By A Correspondent

Okay, we’ve cheated. We know GroupM publishes a propah India-specific report in Februrary, but we’ve noticed over the years that the global This Year Next Year report released in Decemeber is also fairly detailed.

So while we carry the report now, please do note that there may well be a full-blown one in the coming months. So here’s the report:

“The IMF expects real GDP to grow 7.4% in 2019 (12.1% nominal), driven mainly by services and private consumption; manufacturing and agriculture are likely to see moderate and low growth, respectively. Bank balance sheet repair and GST reform is likely to start yielding results sometime in 2019, accelerating a reviving investment cycle, but downside risks remain: continued global trade conflicts and high oil prices are likely to impact the exchange rate, trade deficit, liquidity and inflation.

Auto advertising growth is expected to be high, as car, scooter, luxury bike and commercial vehicle segments will see good sales growth in 2019, driven by urban demand and infrastructure spending. Rural-led motorcycle sales will be monsoon-dependent.

BFSI adspends will be moderate to high, as bank adspends remain subdued but insurance and financial services spend robustly to expand penetration, with the government-led health insurance scheme also providing a boost to growth. Digital payments are expected to touch $500 billion by 2020, and insurance to be a $280 billion sector by 2020.

Consumer durables ad monies will see moderate-to-high growth: low penetration in consumer appliances, shorter replacement cycles in consumer electronics, robust replacement demand overall and unexpected/extreme weather – hotter summers, hazier winters – will all contribute to spends.

E-commerce adspends will grow fast: a report cites the sector to touch $100 billion GMV by 2020, while Morgan Stanley predicts it to touch $200 billion by 2026 and expects ~50% of India’s internet users to have matured by 2019/20 (five years or more of internet use). Online shoppers are expected to increase from the current 14% of internet users to 50% by 2026. Strong consumer expenditure growth should lift Retail advertising in the order of 12-14% year over year between 2017 and 2020, and the explosion of modern retail, expected to nearly double in size between 2016 and 2019, will drive ad monies.

FMCG adspends will grow fast, as key drivers remain strong: expanding rural penetration, strong rural demand supported by increased welfare spending in a busy election year in 2019, and steady urban sales and growing interest in luxury and health-wellness products.

Services ad growth should be strong, as the major segments of travel and hospitality, health care and logistics are all expected to perform well in 2019. The travel market is tipped to reach $40 billion by 2020; logistics are expected to hugely benefit from GST.

Telecom ad growth will be driven by mobile handsets. 2017 saw 288 million shipments (124 million of which were smartphones). The IDC predicts mid-teen growth in 2019-2020, led by low-priced handsets. Telco spends will be conservative, as incumbents face continued pressure on margins due to intense competition – likely to continue till ~2020.

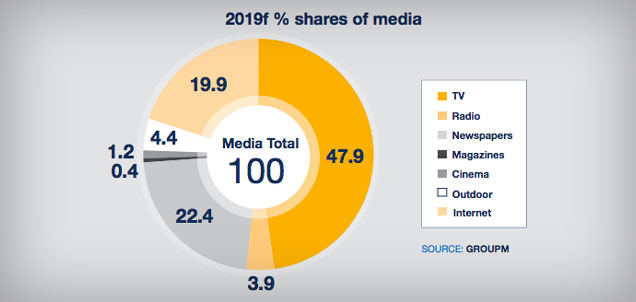

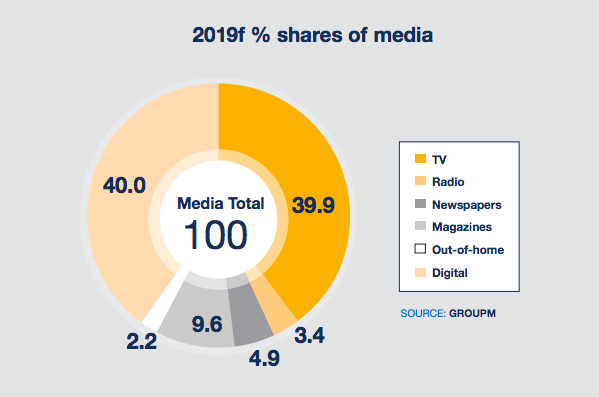

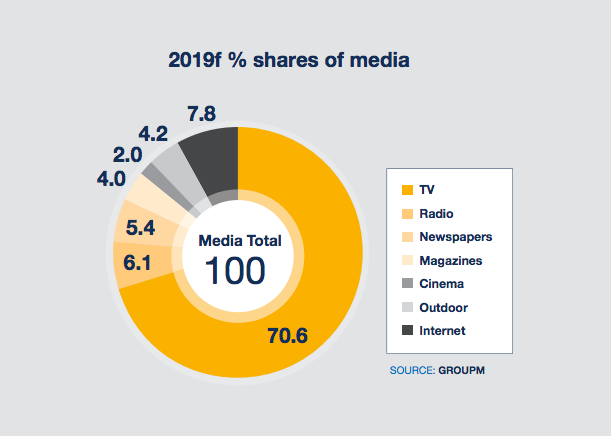

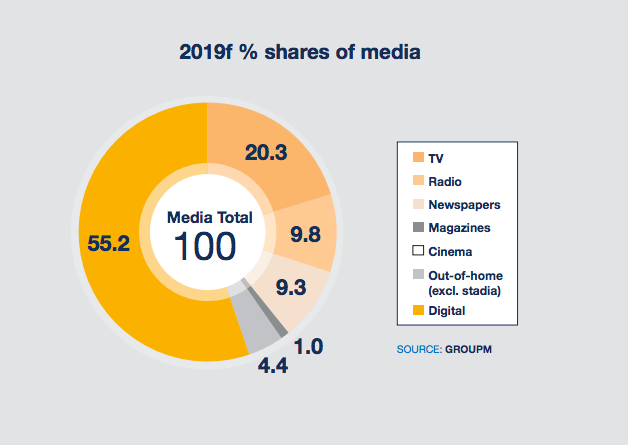

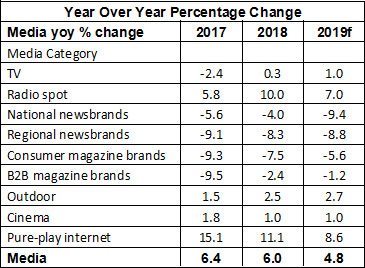

TV: sports and elections will drive advertising. Print to grow at a slower rate, losing share to digital; election spending will provide some relief. Radio is expected to do well from auto, mobile handsets and a revival in FMCG, real estate and government spends. Cinema & outdoor will continue to grow, as technology adoption improves ad visibility and from the growth of organised retail. Digital: will see high double-digit growth backed by video (with OTT players/AVOD gaining traction) and other premium inventory.â€

And here’s the final analysis:

“It will be a toss-up with China for 2018, but this year and next India could remain the world’s fastest-growing large economy, with only the Philippines on its heels. Despite two successive quarter-point repo rate rises in 2018 (to 6.5%), the rupee has depreciated 10% versus the US dollar in the year since our December 2017 forecast, in line with the average of the currencies in our country set. The rate rises were a response to CPI creeping up, and there may be more to come. This reflects the health of India’s domestic demand: like the USA, it is a relatively self-sufficient, low-trade economy, which is a strength when global trade is contracting. HSBC predicts India’s consumer demand growth will peak at an impressive 9.1% (real terms) in 2018 before moderating to around 7%, which only China is likely to beat. However, no country is immune from the demand-sapping effect of pricey oil and a runaway dollar, which would only encourage capital flight from the developing world back to the rising-rate USA.â€

And here’s how India fares in the global perspective:

India’s prospective 2019 growth this year is the same order as Australia, Russia and Brazil combined, even though India’s ad economy is only a quarter of the others’ combined heft. Such is the arithmetic of 14% ad investment growth with its roots in 7% real growth in India consumer spending (after 9% in 2018).