By John Nendick

Is the customer best placed to understand what they want? Their point of reference often is defined by their experience and influenced by what they know, so how aware are they of everything that is possible?

Today, the potential of media and entertainment (M&E) companies to understand their customers is greater than at any time in history. Successfully capturing insights from an array of sources and translating them into viable products, services and business models will go a long way in defining the leaders of today and the leaders of tomorrow.

Generation Z is different from anything we’ve seen before. Much has been said about Millennials, but Generation Z is the first to be digitally native. They are the first to grow up using social media, mobile technology and mobile video. Given that YouTube was only founded in 2005, most Millennials remember a world without mobile video — most of Generation Z do not.

Technology aside, Generation Z also has refreshingly different attitudes. They are more entrepreneurial; they grew up with search engines and like to discover content for themselves. They also like to be involved in the process, contribute to the solution and be more immersed in experiences.

The step change for M&E companies from traditional business-to-business (B2B) models to direct consumer relationships is focusing attention on the need for more granular insight. Nowhere is this more apparent than in their efforts to understand the unique behaviors and preferences of Generation Z.

Responding to changing consumption models means a rethink for M&E leaders about new business models and new investments. To better understand where investments are being made, EY conducted an analysis of two groups: today’s leading telecoms, technology and media companies, and the next generation of companies in those sectors.

Some key findings include:

Digital advertising has created a dilemma

:: Digital advertising, a top-30 focus area of the industry, has lost as much as US$8 billion in revenues.

:: Half of the loss derives from “nonhuman traffic†— fake advertising impressions that are neither generated by real advertisers nor received by actual consumers.

:: The other half comes from a variety of factors, including ad blocking and content infringements, such as the sharing of passwords.

Unicorns and decacorns are driving investments

Our analysis focuses on 60 unicorns. These are the world’s most valuable, privately held companies founded in the past 10 years with a market valuation of US$1 billion or greater. Decacorns have a market valuation of US$10 billion or greater.

Across telecoms, technology and media, the 60 represent US$143 billion in value and a broad mix of services, business models and subsectors. They are digital first and adept at scaling new service offerings and at accessing new distribution channels, customer and audience segments.

Incumbents are responding, at least in part, by taking positions in unicorns and creating a tangled web of investments. Of those on our unicorn list, Vice Media has received two rounds of investment from Disney. NBCUniversal holds stakes in BuzzFeed and Vox Media. NBCUniversal’s parent, Comcast, which also has a stake in Vox Media, is an investor in wearable tech company Jawbone, neighbourhood social network Nextdoor and fantasy sports provider FanDuel.

M&E executives are confident in the broader economy

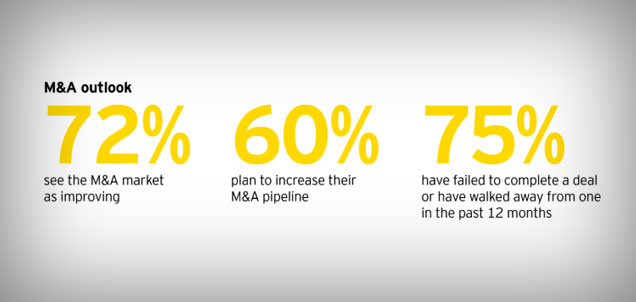

The rise of unicorns illustrates the relentless treadmill of disruption, and yet there is a newfound confidence among M&E executives about the economy and the wider investment climate.

Eighty-one percent of M&E executives say the global economy is improving, compared with 52% who said that a year ago. In the year ahead, the global M&A market is forecast to remain buoyant, with 73% of executives indicating it will improve, up from 49% last year.

The target areas for investment are a mix of emerging market powerhouses, such as China and India, and more mature media markets, such as the UK, Australia and the US.

The Internet of Things (IoT) is coming of age. The connected home, connected car, connected store and wearables already are a reality that will only grow. By 2019, the number of connected cars in the US will almost triple to 60 million. Estimates vary, but 30 billion installed IoT units are forecast to be installed by 2020.

For M&E companies, IoT offers huge potential. In its simplest form, IoT is the proliferation of sensors to capture vast and varied data about customers: their behaviours, emotions, sentiments, physical reactions and well-being. Yet, data is only part of the picture.

Three ways M&E leaders can invest today for success tomorrow

The next step is to make sense of it — to uncover what customers really want. And even then, it is the action it engenders that finally turns the data into a business model. In plain terms, technology and gadgets are not enough to capitalise on the IoT, but the timely, targeted and relevant delivery of content creates experiences that bring the IoT to life.

1. Double down on data

Generation Z is the most willing to surrender personal data, albeit on the assumption of a value exchange. M&E leaders will take advantage of this.

They will take this data and, based on predictive insights with more targeted content and advertising, they will distill it into more tailored experiences.

The competitive advantages available to those who gather data are increasingly apparent to cable operators such as Comcast. They know the set-top box, which was originally envisaged as a one-way distribution device, is really a treasure trove of data and insight about their subscribers.

Comcast collects viewing data from almost 90% of its subscriber base, with more advanced set-top boxes collecting even richer information. By adding set-top-box data to existing customer relationship management information, web browsing histories and third-party data, Comcast builds a picture of its subscribers that is sufficiently granular to open up new revenue opportunities.

Comcast can monetise it themselves through personalised advertising systems like their Adtag and Adcopy solutions, but it can also make data available to third parties, such as ratings agencies, content providers and advertisers.

2. Tell stories and build experiences

Storytelling is important to Generation Z. They care about seamless experiences and value engagement that builds into ongoing relationships rather than just transactions. M&E companies that understand this will utilise the array of connected devices to which customers have access, in an effort to tell integrated and connected narratives.

In February 2016, Sky launched its Sky Q box in the UK. There are parallels with Comcast’s Xfinity.

It is a new-generation set-top box that effectively operates as a Wi-Fi hub, bringing together multiple connected screens and devices throughout the home. Packed with 12 tuners, the new set-top box creates a connected home, enabling seamless transition from room to room and from device to device. It allows customers to control of all their connected devices, not just Sky devices, through one integrated experience.

3. Look for partnerships (acquisitions)

Their investments in unicorns illustrate M&E leaders’ understanding of the need for partnerships and acquisitions, which provide the fastest route to expanding capabilities, accessing new business models and achieving scale. Media and entertainment companies are reaching out to work with technology and telecommunications players, cybersecurity services, venue owners, automotive companies, health providers and appliance manufacturers.

Summary

The rise of Generation Z — now 25% of the US population — is forcing media and entertainment companies to rethink whether they know what their customers want. In response, companies can look to utilise data, tell stories and look for partnerships.

John Nendick is Global Technology, Media & Entertainment and Telecommunications Deputy Sector Leader at EY. Repubished with permission from EY (Ernst & Young)