By Indrani Sen

A lot has happened in the last one week, when we speculated about how Covid-19 might affect the AdEx in 2020. As India fights against all odds to stop the accelerated outbreak of the virus through community transmission with the entire country is facing partial to total lockdown, there is no doubt that our economy will be badly affected like many other developed and developing countries. So, along with the rest of the world, India will be getting into a severe recession for the rest of the year. The point we need to speculate, will there just be a dip in the growth rate of AdEx or will we see a negative growth as we saw in 2009?

A lot has happened in the last one week, when we speculated about how Covid-19 might affect the AdEx in 2020. As India fights against all odds to stop the accelerated outbreak of the virus through community transmission with the entire country is facing partial to total lockdown, there is no doubt that our economy will be badly affected like many other developed and developing countries. So, along with the rest of the world, India will be getting into a severe recession for the rest of the year. The point we need to speculate, will there just be a dip in the growth rate of AdEx or will we see a negative growth as we saw in 2009?

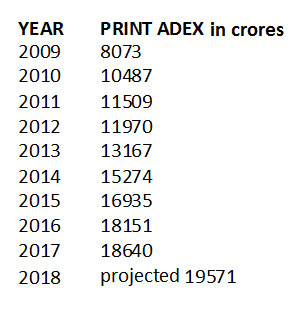

The international financial crisis of 2008 which originated in the sub-prime mortgage crisis in the US and led to a severe recession in many countries over 2008 and 2009 also affected the Indian economy and we saw first a dip in the AdEx in 2008 and then a negative growth in 2009. However, AdEx recovered quickly from that recession and we saw a healthy growth in 2010.

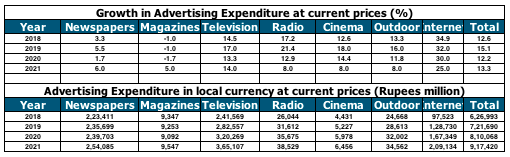

Source: Pitch Madison Media Advertising Outlook 2015

The ripple effect of Coronavirus is going to create an employment crisis across the globe and India will not be an exception. We were already at a high unemployment situation before this crisis hit us. With industries experiencing forced shutdowns, many are asking their employees on go on leave without pay or with truncated pay. Employees who work on the basis of contracts, as per terms and conditions of the contracts are often not paid unless they report to work and in the present situation are likely to lose financially. Financial loss will be experienced by the lower end of self-employed workers (Ola/ Uber drivers, auto drivers, rickshaw pullers, plumbers, electricians, etc.) as well as the daily wage earners. MSME sector which is known as the engine of growth and employment in India will also take a big hit. A combined effect of these muted wage or loss of wage will lead to decrease in consumer demand. In addition, there will be a disruption in the supply chain also due to temporary closure of production, lack of transport for distributing the goods, etc. These changes in demand and supply will have adverse effect on the marketing and advertising budget forcing the advertisers to curtail their expenditure.

Circulation of our print media so far has not been affected like global print media many of who have stopped the printing of hard copies, thanks to the last mile delivery by newspapers delivery persons and hawkers as against the sale through news-stands in developed countries. Indian newspapers managed to develop a schedule of work from home for their reporters and a system of rotation for other essential staff in order to reduce the number of employees present on their premises.

The ‘Janata Curfew’ on March 22 followed by lockdown of some cities/ districts from March 23, may force newspapers also to take a call regarding their production as the distributors/ hawkers and the delivery boys will also get hit by the lack of local transport. Probably, newspapers from second-tier cities under lockdown will be less affected than the newspapers from metros facing a similar situation. So, some Indian newspapers may experience temporary closure and fluctuations in their circulation and readership and subsequently lose ad revenue as supplies of goods dwindle due to logistical issues related to production, transportation, etc. and consumer demand drops.

There is going to be an increase in TV viewership, particularly the viewership of news and entertainment channels as people try to stay abreast with Covid-19 related news and entertain themselves with serials and movies during their stay at home. With all production of Film and TV industry closed till March 31, there is a chance that the serials will run out of their banked episodes which have been already shot and canned. Lack of new episodes will affect the viewership of serials adversely. Even if the viewership of GEC and Movie channels increase, ad revenue may go down due to demand and supply related issues as mentioned above in relation to print.

Sports Channels are going to lose both viewership and advertising revenue with cancellation of sporting events and their telecast. As TV still accounts for the major share of our ADEX, the extent of loss of TV revenue will determine the fate of AdEx in 2020.

Contributions of radio, cinema and outdoor to the overall AxEx are much less than Print and TV. However, ad revenue of FM radio stations will be affected as listening to car radio goes down with people being forced to stay at home. In the US, Nielsen is working on special analysis as well as a quick survey to give the advertisers some idea about how Covid-19 has affected radio listenership. Our Radio Audience Measurement is already affected by lack of financial support from the sector and it may not be possible for them to react in a similar way (http://www.insideradio.com/free/nielsen-to-release-study-on-covid–impact-on-radio/article_6c1e0246-6a81-11ea-8ab4-17d484c1eb56.html).

Many of radio advertising deals are linked with on ground activities and consumer activations and radio ad revenue will see a decline due to curb on all such activities. With closure of malls and cinema halls, cinema will lose the ticket sales money as well as advertising revenue. Traffic on the roads, stations, airports will dwindle due to lock down of cities, social distancing and work from home which will have a negative impact on OOH advertising.

Usage of digital as well as social media will increase during this troubled days as people are trying to get constant update on the pandemic, keep in touch with their friends and relatives while staying at home and opt for some entertainment of their choice on OTT platforms. There is a good chance that advertisers will try to utilise this opportunity by stepping up their budget on digital and social media till the ripple effect of Covid-19 force them to stop advertising.

So far, we have seen only an estimate for loss by events and experiential industry which has been estimated as Rs 3000 crores with ten million jobs at risk which was published on March 17, 2020. (http://everythingexperiential.businessworld.in/article/Loss-to-events-experiential-industry-in-India-estimated-at-Rs-3000-Cr-due-to-COVID-19-ten-million-jobs-at-risk/16-03-2020-186335/). Other media sectors have not yet made any forecast of their probable losses.

The ripple effect of Coronavirus will be directly proportional to the number of days that India takes to control the spread of the virus. In some European countries currently experiencing community transmission, economic analysts are already forecasting that at least 12 to 16 weeks period will be required to curb the virus. If India gets into a similar situation, it may take us longer to curb the virus given the expanse of our country and irresponsible behaviour of our citizens. In that case AdEx will end up with a negative growth like we experienced in 2009.

Trying to estimate the traditional media expenditures during the three months, from August to October, is like the age old story of the blind men with the elephant. Each blind man made a guess based on which part of the elephant he was touching! In this case, please read it as based on the media agency or the advertisers own experience with rate negotiation for Diwali campaigns. The estimates put up by TAM India for Adex is therefore corrected accordingly.

Trying to estimate the traditional media expenditures during the three months, from August to October, is like the age old story of the blind men with the elephant. Each blind man made a guess based on which part of the elephant he was touching! In this case, please read it as based on the media agency or the advertisers own experience with rate negotiation for Diwali campaigns. The estimates put up by TAM India for Adex is therefore corrected accordingly.

By Sam Balsara

By Sam Balsara