Courtesy GroupM

As part of the ‘This Year Next Year’ report presentation on Monday, GroupM captains presented a report on trends impacting the Indian advertising industry.

Said Karthik Nagarajan, Chief Content Officer, Wavemaker India: “It has been an interesting year for digital marketers as the nation-wide lockdown brought about exponential growth in certain trends which were already on the up – whether immersive experiences like gaming, the rise of audio or influencer marketing. People have started gaining interest in localized content and now OTT – audio or video, has become a major part of their entertainment. We are also moving towards an era of fragmented social media, where creators will take precedence over communities. Also, with the consumer becoming more conscious by the day, we will see empathy becoming a constant thread in brand communications.”

Sharing some light on the trends, Bharat Khatri, Country Head, Xaxis India added: “Brands are aggressively looking at deploying new tools, data & cloud infrastructures which has resulted in the acceleration of digital transformation post Covid-19. With the increase in demand for different platforms, creativity and localized content, the advertisers have plenty of opportunities to reach consumers through engaging via different audio/video formats & achieve real outcomes in a device agnostic world. In short, the brands are continuously looking out for new ways to reach out to connect with their consumers and make the relationship stronger. We also see that Gen Z has been making a lot of their decision basis social media platforms and this coincides with the rise in new age ecommerce platforms.”

Here are the 10 trends:

1) From Carefree To Conscious – The Great Shift In Consumer Behaviour

• During the lockdown, there was a 42% growth in searches to know “what’s normal” forbody stats like BP, body temperature and blood sugar

• Browsing content on healthy cooking went up by100%

• All this point to a marked change in what the user is seeking, towards self-preservation and wellness

• Thisis also further accentuated by over 52% rise in content consumption on pets and a 70% increase in searches related to Yoga

• This behaviour change will also imply how they look at Brands and consumption at large – Consumers are also more likely to embrace brands who showcase empathy and care aboutthe larger world /environment

• This is presenting an opportunity tobrand

:: Back of the pack = front of thepack

:: Highlighting goodness in every possibleway

2) Everything Is Becoming Hyperlocal

• What is happening in your immediate surroundings – whether town or district istaking precedence over what is happening in the country or the World

• Oneof the biggest indicators of this is the surge in regional language news & content during the lockdown

• We are seeing similar trends in digital consumption as well in terms of the rise of more regional news and content consumption– in platforms like Daily Hunt and share

• This also is happening simultaneously as our capability to sharp shoot communication has increased– for example, our ability to do Pincode-level targeting, thanks to multi-faceted data

points on the audience or targeting based on distribution pattern or market share in specific locations.

• There’s saying that- Every 15-20 km, the language, dialect, music, food, … everything changes in India

• Brand owners have opportunity to leverage this and drive precision @scale

3) Driving Up The Subscription Bandwagon

• 2021 would “once-in-for-all” smash the adage that “Indians don’t pay for content” and drive up thesubscription game for Sports and other forms of quality original It’s creating a direct 2 consumer opportunity.

• Thereare many OTT player who has achieved their subscribers target 12- 18 month ahead of This is not limited to live sports and premium video content – there’s the start of a similar trend in news, audio content and premium domain-specific content in small ways.

• Platformslike Substack helping talented Journalist reach direct to their readers and monetize their content.

• 2021 is also going to be an interesting year for sports – 2020’s loss, in terms of sports events, is 2021’s gain. Global sporting events like Euro 2020 and Tokyo 2020 are due to happen this year. Add to this, local favourites i.e., IPL 2021 (within 6 months of its previous edition) and ICC T20 (which would be hosted in India) and you’ve quite a field day for Indian sports fans and broadcastersalike! an Indian Sports Fan as s/he would be battling questions on what to subscribe, when to subscribe, how long to subscribe, where to watch and many such conundrums

• Interesting time ahead for content industry and distributionplatforms

4) Gaming & Esports Growth – More Than Time Pass

The next generation of entertainment is immersion and engagement while gaming will be a natural winner there

• 5G

• VR

• Gaming

Gaming will become not just about time spent but also a cultural destination. The nature of this entertainment is not a lean back but a more immersive one. Music concerts and other experiences will also be activated on esports platforms. A handful of businesses can talk positively about 2020 and COVID- 19… One such benefactor is gaming and esports. In peak lockdown during Apr’20, there was an 11% increase in users per week and has seen a rise in the number of gamers where 66% of new gamers are females and 56% of new gamers are above the age of 45. Now gaming as an industry has evolved in multiple ways too. Most companies in this industry are looking to create platforms that will be central to an individual’s life where activities, like shopping, socializing, events (especially esports) can all be done in virtual and interactive ways. During the lockdown, esports live-stream viewership grew by 61% and 66% in week 1 and 2, respectively. These are great signs, considering that despite the majority of the on- ground esports events getting pushed in 2020, the gaming fans have held their own. With 2020 contributing immensely to gaming habit formation; for 2021 to be the year of esports, organizers need to focus on building career opportunities starting with improved prize money pool.

5) Platforms Will Become Creator Led Than Community-Led

The entry barrier for social platforms used to be the network effect. a.k.a how many of my friends/people are there on the network. As we move towards an ecosystem where people join platforms more for the experience and creators on it, this barrier will be lowered significantly. We are possibly looking at 4-5 different platforms with a 100 Million plus user base, not far from now

Influencer content for brand building will sustain but a majority of categories will move towards a performance mindset for advocacy. Newer platforms, driven by creators already have seamless commerce features built-in. This will spur content-to-commerce in a big way in 2021. The journey from platform-based advocacy to an integrated strategy for brands will now scale to include commerce as well. This will also bring in more industry guidelines on influencers disclosing brand partnerships.

6) Immersive audio becomes a cultural movement. Finds a loyal audience across age demographics

As we predicted last year, audio has truly made its comeback in style. Platforms like Clubhouse are seeing great traction and audience for podcasts has grown manifold in India in 2020 and the MAUs are already where social media was a few years back. The IAB has just released technical guidelines for podcast measurement in the US. In India, standards and guidelines will emerge and be solidified, as we are reaching critical mass. Given the proven efficacy of audio on brand recall, this will be extremely critical for brands looking to make cultural interventions.

7) Digital Transformation – ROI To Opportunity Cost

Leaders are aggressively deploying new tools, data & cloud infrastructures, the digital transformation process got accelerated post-Covid. This will help create new age “Marketing Digital Infrastructure “and replace old tech which was becoming a barrier to fast-track digital transformation. Advancing towards a P3PC (post-third-party cookies) has accelerated the long-term data strategies plan to own the consumer where brands have already started to deploy CDPs (Customer Data Platforms) to transition from segment audience data approach to individual consumer profiles. The industry will continue to see this trend in both advertiser & publisher ecosystem on putting more focus towards 1st party data activation powered with contextual targeting.

8) Streaming Wars- In a Device Agnostic World

2020 pandemic turned out to be an opportunity in crisis for OTT industry in India. Connected TV is simply becoming the new TV. It is the way large segments of consumers will access premium content. As we see by its current use for reach extension, CTV is a medium through which mass brand messaging can continue going forward. The fact that it is more targetable and measurable than ‘old TV’ enables marketers to elevate and personalize their messaging when appropriate. So, it can be the best of both worlds. Growth in SVoD may sound bad news for advertising, as largely SVoD platforms are ad-free. But in India, the home- grown broadcaster & independent OTTs at an early stage only has adopted hybrid multi-tiered monetization model by giving the audience the choice of both free, ad-supported content & premium subscription offering. This is giving advertisers plenty of opportunities to reach consumers through engaging video formats & achieve real outcomes in a device-agnostic world. In 2021, this advertising channel will continue to have a lion share in programmatic spends & will also bring incremental budgets from the traditional/linear TV pie. With increased spends, we will also see advertisers adapting to more evolved, efficient & effective programmatic buying methods like PMPs (Private Market Place) to get a unified consumer view & thus maximizing the ROI from video spends.

9) Connected Commerce- The Customer-Convenience Imperative

E-commerce platforms have become an indispensable digital channel to reach target audiences and influence sales. Marketers will need to think like DTC brands – embracing emerging technologies, customer service obsession and adaptive messaging to get closer to their consumers. DTC brands have excelled at creating 1:1 relationship with their consumers since they have closed-loop measurement within their customer journeys. Shoppable Ads are on the rise as Genz are deciding on social media videos. These new media formats play an important role in cultivating better outcomes overall for an advertiser. In 2021, we will see a big shift of spends happening from current market-leading DSPs especially in display channel towards the new age e-commerce DSPs like Amazon, Flipkart, Paytm. Categories, where spend shift, is quite inevitable are FMCG, BFSI, Grocery, Apparels, Health & Personal care, as ecomm DSPs offer end to end marketing funnel solutions with efficient ROAS.

10) Bringing Creativity Back Into Digital Advertising

The industry is recognizing that creativity is the first step to grabbing attention and enhancing the influence, and media buying should aim to match advertising messages with real consumer behaviours, not just attributes. Brands need to embrace AI to boost personalization at scale. It is like feeding an algorithm with historical & real-time data and then letting AI perform analysis, build & serve the user hyper-personalized message. Traditional personalized creative tools were built for targeting customer personas or profiles, where each profile used to represent a category of consumers, however, in case of AI personalization tools it is like engaging with each customer as an individual profile. With increased social commerce share, AI-based hyper-personalization engines will be the need of the hour, as it will improve both ROI & customer experience.

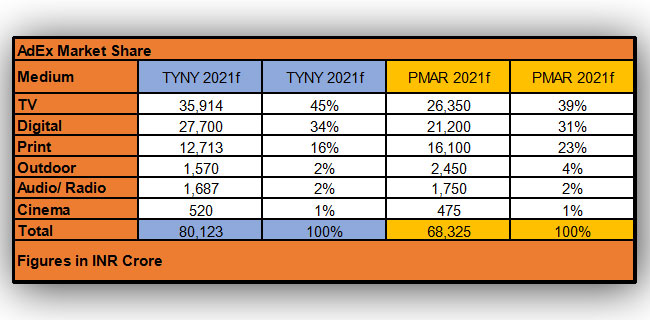

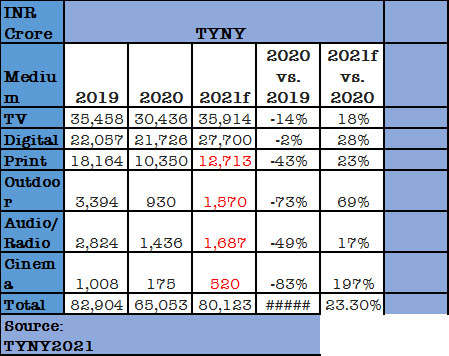

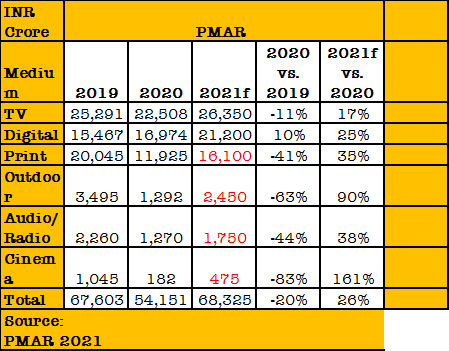

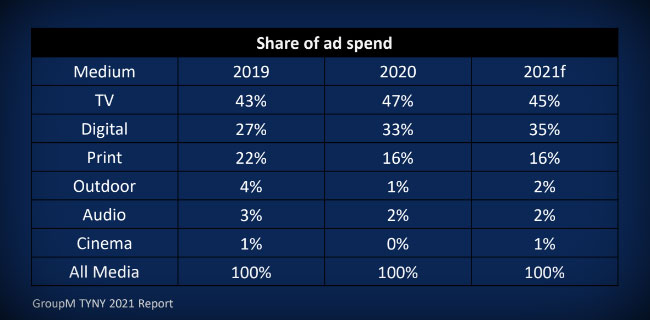

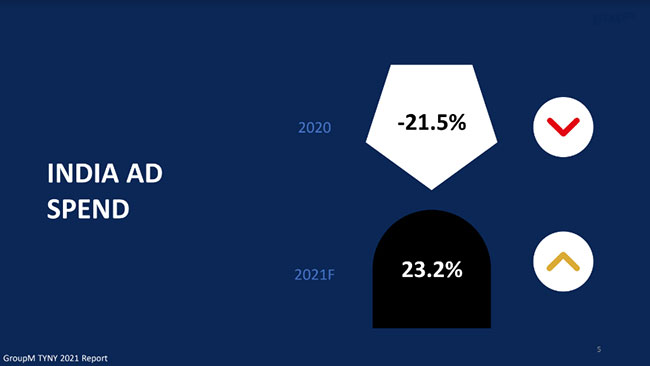

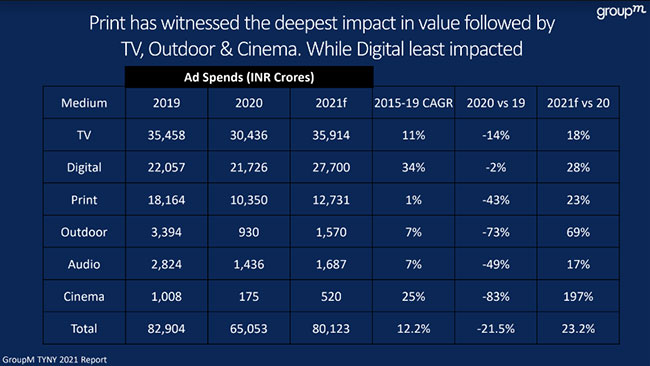

Like every year, last week we saw the release of both This Year Next Year 2021 (TYNY2021) by GroupM and Pitch Madison Advertising Report 2021 (PMAR2021) by Madison Media. Both agreed that the pandemic year 2020 was a disastrous one for the Indian Media and Advertising Industry, when the overall AdEx dropped by 20% (PMAR2021) to 21.5% (TYNY2021) from the 2019 level. Both have predicted better days in 2021 with the overall AdEx growing by 23.3% (TYNY2021) to 26% (PMAR2021). According to PMAR2021, the predicted AdEx INR 68,325 crore in 2021 will touch the AdEx INR 67,603 crore in 2019. According to TYNY2021, the forecast for 2021 is INR 80,123 crore, which falls short by 3.35% from the AdEx in 2019 which was INR 82,904 crore.

Like every year, last week we saw the release of both This Year Next Year 2021 (TYNY2021) by GroupM and Pitch Madison Advertising Report 2021 (PMAR2021) by Madison Media. Both agreed that the pandemic year 2020 was a disastrous one for the Indian Media and Advertising Industry, when the overall AdEx dropped by 20% (PMAR2021) to 21.5% (TYNY2021) from the 2019 level. Both have predicted better days in 2021 with the overall AdEx growing by 23.3% (TYNY2021) to 26% (PMAR2021). According to PMAR2021, the predicted AdEx INR 68,325 crore in 2021 will touch the AdEx INR 67,603 crore in 2019. According to TYNY2021, the forecast for 2021 is INR 80,123 crore, which falls short by 3.35% from the AdEx in 2019 which was INR 82,904 crore.

By Brian Wieser

By Brian Wieser