 advertisements)

Suo Motu Surveillance by ASCI (33 advertisements)

PERSONAL CARE: – Eight advertisement complained against

Direct Complaints (2 advertisements)

Suo Motu Surveillance by ASCI (6 advertisements)

FOOD AND BEVERAGES: – Eight advertisements complained against

Direct Complaints (6 advertisements)

Suo Motu Surveillance by ASCI 2 advertisements)

OTHERS: – 19 advertisements complained against

Direct Complaints (10 advertisements)

Suo Motu Surveillance by ASCI (nine advertisements)

Mindshare has collaborated with Cosmic Information and Technology Limited to launch a new voice-driven platform called mSamvaad.

In its first venture, Mindshare rolled out a high-scaled engagement programme for Horlicks to reach out to mothers in the media dark areas of Bihar for its new variant that improves nutrient absorption among children.

Niraj Ruparel

Sharing his thoughts on the innovation, Niraj Ruparel, National Head – Mobile, Mindshare India said: “Since the past decade, our efforts have enabled number of top brands to engage their end-consumers with the most advanced and innovative voice-based solutions. Our solutions are aimed at penetrating the fragmented consumer segments of India and surpassing the barriers of communication due to low literacy rates and lack of access to data and connectivity. “mSamvaad” is one of our most successful voice product which we plan to take to the next level in the near future. We look forward to extending this platform to all prospects that are looking at customer engagement in rural India.”

Added Nilesh Bhagat, CEO, Cosmic Information and Technology Limited: “Cosmic Information & Technology Limited is committed and will continue to leverage its large and robust Voice Infrastructure and in-house innovation lab, to co-create quality solutions, which addresses brand challenges and help them to have a simple, yet targetted delivery of message as well as meaningful conversations with their brand audience, resulting into deeper level of engagements.”,

Vikram Bahl

Said Vikram Bahl, Area Marketing Lead, Nutrition, GSK: “This is a laudable initiative by Mindshare India along with Cosmic Infotech and we are glad to have been a part of it. We have always undertaken efforts to create awareness around holistic nutrition, especially in rural areas and this was a great opportunity for us to achieve our objective. We look forward to many such innovations in technology that can help us deliver intended message to rural markets.”

East Indian Hotels Limited, the flagship company of the Oberoi group, has appointed Mirum India for providing marketing cloud services. EIH has selected Salesforce Marketing Cloud platform to ensure seamless user experience through relevant communication for the right target audience and customers.

Said Hareesh Tibrewala, Joint CEO, Mirum India: “We are proud to be associated with one of the leading and internationally acclaimed names in the hospitality industry, The Oberoi Group. We are confident of implementing a seamless marketing automation system to address the customer needs, with our Salesforce platform expertise. We believe an integrated MarTech solution will support and positively impact the Group’s customer communication and engagement needs.”

It’s still a few days before the first of the India forecasts are released by IPG Mediabrands and Publicis Media. And perhaps some India numbers from GroupM. But here’s GroupM’s review of 2019 and the forecast for 2020. Shape of things to come?

U.S. advertising will grow +6.2% in 2019 to $244 billion. This will mark a fourth consecutive year of solid mid-single-digit growth for the industry on an underlying basis. Taking out directories and direct mail makes the health of the industry look even stronger, with a +7.6% underlying growth rate for 2019, although including political advertising in all years brings growth down a few notches to +3.8% all in. However we look at it, growth has been robust relative to the general economy, which is generally decelerating on an underlying basis.

2020 still looks solid; we are forecasting +4.0% growth next year. We expect some softening next year as the economy reverts toward normalcy after a period of growth likely supported by factors including the 2017 domestic tax cut, an expanding federal deficit and low interest rates. As the effects of these fade, heightened trade barriers should concurrently become a drag on the overall economy. The 2020 Olympics also likely provide some marginal benefits, although we note that it can be difficult to identify the degree to which Olympic activity captures spending that would already have occurred or if it causes incremental spending to flow into the advertising market.

In more tangible terms, the key variables driving our model are personal consumption expenditures (PCE) and industrial production (IP), which combined have a solid 0.8 R2 correlation with normalised (excluding political) advertising. PCE will likely decelerate versus 2019 levels, while IP might go slightly negative. Using these inputs without adjustment would yield a zero-growth domestic advertising market next year, although it would be hard to imagine a three to four percent nominal GDP/PCE growth economy not producing a similar rate of growth in advertising. Further, we know that a range of factors implicitly not contemplated by our model are holding up advertising growth.

Digital-first marketers are likely driving much of the industry’s recent growth. We have previously written about the emergence of massively scaled digital brand owners whose businesses are endemic to the internet. We can point to Facebook, Amazon, Netflix,Alphabet, eBay, IAC, Uber and Booking.com as eight companies that are likely to spend more than $30 billion on advertising globally this year. Most of this spending will go into their home market, the U.S., adding billions of incremental spending every year into the domestic advertising economy. If we add in the next tier of digital endemics that may not have existed even a decade ago at anything like their current scale—think Wayfair, Chewy.com or any of the dozens of other digitally oriented companies spending hundreds of millions of dollars on advertising annually at this point in time—it’s not hard to imagine additional percentage points of growth emerging from these types of marketers.

Such rapid growth from these marketers as we have seen in recent years should abate, and eventually they should normalise their growth rates. This would contribute to industry-wide ad spend deceleration. However, the U.S. is more likely to produce more of these kinds of marketers in years ahead than are most other economies, and so there is some reason for a degree of optimism around these figures. For example, we expect the new and existing streaming video services to account for multiple billions of dollars in domestic advertising spending by the time these services are all operating at scale.

Overall, our best “feel” for the advertising market is to forecast a lower growth rate beyond 2021, and we incorporate a +3.0% expectation for subsequent years.

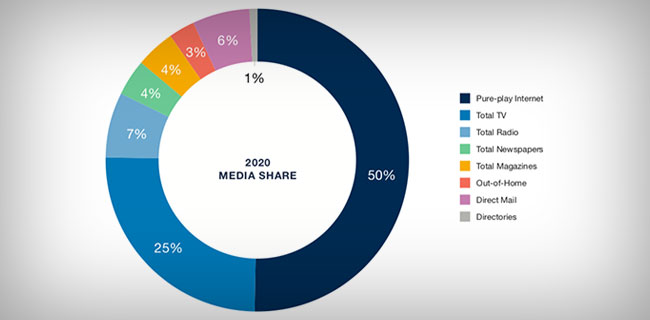

Advertising revenue to pure-play internet-based companies should grow by double digits next year to reach $127 billion in revenue, representing a 50% share of industry revenue. We forecast digital pure-play media (i.e., excluding digital revenues associated with traditional media owners) will end 2019 with a +20% increase. Growth is still expected to be resilient next year, rising by +13% in our forecast and accounting for 50% of all media we track here. There is undoubtedly still room to grow. We can certainly point to other developed economies that currently see digital advertising accounting for higher shares of industry-wide spending, but we think the aforementioned digital endemic marketers will increasingly replace traditional companies that came before them. As those marketers necessarily skew their spending toward digital advertising, spending shares shift in the aggregate toward digital media.

TV advertising is soft as we close 2019 and will end the year with a -7.0% decline (-2.0% excl. political), falling to $65 billion in ad revenue. Of course, many of the digital-first brands we’ve been discussing will also spend on traditional media, especially television. While defining a “digital brand” is highly subjective, those marketers are undoubtedly making up for most of the cuts in spending that other marketers appear to be making. Excluding political, underlying television advertising is trending toward a low-single-digit reduction during 2019. National TV advertising will be closer to zero, or even up very slightly, while local is down by low-single-digits. We expect this declining trend to persist, even with new forms of premium TV advertising regularly emerging. Certainly the ad-supported SVOD services will be attractive environments and their enhanced targeting capabilities will also appeal to advertisers. They will partially offset the ongoing erosion of traditional TV’s reach and frequency, but the core set of advertisers that have historically driven TV spending are likely to reduce the budgets they allocate to the medium.

Outdoor should be the fastest growing “traditional” medium, up by +8.0% to reach $8.3 billion. Among other media, outdoor remains a standout for its capacity to sustain growth. This is supported by ongoing innovation, especially in digital out-of-home and OOH’s relatively unique capacity to generate, capture and sustain attention. These advantages are more apparent to many marketers as traditional television continues to weaken. Digital formats are increasingly important, now accounting for half of spending on OOH, with further share gains still to come especially as more automation takes root, including the emergence of performance-based targeting and data-driven trading. At a category level, digital brands and luxury marketers have provided the industry’s recent boost, and much of this has been concentrated in the largest urban markets. These factors have enabled the medium to grow by +8.0% this year, a level that is not likely to be sustained. We expect more modest +4.0 to +5.0% growth levels over each of the next five years. Notably, this represents a gradual increase in the share of spending in the overall advertising economy, which presently amounts to 3.4%.

Radio is likely to be flat going forward. Radio appears set to hold on to its revenue base this year and is not likely to grow by much any time soon. While there is growing interest in the medium from national advertisers—especially supported by the likes of Pandora and Spotify as well as the emerging category of podcasting—the traditional base of geographically constrained advertisers that should be optimally positioned to support locally oriented media like radio has weakened over time.

Print will continue to be weak, although it retains value as a niche medium. Unsurprisingly and despite improvements in measurement and its capacity to engage deeply with consumers, overall, the medium is still set to decline on an ongoing basis. Double-digit declines are likely to persist for newspapers and magazines, even including digital extensions. Directories will likely look worse, with -20% or greater declines going forward. By declining in only low single digits, direct mail looks somewhat more positive.

U.S. political fundraising is approaching $16–20 billion for 2020; political advertising is expected to be $10 billion or more. So far, our forecasts have excluded politics from media spending because the scale of such activity meaningfully distorts year-over-year growth trends. Disclosures from the Federal Election Commission (FEC) covering the first half of 2019 indicate that total federal election fundraising was approximately $2 billion, up around +45% versus 2018 levels and +46% versus 2016 levels. During the prior two-year cycle, the first half-year accounted for only 15% of fundraising, and during the two-year cycle before that, the first half accounted for 16%. This indicates that fundraising through the end of 2020 will exceed $10 billion and could approach $12 billion for federal races, of which somewhere between 60–70% ($7–8 billion) would likely be disbursed during 2020. Local, nonfederal races are tracked separately and via different sources, but data from FollowTheMoney.org indicates that in 2018, there was a total of $8.7 billion in fundraising during that calendar year alone. Assuming that number rises next year, we could expect $16–20 billion in total political spending on all activities in the U.S. in 2020.

How much of this will turn into media spending? Our understanding is that in a typical campaign, 60% of funds raised may be deployed into media spending, which would translate into $9.6–12 billion in total activity during 2020, which places our $9.8 billion estimate on the low end of this range. Consequently, we recognise that the current political cycle could lead to higher levels of spending than we currently incorporate into our forecast. As our estimates currently stand, and including political advertising in all years, we forecast 2020 advertising growth of +7.1% on a broadly defined basis (including directories and direct mail) or +8.1% on a narrowly defined basis (excluding directories and direct mail).

Media is a means to an end; the marketer’s goal should be to optimise the mix of external and internal resources available to drive business growth. Putting all of this into some context, we are mindful that marketers can look at the data included here to gain a sense of the health of their media partners now and over the next several years. However, even a media owner in decline may still be investing in new and better ways to connect with audiences. At the same time, other media owners may be healthy in terms of revenue growth but may be neglecting to invest in everything they can to make their ad inventory more effective. As marketers continue to view media as a means to an end, investments in internal marketing infrastructure, marketing technology software and external services are among the other ways to support marketing excellence. We encourage marketers to put processes in place to optimise the balance between all of these elements. This will ultimately be more impactful than the choice to invest or stay away from any one type of media as it grows or declines in the years ahead.

DAN Programmatic has announced the launch of Dentsu Marketing Cloud Platform to power the network’s advanced analytics capabilities.

Shamsuddin Jasani

Commenting on the launch, Shamsuddin Jasani, Group MD, Isobar – South Asia said: “In our recent conversations with marketers, there is a growing pain point of limited data control due to the black boxes in which various ecosystems operate in. We are constantly hearing that clients are looking to gain deeper insights into their audiences and their journeys and to turn those insights into better brand and audience experiences. To address this concern, we have invested in developing from ground up the Dentsu Marketing Cloud Platform to present clients with greater insights to enhance marketing effectiveness and increase their control over their data.”

The Dentsu Marketing Cloud Platform will operate as a marketing intelligence platform, which will house intelligence from the globally acclaimed DAN Data Labs ecosystem, first, second- and third-party data. It brings together advertising and analytics to help surface deeper insights, establish enriched customer connections and drive better marketing results.

Gautam Mehra

Added Gautam Mehra, CEO, DAN Programmatic & Chief Data Officer, DAN – South Asia: “Under the Dentsu Marketing Cloud Platform, clients will be able to better segment their audience cohorts using advanced analytics. With the integration of client owned or DAN owned pixels governing the flow of data, clients will be able to run proprietary multi-touch attribution models, market mix models and a whole gamut of services to not only provide better insights, but to deliver high touched consumer experiences through sharper targeting,”

The Bengaluru offices of Mullen Lintas and Lowe Lintas have announced new leadership appointments. Kishore Subramanian, who successfully led Mullen Lintas’ agency office for over four years, has passed the baton to Siddhartha Roy.

Meanwhile Subramanian will be moving to Lowe Lintas as its Bengaluru office’s Planning Head.

Speaking about the key changes, Virat Tandon, Group CEO, MullenLowe Lintas Group said “I am delighted to welcome Sid to Mullen Lintas. In him, we found the skills to hyper-bundle the group’s services and give unfair share of attention to our brands. I was truly impressed by his entrepreneurial spirit and a future facing solutions mindset. I am positive that Mullen Lintas Bangalore has an exciting future under his leadership. I would also like to congratulate Kishore for giving Mullen Lintas Bangalore a formidable start by way of the brands and team he put together. Kishore is a planner at heart and that’s what he wanted to get back to. So, he takes over as the Planning Head for Lowe Lintas South. I am certain that he will bring his magic to the fabulous brands that Lowe Lintas Bangalore has and further develop the already strong planning product.”

Nielsen India expects the fast-moving consumer goods (FMCG) sales coming from the e-commerce channel to grow to $4 billion by 2022. The channel contributes 2 per cent to the current FMCG market. These are insights from Nielsen’s recently launched E-Trak Index – a measurement solution that tracks the FMCG E-Comm industry.

Metros lead the e-omm FMCG race with a 6 per cent contribution from the channel to total FMCG sales. Amongst these, Foods is the biggest contributor with 44 per cent; then it is personal care (40 per cent) and household care (13 per cent).

India’s first such solution is created using aggregated ePOS (electronic point of sale) data from cooperating E-commerce players and data science backed estimation for non-cooperating E-commerce players in India. The index adds a crucial element to the Retail Measurement Services that Nielsen provides by adding a view of the FMCG E-Comm space for All India Metros currently – with monthly read for Total FMCG, Super-categories, Category level for about 20 categories and for 11 categories at a top manufacturer level. Manufacturers and marketers get data, information and insights that can be further used to hone their E-Comm channel sales strategy to help shape a smarter market.

Announcing the launch of E-Trak, Prasun Basu, South Asia Zone President, Nielsen Global Connect, said: “Measurement is necessary. Measurement is difficult. Best possible measurement.” Explaining this further he added “Data and insights from Nielsen’s Retail Measurement Services continue to provide an essential foundation for manufacturers and marketers to understand their market. In this rapidly evolving world of commerce, India’s FMCG industry is now making its presence felt in the E-Comm channel – appealing to consumers’ need for convenience, and in sync with increasing smartphone and internet penetration. To give a truly complete picture of the changing marketplace, we are happy to announce that Nielsen India has launched a specific E-Trak index that will now measure FMCG consumer offtake in the E-Comm space – marrying this with trends seen in modern and traditional trade to get a read on omnichannel in the country.”

Added Sharang Pant, Head-Retail Measurement Services and Retailer Vertical, South Asia, Nielsen Global Connect: “While the foundation is taking shape, E-comm’s dynamic nature has made it a disruptor in the marketplace. E-Comm has seen a transformative journey and is now a $1.2Bn Industry growing from 0.5 per cent contribution in 2016 to a 2 per cent contribution in 2019, and slated to be 5 per cent in 2022 – this is in half the time that brick and mortar retail took to evolve. That said, these channels are not cannibalizing each other, and all continue to grow with E-Comm outpacing modern trade and traditional trade. The view that Nielsen presents on understanding channel, category and consumer trends will directly help players understand the right strategy in terms of assortment, pricing and positioning to win with the evolving consumer”

Said Nitya Bhalla, Head- Data Science, South Asia, Nielsen Global Connect: “Given the significance of the channel from both a current as well as future perspective, Nielsen has built a unique state of the art hybrid model for estimating this dynamic and growing channel. The methodology involves leveraging data from key collaborating E-tailers in the FMCG space. We then use crowd sourced data coupled with machine learning techniques from a panel of 200K+ consumers to estimate the Ecommerce sales for FMCG products.”

The Advertising Club has announced the nominees of the 2019 Marquee Awards. The awards will be presented on Thursday, December 12 in Mumbai.

Speaking about the upcoming edition of the Marquees, Partho Dasgupta, President, The Advertising Club said: “Our focus at the Advertising Club with award platforms like the Marquees is to encourage and applaud pioneering work by brands and marketeers that have helped in furthering every category’s growth agenda through crafting effective brand strategies.”

The list of nominees for MARQUEES 2019 are as follows:

Sr. No

Sector Category

Company

1

Auto (4 Wheeler)

Maruti Suzuki India Ltd, Hyundai Motor India Ltd, Tata Motors Ltd, Honda Cars India Ltd, Toyota Kirloskar Motor Pvt Ltd, Mahindra and Mahindra Ltd., Ford India Pvt Ltd.

2

Auto (2 Wheeler)

Hero Motocorp Ltd, Bajaj Auto Ltd, Suzuki Motorcycle India Pvt Ltd, Honda Motorcycle and Scooter India Ltd, TVS Motor Company Ltd, India Yamaha Motor Pvt Ltd, Royal Enfield (Unit of Eicher Ltd)

LIC, Tata AIA Life Insurance, Aditya Birla Sun Life, SBI Life, Max Life, ICICI Prudential Life, Kotak Mahindra Life, Bajaj Allianz Life, HDFC Life

7

Insurance (Non-Life)

Tata-AIG, SBI General, Star Health Insurance, ICICI Lombard, IFFCO Tokio, New India, Oriental, Reliance, Bajaj Allianz, HDFC ERGO

8

Banking

State Bank of India, HDFC Bank, Ratnakar Bank, IndusInd Bank, Bandhan Bank, ICICI Bank, Axis Bank, Canara Bank, Kotak Mahindra Bank, Bank of Baroda, Yes Bank, Punjab National Bank

Adspends in India will grow 12.6% in the year 2020, a slight increase from the 12.4% in the year 2019. This was part of the global ‘This Year Next Year’ report released by GroupM at a global level. It may be noted that GroupM presents its India-specific numbers every year in early February, which can hence be expected two months from now.

According to the numbers released, for India, the growth in television will be 11.1%, whereas for radio it will be 8%. The growth forecast numbers for newspapers and magazines are 1% and -10% respectively. While the growth for outdoor and cinema is pegged at 8.1%, that for internet will be 26.3%.

Prasanth Kumar

Said Prasanth Kumar, CEO, GroupM South Asia: In 2020, India faces challenges and uncertainties across sectors, just like other markets. However, this also brings opportunities for brands to innovate. This will be propelled by greater use of technology and better content across media.”

Meanwhile, here’s the rest of the report:

The global economy has weakened in 2019 and will remain similarly soft in 2020. By our calculations, based on Refinitiv data, the gross domestic product (GDP) of the countries we track in “This Year, Next Year” is growing by only +2.6% this year in real (inflation-adjusted) terms.

Growth in 2020 is expected to be similar (+2.5%), with only slightly faster growth (+2.8%) in 2021 and beyond. For reference, +2.5% would be the slowest pace of growth in any non-recession / non-recovery year over the past two decades. In nominal terms (including inflation), 2019 growth for these countries is expected to be +4.9%, down from growth of +5.8% in 2018 and +5.7% in 2017. 2020 looks somewhat similar to 2019, and marginal improvements follow in subsequent years.

Nominal growth rates are important to track because they are the most directly comparable figures to those with which marketers and media owners work in determining their own financial plans.

Personal consumption expenditures are holding up better. One factor that has probably helped sustain marketing growth so far this year is growth in personal consumption expenditures (PCE). As consumer spending represents more than half of all economic activity, PCE can be more important to monitor than GDP. Global growth in nominal PCE is holding up as well in 2019 as it did in 2018 at +5.5% in both years. Growth is expected to slow, but only modestly in the years ahead. Of course, changes in inflation levels diminish these figures, with expectations for real (inflation-adjusted) PCE growth at incrementally slower levels each year over the next five years.

Industrial production often correlates more tightly with advertising growth trends. Industrial production (IP) figures are another key set of metrics to monitor, as IP often correlates better with advertising activity than either GDP or PCE (manufacturers generally only make things for sale if they are planning to spend money on advertising them). Weighted against GDP in the markets captured here, we see pronounced weakness in 2019 and 2020 (+1.2% and +1.5%, respectively) relative to 2017 and 2018 levels (+3.5% and +3.1%, respectively). Recovery toward slightly higher levels is anticipated for 2021 and beyond.

Trade and other factors are key sources of uncertainty. As the Organisation for Economic Co-operation and Development (OECD) has pointed out, slowing global trade is clearly dragging on economic activity, and seemingly heightened geopolitical uncertainties are similarly unhelpful. All of this would worsen if the U.S. experienced a recession, although the U.S. economy has remained resilient, likely aided in part by low interest rates and corporate tax reductions, alongside a federal deficit of nearly $1 trillion during the most recent fiscal year. This was equivalent to more than a quarter of all government expenditures and nearly 5% of the overall economy, or more than double its recent trough in 2015.

Mean and median growth rates may tell different stories. We note the difference between mean and median growth rates, with larger economies expected to perform relatively better than smaller ones in the years ahead.

Global Advertising Growth Summary

In this environment, deceleration in advertising growth should be generally unsurprising. Global advertising, excluding U.S. political advertising (large enough to distort global growth rates by +/-1% each year), expanded by +5.7% in constant currency terms during 2018, capping the third year of better than +5% growth and the best year of the current economic cycle. However, 2019 appears set to grow nearly a percentage point slower at +4.8%, and growth is expected to slow by another percentage point in 2020 and 2021. We forecast +3.9% growth next year and +3.1% growth the following year. Growth is expected to range between +3–4% through 2024. Although much worse than recent years, we note that this would amount to a similar pace of growth to what was observed during 2012–2014. We estimate that the total global advertising market during 2020 will amount to $628 billion as we define advertising here, but would likely approach $700 billion on a broader definition that includes spending on direct mail and directories around the world.

Notably, a substantial share of global advertising is now accounted for by digital-first brands that are endemic to the internet. Based upon their securities filings, we can see that Alibaba, Alphabet, Amazon, Booking.com, eBay, Facebook, IAC, JD.com, Netflix and Uber are each now $1 billion+ advertisers, accounting for $36 billion in spending during 2018, up by a quarter over 2017 levels; growth in 2019 was presumably very similar. Adding a couple dozen companies from the next tier of comparable marketers would easily add tens of billions of dollars of additional activity. Combined, this small group of companies accounts for a majority of the world’s growth in spending on advertising. To the extent that these companies tend to take shares of consumer spending from others and do not directly cause the global economy to expand, at some point their growth converges with global averages, resulting in slowing growth in spending as well.

The median growth rate has exhibited sharper deceleration in 2019 than the mean. For the countries we have tracked with consistent data back to 1999, the median growth rate in 2018 was +5.2%. It is expected that 2019 will be +2.1%, followed by +2.7% growth in 2020, with generally slower growth than the weighted average. The difference between the mean and median highlights that growth is driven by a small number of large countries and that the typical small country is experiencing worse growth trends, bringing down the worldwide average. By contrast, median country growth was typically well above the mean as recently as 2013, reflecting a period where much of global advertising growth was driven by smaller countries. This maps to the aforementioned global economic trends.

The U.S. remains the largest global advertising market, with $246 billion in advertising as we define it here, and growing above global averages. With nearly 40% of the world’s total and a still-robust advertising market in 2020 and beyond (at +4–5% growth excluding directories, direct mail and political advertising), the U.S. is helping raise global averages. Our forecasts anticipate a slowing economy as well as the gradual maturation of the digital brands that have driven so much recent growth. On the basis described here, normalized U.S. advertising should slow from +7.6% in 2019 to +5.0% in 2020, +3.4% in 2021, and similar levels in subsequent years.

China’s $90 billion media market is maturing and beginning to slow, but is still more than two times the size of the number-three market, Japan. After many years of rapid growth, China is now solidly the world’s clear number-two market for advertising, with 16% of total media-owner ad revenue, nearly matching the country’s 17% share of global GDP. However, macroeconomic concerns—including issues referenced above and a general maturation of the Chinese advertising market—are weighing on growth

this year and beyond. We forecast growth of only +3.7% in 2019 and +1.4% in 2020. Similarly, low levels of growth are anticipated in subsequent years despite faster levels of economic expansion for the overall Chinese economy. Japan remains a solid number three, with 7% of global advertising ($41 billion in 2020) and 6% of GDP, but growth is expected to be tepid there as well; +1.7% growth in 2019 is expected to be followed by +1.8% in 2020, and closer to +1% in subsequent years.

The U.K. is still growing at a remarkably fast pace. Among larger advertising economies, the U.K. and the U.S. stand out for their healthy growth expectations. For the U.K., it is a feat made more remarkable given how much uncertainty has persisted over the past three years since the Brexit referendum. Five years ago, the U.K. was essentially tied with Germany as the number-four market for global advertising, but since that time the U.K. has grown by +44% while Germany has only expanded by 7%. The factors driving the U.K. are likely similar to those that have helped make the U.S. a strong market, including a substantial presence of digital brand spending as well as the expanding availability of ad inventory (in digital environments, primarily), which help make it possible for smaller marketers to use media. Although we do expect growth to taper off from the high-single-digit levels we have observed since 2014, solid mid-singles (+6.7% in 2020 and +5.5% in subsequent years) are now expected.

Germany and France are growing at below-global average rates; so is much of the rest of Europe. Brazil should be above average, while India is the world leader among larger media markets. Germany and France have certainly underperformed U.K. and U.S. levels of advertising growth in recent years, but remain in the number-five and number-six positions for now. France appears set to grow at a slightly faster pace than Germany, with a +2.8% five-year compound annual growth rate (CAGR) through 2024 for France versus a +1.6% CAGR for Germany. By 2024, Germany should still be the fifth-largest advertising market, but France will likely be overtaken in importance by both India and Brazil, currently number six and number seven, respectively. Brazil should grow at a solid +4–5% level through 2024 after a soft 2019 (we believe the ad market there grew by only +3.3% in 2019), but India should continue to be stellar, maintaining double-digit growth rates (we estimate +12–13% each year from 2020 to 2024, similar to 2019 levels). Of course, inflation is an issue for both of these countries, negating much of Brazil’s growth. However, in India the effect will only mean that real growth is in high-single digits rather than low doubles.

Canada and Australia are similarly sized markets, but they are growing in different directions. Canada and Australia round out the world’s $10 billion+ ad markets in 2019, with Canada expected to grow slightly faster over the next five years and growth likely largely tied to the health of its southern neighbor. Australia’s trends will likely differ, as we see at the present time with that country’s economy soft and facing a real risk of recession for the first time in decades. The Australian ad market was likely only stable in 2019 versus 2018 and probably grows only slightly in 2020, for a +2.0% gain expected next year. By contrast, Canada is expected to grow +5.0% in 2019, and should slow toward a high 3%+ growth level next year and in subsequent years. Overall around the world, 14 territories are expected to decline during 2019, with Italy the largest among them: We anticipate Italy will fall by -0.4%. Other large markets among this group include Mexico and Switzerland, which are expected to decline by -4.6% and -8.0%, respectively. Next year, fewer markets are expected to decline, with Switzerland the most significant among them

Life Insurance Council announced the launch of the Indian insurance industry’s first joint awareness campaign titled ‘Sabse Pehle Life Insurance’, stressing upon the need for life insurance.

Said S N Bhattacharya, Secretary, Life Insurance Council: “There is a need to make all Indians aware of the fundamental need of life insurance. Many a times Indians buy life insurance for peripheral benefits, without really understanding why it is imperative in our lives. We hope the larger Indian population will identify with this thought provoking campaign and be encouraged to opt for life insurance as their primary protection instrument.”

Added Prasoon Joshi, Chairman, McCann Worldgroup – Asia Pacific, CEO & CCO McCann Worldgroup India: “The campaign is trying to inculcate responsibility towards financial planning at an instinctive level. ‘Sabse Pehle Life Insurance’ is a simple, relatable and culture-rich idea that people can easily identify with.”

It took us some time to reach him. And when he didn’t respond to our messages, we sent him a set of five questions. A little while later, he texted back saying: Call me. Which we did. Here goes the transcript of a telecon – somewhere around 8pm on the Eventful Tuesday.

Sorry to be so persistent.

No, no. Not at all. You know, I was just not taking your call, but you can imagine there is so much of interest in this. I have just signed a whole bunch of contracts to make sure that I cannot talk too much, but go ahead. Ask me.

So what happened. It seemed to be smooth sailing?

Honestly, it’s been an incredible year. But I’ve been wanting to move on for some time and I took the call some time back to make the move. It’s as simple as that. People are speculating a lot of things on audit and all of that. Like, nobody leaves because of an audit! You know that. Right?

I’ve spent now 17 years with the group and nobody has made real value for themselves without doing something of their own. So, this is my time.

Clearly this was thought-out move

These are always thought out things, no? For everybody else it seems like this is new or surprising, but obviously it has been in the works for a long time.

Hmm. You wouldn’t have taken a decision just like that.

Yes. Even from the group’s perspective, they’ve got two leaders and ultimately they would have to get into a country model, right? And if my choice was to move on and do other things then they have to exercise what option is there with them, no? They have to do that.

So till when are you with the group?

So like the way these things work, today is the last day. This is how all these things work…

True.

Because if I’m starting on my own, I cannot possibly continue, right?

Yeah, it’s fair to both parties.

Absolutely and that’s what it is. So, you will hear a lot more news, in the next few days. Hold on, as you can hear from the background. Lots of celebrations here! (as we started the conversation, there was a fair bit of ambient noise, but it died out soon hereafter)

Yes, I have heard about some more people (from the group) joining you.

See, that is up to those people. I’m starting something/ It is up to those people what they want to do. I mean, I cannot comment on other people

So what is it going to be? What are you looking at doing? Similar kind of an advertising agency… an area that you know so well.

The objective is to create the most creative company in the world. That’s it. Period. That’s the objective. Now, I’m going to go ahead and create the most creative company in the world.

As you look back at your stint at Leo Burnett and Publicis Communications, what would you say were your most memorable moment… something that you treasure?

Honestly, my most memorable moment is creating the Bajaj V piece. That’s from the work perspective but from a business perspective, the fact that Prodigous is the largest production house and the fact that it didn’t exist two years back is really what I look back at as incredible moments.

Since you mentioned you just signed some contracts to not speak, is there a restriction on you taking away some clients (to the new venture)?

There are always contracts in play and like I keep saying, “The world is an oyster right now,” and there are so many opportunities. When you look at the environment and there is so much change, there cannot be a better moment to start. When you look at the story of Leo Burnett, he started the company during the Great Depression, 1935. I think I have a better moment.

Any unfinished agenda at PubComm?

Not at all. I’m very satisfied with my stint and this is the perfect moment to close this chapter and start a new one.

By A Correspondent

By A Correspondent

It took us some time to reach him. And when he didn’t respond to our messages, we sent him a set of five questions. A little while later, he texted back saying: Call me. Which we did. Here goes the transcript of a telecon – somewhere around 8pm on the Eventful Tuesday.

It took us some time to reach him. And when he didn’t respond to our messages, we sent him a set of five questions. A little while later, he texted back saying: Call me. Which we did. Here goes the transcript of a telecon – somewhere around 8pm on the Eventful Tuesday.