By Indrani Sen

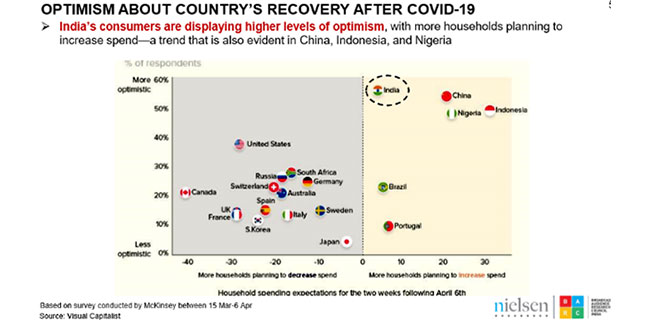

BARC India and Nielsen Media jointly released the fifth edition of the report on ‘Crisis Consumption on TV and Smartphones’ last week. Their presentation before discussing the details of the TV and smartphone consumptions, gave a brief glimpse of a global scenario showing that Indian consumers are more optimistic about their country’s recovery after Covid-19. Similar trait has also been found among consumers in China, Indonesia and Nigeria who have shown higher levels of optimism than Indian consumers.

BARC India and Nielsen Media jointly released the fifth edition of the report on ‘Crisis Consumption on TV and Smartphones’ last week. Their presentation before discussing the details of the TV and smartphone consumptions, gave a brief glimpse of a global scenario showing that Indian consumers are more optimistic about their country’s recovery after Covid-19. Similar trait has also been found among consumers in China, Indonesia and Nigeria who have shown higher levels of optimism than Indian consumers.

Another chart showing a comparison of growth in TV viewing across the globe compared to the pre Covid-19 period and last week (Week 15) highlights the growth in India (40%), Australia (34%), Czech Republic (25%), France (20%) and United Kingdom (17%). The viewership growth in India was driven by both reach and ATS.

After a huge dip in FCT in week 14, there was a rise in FCT during week 15 with many Indian advertisers using the COVID19 theme. Advertisement of essentials category saw a growth across TV genres, but Digital Video Advertising spends dropped across most categories. Reruns driven Hindi GEC in HSM were at an all-time high with 8.5 BN impressions with Mythological shows leading the way. HSM Urban maintained a all time high for 3rd week in row.

TV viewership growth was led by News and Movies and the Movies growth came more from the PAY platforms. Consumption of both News and Movies genre surged after the lock down and now continue to maintain their higher shares. Viewership growth is highest in Mumbai, Bengaluru and Delhi compared to other megacities.

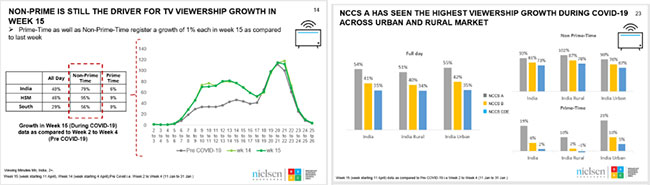

Nonprime time is still driving the overall growth in TV consumption which raises doubts about the long term stability of this growth as after the lockdown is lifted, consumers would not have time for engaging with nonprime time shows. NCH A has seen the highest viewership growth across urban and rural markets with India rural showing high growth of consumption in non-primetime.

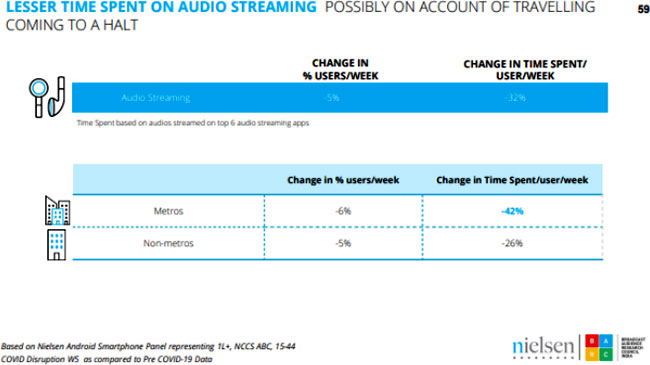

Strong double-digit growth was seen across various segments of OTTs (movies, originals, etc.) while audio streaming apps show a decline possibly on account of commuting going down. During the lockdown period consumers might be opting for audio visual entertainment against just audio entertainment.

The new normal of 3 hrs, 40 minutes+ a day on Smartphone continues – 10% increase over pre-Covid-19 times. News franchise on Smartphone continued to be nearly 50% of all smartphone audience, Views grew by 40%. Almost 4 in 10 searches in week 5 were around Coronavirus which is 4 times the searches made during week 1.

One in five smartphone consumers in India were using the Aarogya Setu app in Week 5 – an 80% + increase v/s the launch week of the app. Consumer time spent on social networking has grown by 35%+ and 1 in 5 spends more than 1 hour per day. With large number of Indians working from home, a staggering 200% increase was seen in time spent on video conferencing and time spent on virtual drives almost doubled.

There is already lot of speculation on the scope of extending WFH and flexible working hour concepts to our work culture as the lockdown is likely to be lifted gradually and definitely not uniformly across the country. It will take quite a few months for our school and college education system to return to normalcy. The growth spurts which we have witnessed in TV and smartphone consumption will not be reduced abruptly. The higher level of smartphone consumption is more likely to continue even after the cloud of Covid-19 starts moving away from India, whereas the higher level of TV consumption is bound to come down and settle at a level above the pre-Covid days.