The path to love is paved with gold. And strewn with flowers.

The path to love is paved with gold. And strewn with flowers.

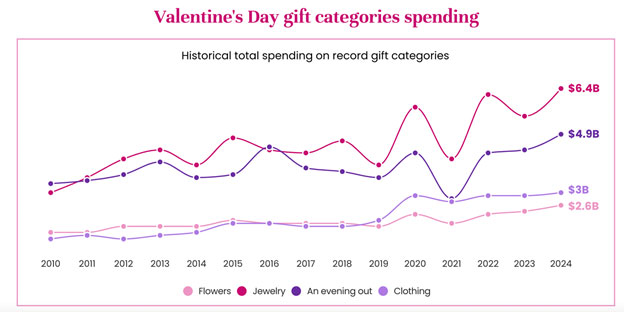

In the United States, consumers plan to spend $25.8 billion on Valentine’s Day this year – an average of $185.81 per person. A 2023 Assocham report estimates the Indian Valentine’s Day market to be worth ₹25,000 crore, while the flower market around Valentine’s Day is estimated at about ₹500 crore.

While couples spending on jewellery, flowers, clothes and romantic dinners drive the lion’s share of that consumption, non-romantic celebrations are a growing trend across the world.

A remarkable evolution of the target audience is apparent in the diverse celebrations associated with Valentine’s Day. Celebrations are now about various kinds of relationships, including friendships, family bonds, self-love, and even expressions of love for pets.

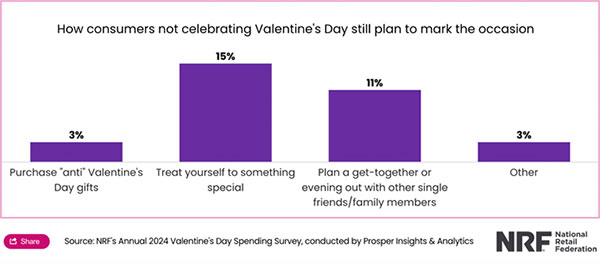

Research amongst ‘non-couples’ reveals that people are spending on themselves – which is only to be expected in this age of self-love, getting together with other unattached friends or family members, or even buying ‘anti-Valentine’ gifts.

These trends are particularly popular among younger consumers.

Over half (53%) of 18- to 34-year-olds and 42% of 25- to 34-year-olds not celebrating Valentine’s Day still find a way to mark the occasion.

Crafting campaigns that embrace this diversity resonates with a broader audience, capturing the essence of love in its myriad forms.

For young women who mark the occasion by treating themselves or throwing a party with single friends, there’s “Galentine’s Day” gift guides from brands like Macy’s, Kay Jewellers and Walmart

1-800-Flowers emphasises the importance of celebrating friendship, recognising that Valentine’s Day is not limited to romantic relationships.

Their ad features a heart-warming scene between two friends, as they reflect on the bond they share and how their friendship has evolved over time. The friends engage in a touching conversation, asking each other meaningful questions about their friendship and the impact it has had on their lives.

DoorDash Self-Love

Knowing that most other delivery services would cater to traditional couples, delivery app DoorDash put forth a narrative that gave single women permission to enjoy Valentine’s Day to the same extent that couples would. This meant capitalising on the existing narratives around pleasure, passion, and romance that are always front and centre on Valentine’s Day – and tailoring them to single women.

Since self-love isn’t new, it was important to have a fresh take. Taking self-love literally, the campaign tapped into the 72% of US adults that believe self-pleasuring is a form of “therapy”, and start a conversation that is weirdly taboo: female self-pleasure. Rooting the conversation in destigmatising female self-pleasure, it used the most iconic Valentine’s gift — a bouquet of red roses. The surprise element: The Self Love Bouquet, a bouquet exclusively on DoorDash made of 11 real roses and one Rose, the bestselling female sex-toy of the last five years. In creating the bouquet, DoorDash was able to deliver $6 million worth of flowers – twice as much as in the previous year to a new demographic – single people who don’t purchase flowers on this holiday, selling the stocks out in four days.

Watch here: https://www.youtube.com/watch?v=f90ORAVPGSc

My Muse

In India, sexual wellness brand, MyMuse challenged love’s most well-known ambassador, Cupid, with its campaign, ‘Modern Love Needs Modern Solutions.’

With Cupid representing age-old societal norms that represent only one right way to love, MyMuse shows how love and people’s expression of it have changed. So, whether it’s choosing your own path, picking your own traditions (old or new), or choosing to settle down or stay single, MyMuse understands that there is no one-size-fits-all in modern love.

Proposing that “Modern Love Needs Modern Solutions – Cupid doesn’t get it, MyMuse does, the brand is running a campaign showcasing a well-meaning Cupid, who attempts to bring couples together in the name of love, using age-old tricks. As his attempts are rejected by people who prefer to find love and express it in their own way with the help of MyMuse products, Cupid has a complete meltdown and starts questioning his life’s purpose.

Watch the series here:

In addition to the films, MyMuse created a Cupid profile and launched a #cancelcupid campaign on LinkedIn, where it leveraged its employees as brand ambassadors.

https://www.linkedin.com/posts/mymuse-india_cancelcupid-activity-7158445512885452801-J-cG/

New forms of celebrating relationships notwithstanding, technology is allowing couples in love to experience Valentine’s Day in fresh ways.

Gaming romance

Zynga, the game publishing label owned by Take-Two Interactive, is commemorating the season of love with a variety of delightful Valentine’s Day 2024 festivities throughout its array of games.

On Farmville, FarmVille 3 – Sweet Nothings, Ginny is brimming with enthusiasm for Valentine’s Day, eager to ensure that everyone on the farm feels cherished and included. She has organized a Valentine’s Phone Booth, where individuals can dial their loved ones and traditionally convey their affection. Participants can even win romantic rewards, contributing to making Valentine’s Day truly unforgettable under Ginny’s thoughtful planning.

On Farmville, FarmVille 3 – Sweet Nothings, Ginny is brimming with enthusiasm for Valentine’s Day, eager to ensure that everyone on the farm feels cherished and included. She has organized a Valentine’s Phone Booth, where individuals can dial their loved ones and traditionally convey their affection. Participants can even win romantic rewards, contributing to making Valentine’s Day truly unforgettable under Ginny’s thoughtful planning.

Monster Legends is commemorating Valentine’s Day with an uproarious new Era Saga featuring Lovestruck, a playful creature known for stirring up mischief during this festive period. However, Lovestruck isn’t the sole attraction in this season’s array; they’re also unveiling Shakespearante, a romantically reimagined rendition of one of their beloved characters.

Monster Legends is commemorating Valentine’s Day with an uproarious new Era Saga featuring Lovestruck, a playful creature known for stirring up mischief during this festive period. However, Lovestruck isn’t the sole attraction in this season’s array; they’re also unveiling Shakespearante, a romantically reimagined rendition of one of their beloved characters.

Dragon City is staging a series of Valentine’s Day-themed events. Players are invited to gather around the campfire to listen to the twisted tale of the new Storyteller Dragon in Part I of the ‘Enemies to Lovers’ Valentine’s event. Participants can aid the new Hanshock and Gretackle dragons in piecing together this ancient narrative by unlocking storybooks filled with rewards and restoring honour to their families in Part II, ‘Sweet Revenge.’

Dragon City is staging a series of Valentine’s Day-themed events. Players are invited to gather around the campfire to listen to the twisted tale of the new Storyteller Dragon in Part I of the ‘Enemies to Lovers’ Valentine’s event. Participants can aid the new Hanshock and Gretackle dragons in piecing together this ancient narrative by unlocking storybooks filled with rewards and restoring honour to their families in Part II, ‘Sweet Revenge.’

Cadbury Dairy Milk Silk – AI Stories

Cadbury Dairy Milk Silk, the chocolate brand from Mondelez India, plays cupid once again to highlight love stories around us. This year, the brand brings an experience that allows couples to transform everyday moments of love into cinematic experiences, powered by generative AI and filmmaker Zoya Akhtar.

Consumers can scan the QR code on Cadbury Dairy Milk Silk packs, leading them to a site where they will need to answer some questions that will help in curating their love stories with personalised avatars, which will be featured in the animated movie. The AI converts simple text input from the consumer into lovable character animations featuring the consumer.

These AI-curated stories will be amplified through strategic media partnerships and personalised content collaborations with leading OTT and music platforms, as well as brand experience zones. Riding on the ultimate goal of making every couple’s Bollywood dream come true, selected videos from the campaign will be featured on the streaming platform Disney+Hotstar, allowing consumers to share their love stories with a wider audience.

Watch the launch video here: https://www.youtube.com/watch?v=8FMhNiKYdOw

Bumble

Bumble, the dating app, is celebrating Lunar New Year and Valentine’s Day in Singapore by launching a new campaign called “Toss Love into the New Year”. The campaign is inspired by the traditional and iconic “Prosperity Toss” or Lo Hei and aims to help Singaporean singles cast out their dating fatigue and manifest a more prosperous love life.

As part of the campaign, Bumble is giving away a curated exclusive ‘Lo Hei’ pack filled with eight goodies, such as fish ball crackers, Hershey’s kisses chocolates, and salted egg fish skin from Golden Duck. Each goodie represents Bumble’s eight mantras to manifest a prosperous love life, such as “Everything starts with a belief”, “I take control, love will unroll”, “Healing on the inside, beaming on the outside” and “I’m always real, authenticity is the deal”.

The first 200 users of the app can get the pack on a first-come-first-serve basis. Bumble’s partners in the campaign are Singaporean influencer and content creator Saffron Sharpe and Feng Shui expert and TikTok creator Cliff Tan. Sharpe is featured in a video explaining the meaning of the eight mantras and setting up Bumble’s ‘Lo Hei’ pack. She also provides tips on rearranging one’s personal space to invite love back into their lives.

Watch here: https://www.youtube.com/watch?v=OniSUjjTiV8

Something to be inspired by when planning your next Valentine’s Day activation?

Kunal Sinha is a senior strategy and foresights executive based in Jakarta, Indonesia. He is the author of several books including The Future of India’s Rural Markets and Raw – Pervasive Creativity in Asia. He writes for MxMIndia every other Monday. His views here are personal.

[1] NRF and Prosper Insights & Analytics, 2024

[1] https://startuptalky.com/valentines-day-india-economy/

At the dawn of the internet era and, a bit later, of the social media era, many sociologists believed they would lead to a more informed and enlightened world. The events at Tahrir Square, the subsequent Arab Spring, and later the Maidan revolt in Kyiv seemed, for a period, to support this contention. Marketing gurus posited the dawning of the age of interactive and one-to-one marketing, much like the bazaar of yore but on a global, post-modern scale.

At the dawn of the internet era and, a bit later, of the social media era, many sociologists believed they would lead to a more informed and enlightened world. The events at Tahrir Square, the subsequent Arab Spring, and later the Maidan revolt in Kyiv seemed, for a period, to support this contention. Marketing gurus posited the dawning of the age of interactive and one-to-one marketing, much like the bazaar of yore but on a global, post-modern scale.

It’s that time of the year, when the General Elections are round the corner. While the dates are not out yet, we may be less than 75 days away from the first round of polling. Even if the outcome seems somewhat like a foregone conclusion, the next three-four months will be full of political and media frenzy.

It’s that time of the year, when the General Elections are round the corner. While the dates are not out yet, we may be less than 75 days away from the first round of polling. Even if the outcome seems somewhat like a foregone conclusion, the next three-four months will be full of political and media frenzy.

With apologies to none at all

With apologies to none at all