By Our Staff

Earlier this week, GroupM unveiled its global end-of-year forecast of adspends. The WPP advertising clongomerate also publishes its India-specific numbers, so we are not doing a detailed look right now, but here are highlights of the This Year Next Year study, and a special focus on television thereafter.

Excerpted from the GroupM report:

The overall industry forecast:

• 2021 growth: 22.5% (excluding U.S. political advertising), an upward revision from June’s prediction of 19.2%.

• 2022 growth: 9.7% (excluding U.S. political advertising), an upward revision from June’s prediction of 8.8%.

• Many underlying trends appear to be disproportionately concentrated in the U.S., the U.K. and China, which together account for approximately 70% of all the industry’s growth, despite making up about 60% of the total market.

• Looking at the top 10 advertising markets over the next five years, growth should get back to the mid- to high-single digits:

° France, Germany, Australia and the U.S. all poised to grow in a range of 4-5% annually, on average, over the next five years.

° India, the U.K., Brazil, Canada, Japan and China are forecast to grow between 6-8% annually, on average.

Here are the major areas considered in detail as we reach the end of 2021:

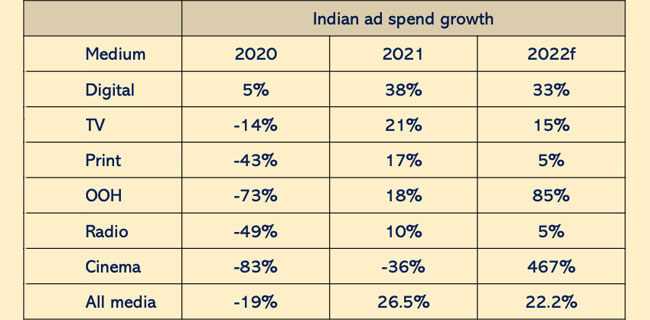

• Digital advertising: likely end 2021 growing by 30.5%, up from June’s forecast of 26% growth.

° Digital advertising accounted for 64.4% of all advertising in 2021, up from 60.5% in 2020.

° Alphabet, Meta and Amazon account for 80-90% of the global total.

• Television advertising:forecasted to grow by 11.7% in 2021, up from June’s estimate of 9.3%. Given 2020’s decline of 13.7%, the industry is not expected to return to 2019 levels until 2023.

° Subsequent years will be roughly flat—up 1-2% per year through 2026—for television advertising in most major markets around the world, as the largest advertisers continue to incrementally shift spending.

° Overall, Connected TV+ will account for about 10% of total TV advertising in 2022 ($17 billion of a total of $171 billion) and is expected to double by 2026.

• Audio advertising: Expectations for audio are that it will grow 15.6% in 2021 and 6.4% in 2022. In subsequent years, we assume a reversion to historical trends: largely flat.

• OOH advertising: Outdoor advertising is expected to grow 17.1% in 2021 and 14.9% in 2022. In subsequent years, we assume a reversion to historical trends: mid-single digit growth.

Now, a superficial read of the data included in This Year, Next Year might leave one with the impression that because 64% of the world’s advertising revenue is generated by digital media and 21% goes to TV, that marketers are allocating 64% of their budgets to digital media and 21% to TV, on average. This would be a mistaken interpretation, because many advertisers—especially small ones and those whose businesses operate entirely online—often allocate all or nearly all of their budgets to digital media while large businesses typically allocate higher shares of their budgets to television.

For smaller businesses, a high digital skew could occur because digital media’s precision targeting capabilities and automated sales platforms are uniquely capable of absorbing advertising budgets that are measured in hundreds or thousands of dollars. Larger advertisers that spend 100% of their budgets online might typically be doing so because their operations are entirely transactional or direct-to-consumer. For them, too, digital media platforms offer unique advantages connecting a budget for advertising with a tangible near-term outcome and the potential for active “growth hacking” strategies, which can work well, at least up to a certain scale.

However, the world of media also includes businesses whose marketing goals are set around brand-building. They often do this by associating their products with top-tier video-based content or otherwise focusing on goals that are not most efficiently achieved through digital media. Further, for many, the combined use of different types of media can be synergistic in ways that are difficult to quantify. For example, we can reasonably assume that a strong brand should drive better performance of an e-commerce-focused advertising campaign versus the alternative of having a weak brand, although the factors that can drive a brand to accomplish this outcome can involve uncountable numbers of variables over many years or even decades

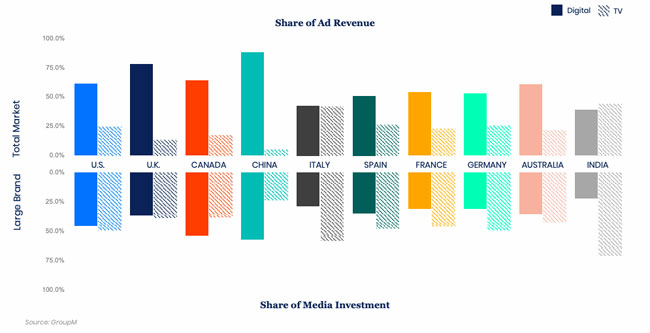

Given our own focus as the world’s largest agency group, servicing larger brands primarily, we wanted to better assess the typical large advertiser media mix. To do this, we looked to GroupM’s own data to find useful illustrations of the ways in which different marketers allocate their budgets around the world. In studying these trends, we primarily focused on two dominant groupings of media, television and digital platforms, and then limited our analysis where possible to a subjectively defined group of large marketers on a like-for-like basis (meaning that we included only the same marketers in each period) within each of our Top 10 markets.

The most accurate benchmark for large brands to consider is that in a typical large country during 2021, a large brand is allocating 47% of its advertising budget to television, including digital video extensions, and 35% to internet-based media, excluding those digital video extensions. For reference, in 2019, television typically accounted for 48%, while digital media typically accounted for 28%. These figures reflect wide gaps between the shares of revenue that media generates, with the difference driven by the wide range of brands that spend money in a given territory.

For individual marketers, we recognize that this data may provide useful information about what other marketers are doing. However, the goal should not be to mimic them. Instead, we present this information to help spur questions about the right allocations for your brand. Well-developed media plans account for a marketer’s unique goals, apply some creativity to achieving those goals and consider what worked well for others who faced similar circumstances. It is our hope that the data presented here leads to the creation of more media plans that meet these criteria.

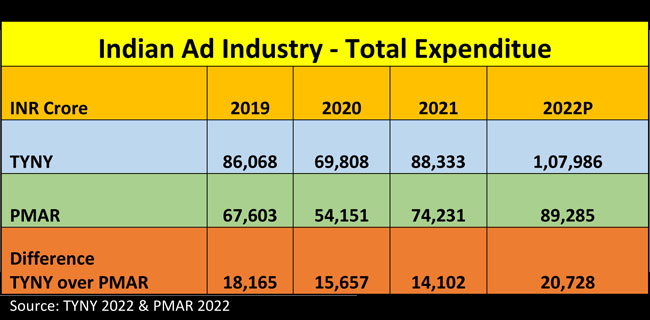

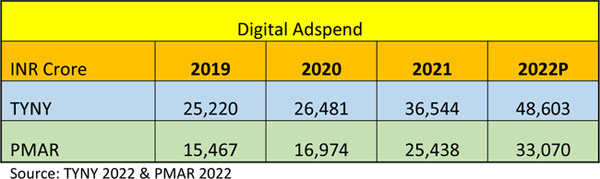

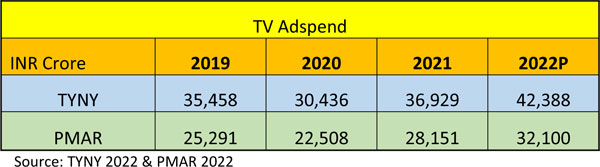

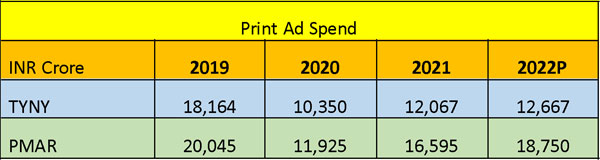

Last week, both GroupM’s This Year Next Year (TYNY) and Madisons Media’s Pitch Madison Advertising Report (PMAR) got released and their basic findings have already been reported by all business and trade media. The general mood in the advertising industry is exuberant as both the reports have confirmed that AdEX zoomed in 2021, by 37% as per PMAR and by 26.5% as per TYNY in spite of the third wave of the pandemic. In 2021, India was the fastest growing market in the top 10 countries, ranking 9 globally and ranking 5 on incremental ad spend predicted for 2022.

Last week, both GroupM’s This Year Next Year (TYNY) and Madisons Media’s Pitch Madison Advertising Report (PMAR) got released and their basic findings have already been reported by all business and trade media. The general mood in the advertising industry is exuberant as both the reports have confirmed that AdEX zoomed in 2021, by 37% as per PMAR and by 26.5% as per TYNY in spite of the third wave of the pandemic. In 2021, India was the fastest growing market in the top 10 countries, ranking 9 globally and ranking 5 on incremental ad spend predicted for 2022.

Journalist-turned-communications and marketing professional Priyanka Mehra has joined Comvergence Worldwide as Regional Director – South Asia.

Journalist-turned-communications and marketing professional Priyanka Mehra has joined Comvergence Worldwide as Regional Director – South Asia.