Why MxM Open Classroom: Upskill yourself!, That’s what one is told so as to make the extended lockdown work for us. But while doing one of the hundreds of free or paid courses sounds easy, in realit, it isn’t. And going through the tests and quizzes that are contained in them can be quite daunting. Starting this week, we start a series of ‘open classroom’ sessions. Each week, we will have a five-part series – Monday through Friday that will tackle an important area of the media marketing services domain. We kick off our series with a focus on Digital Marketing with Bhuvi Gupta, a marketing specialist who has

The HOWs and WHYs of making trends

By Bhuvi Gupta

By Bhuvi Gupta

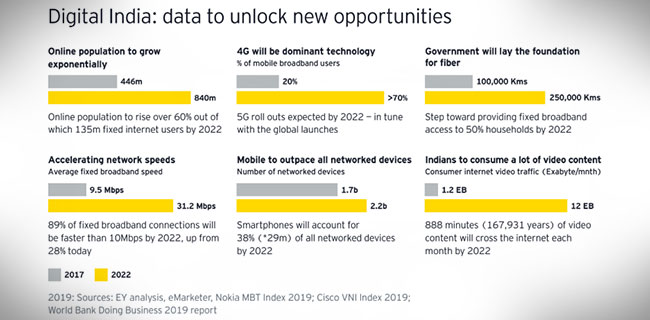

According to a FICCI EY report, the Indian Media and Entertainment (M&E) sector grew 9% to reach INR 1.8 trillion in 2019.

The rapid spread of mobile access is helping the growth of the digital media industry. With a population of 1.3 billion, 688 million internet subscribers and nearly 400 million smartphone users, quantitatively, India already has high numbers but also has high potential for growth. This means that the digital media industry which grew 31% to reach INR 221 billion in 2019 will continue growing and industry experts expect it to grow at 23% CAGR to reach INR 414 billion by 2022. Digital advertising grew 24% to INR 192 billion and is expected to follow a similar growth trajectory. As digital penetration increases, more advertising budgets will get diverted to digital, especially because digital advertising is easier to measure and to finely tailor target audiences.

The biggest challenge with digital is the evolving landscape – changing algorithms of popular platforms, newer applications of Augmented Reality, new platforms with niche demographics (like Helo, ShareChat, Likee, Bigo), and newer forms of advertising like influencer marketing to only name a few. This makes it difficult to allocate digital budgets effectively because the ‘how’ of being effective is constantly in flux.

This series is in a sense a cheat sheet to understand digital advertising better and to ease navigating this evolving landscape. In each article, we will evaluate how to best create virality by leveraging popular digital platforms. Key focus platforms will be Instagram, TikTok and Facebook, chosen because of the reach, they garner.

To kickoff the series we focus on the objective of many if not most campaigns – ‘Virality’. Making a campaign ‘viral’ is the holy grail by which campaigns are measured & many awards given, today.

Marketers know that in spite of how topical and relevant the communication it is impossible to guarantee campaign virality because there are too many variables. However, what is attainable is ensuring that a campaign ‘trends’.

The key difference between a campaign ‘trending’ and it ‘going viral’ are in longevity and organic reach. While a trend may last for a short period of time, may be paid for and limited to a particular target audience, a campaign going viral implies that it has had the longevity of a few days, substantial word of mouth and a high recall value that has surpassed its initial targeting. Hence, while all viral campaigns, trend, not all trending campaigns go viral. With the right strategy it is possible to make a quality campaign trend, which may be the push it needs to achieve virality.

A quality campaign is one, which while espousing product benefits, is topical and evokes a strong emotional response so that it is prompts the viewer to share it to enable word of mouth. An easy test to determine shareability is to ensure that the messaging is entertaining, inspiring or informative or a combination of the three.

Here are Five ways to make a quality campaign ‘trend’–

I. Choosing 1 or 2 focus platforms

Today every social media platform has a key age and socio-economic demographic. Depending on the messaging, the brand, and campaign budgets focus platforms should be defined. It is wise not to focus on more than two, even if budgets permit. Successful campaigns will spillover organically to other platforms, anyhow. For e.g. in 2019, Pepsi used TikTok as their primary platform for promoting their new brand anthem with the tagline ‘Har Ghoont mein Swag’. The campaign anthem was sung by 2019’s most popular Bollywood Punjabi singer, ‘Baadshah’ and the music video starred popular Bollywood youth icons & social media influencers, Tiger Shroff & Disha Patani. TikTok was was aligned to the brand’s mass & youth focused targeting. The campaign was a huge success, with 240+ million views and over 15,000 user-generated videos within 24 hours of its launch. The campaign also naturally spilled over to Instagram, where it received 20+ million views. The campaign remains one of TikTok’s most successful brand campaigns in India.

II. Challenges

A campaign which requires the consumer to engage will automatically have higher recall value & will also allow for the network effect which will help it to trend organically. The messaging of the campaign is key to how it can have a challenge component.

Challenges are especially relevant for TikTok, and Instagram. Hashtag challenges form a key component of TikTok and challenges typically trend for a week. Hence, hosting challenges aligned to brand campaigns on TikTok can help a campaign achieve virality. Currently, a Challenge trending on both TikTok & Instagram is the #PassTheBrushChallenge, where different women, pass a makeup brush to each other while showing before & after images of themselves wearing makeup. The challenge has not been initiated by any brand, but has gone viral with different kinds of iterations being produced, including a male version with a hairbrush!

III. Hashtags –

A hashtag, which can be the campaign tagline in entirety or a part of it is a key component of a trending campaign, as it is an easy identifier when the post gets shared, or mentioned. A hash tag is easy to understand, catchy, and related to the brand. It should ideally be not more than 3-4 words, have a verb, and either the brand name or a keyword from the catch phrase.

Hashtags are vital for discovery on Twitter& TikTok, while they serve as identifiers on Instagram, Facebook & YouTube. Along with the key campaign hashtag, it is advisable to use other aligned & popular hashtags with which the content can be discovered.

For e.g. in the Pepsi ‘Har Ghoont mein Swag’ campaign the key hashtag used was the same as the tagline, #HarGhoontMeinSwag along with #SwagStepChallenge. The campaign was followed up by a follow up campaign, with a new single called ‘Swag Se Solo’ sung by 2019’s breakout Bollywood singer, Tanishk Bagchi, released in February 2020. This campaign used the hashtag #SwagSeSolo and re-used the hashtag #SwagStepChallenge.

IV. Influencer Marketing –

Today, to break the clutter, it is crucial to invest a part of advertising budget on influencer marketing. Influencers enjoy loyal fanbases, and due to their relatibility, are often more trustworthy and credible than celebrities. Targeting influencers aligned to target audiences can help get exponential reach and engagement.

However, influencers per platform need to be defined because each platform has different influencers in the same niche. A beauty influencer on TikTok may not enjoy the same following on Instagram & YouTube, and hence can not be used for a campaign with Instagram as the primary social media platform.

Influencer marketing works on all platforms, but is especially relevant on TikTok, Instagram and YouTube. It is especially effective for marketing new launches. Popular mobile phone brands often leverage influencer marketing while marketing their new launches – One Plus, gets influencers across industries to post videos highlighting the USP of the new launch. Google hosts parties with photo booths and gourmet food and, gifts influencers the latest ‘Pixel’ device. Photos of the party get shared on social media by all the attending influencers, thereby successfully creating a buzz. One of the most successful examples of influencer marketing remains the selfie taken by Ellen DeGeneres at the2014 Oscar ceremony (sponsored by Samsung) where Hollywood’s A listers posed for a selfie taken with a Samsung Galaxy Note 3. What remains ‘Note’-worthy is that the picture, which was shared, was not of the selfie but that of the stars taking the selfie so that the ‘Samsung’ logo was prominently displayed.

V. Digital Advertising –

For platforms such as Facebook, and now Instagram, which have attained maturity in their life cycle, the competition for organic reach is high. Hence, using advertising for discovery and amplification is necessary for virality. To enable speedier discovery it is advisable to use advertising on TikTok as well. Digital advertising used in conjunction with the above strategies, on the chosen platform (s) can effectively amplify the campaign. While it will definitely help a campaign to trend, it can often serve as a tipping point for creating virality.

The gulf between a trend and virality is deep and often, a trending campaign that reaches relevant audiences is sufficient to earn ROI and achieve the brands marketing objectives. Virality is very often a vanity metric, which helps the brand create widespread awareness like traditional ATL marketing but may not aid in creating actual consumer intent.

Bhuvi Gupta is a marketeer with over a decade of work experience, of which the last six have been in the media & entertainment industry. She has been a part of many launch marketing campaigns with experiences at the Times of India group, Republic TV and the latest in marketing a Bollywood film

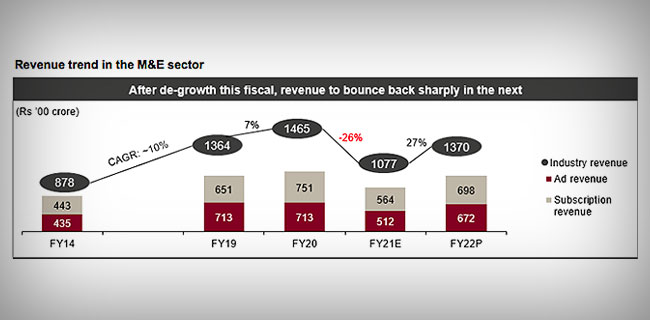

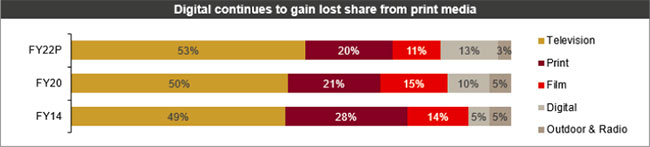

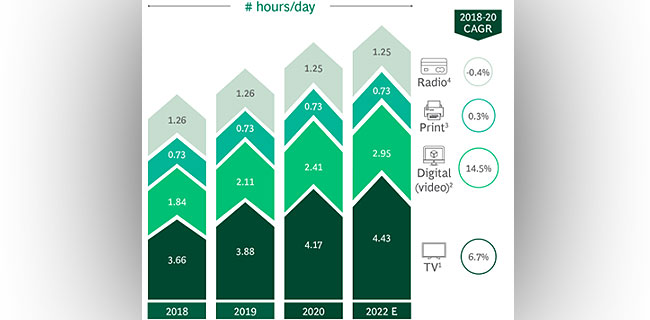

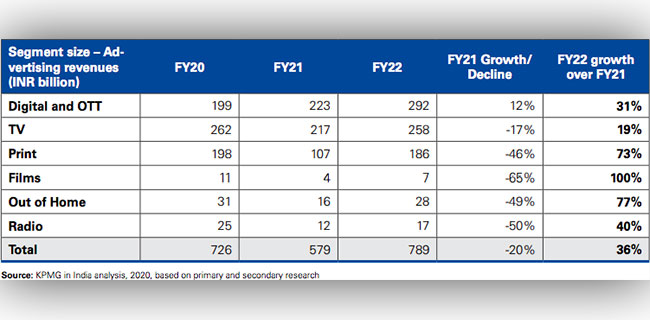

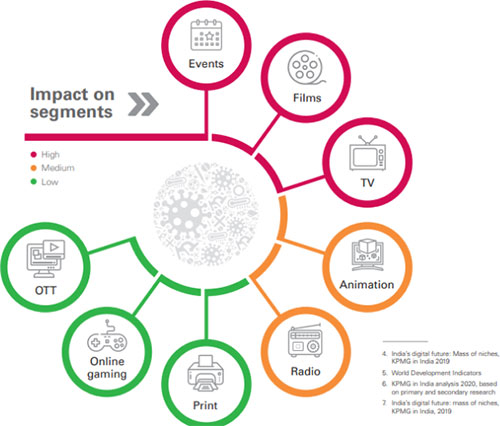

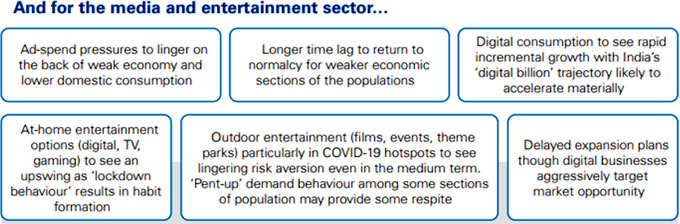

Last week, KPMG released a report titled “Covid-19: The Many Shades of a Crisis” trying to provide stakeholders in media and entertainment a perspective of the effects of Covid-19 on M&E sector (https://home.kpmg/content/dam/kpmg/in/pdf/2020/04/the-many-shades-of-a-crisis-covid-19.pdf).

Last week, KPMG released a report titled “Covid-19: The Many Shades of a Crisis” trying to provide stakeholders in media and entertainment a perspective of the effects of Covid-19 on M&E sector (https://home.kpmg/content/dam/kpmg/in/pdf/2020/04/the-many-shades-of-a-crisis-covid-19.pdf).

By Shailesh Kapoor

By Shailesh Kapoor

On the second working day of this rather short post-Diwali week, here’s a question uppermost in our minds. If you wish to access the archives, please go to the Das Ka Dum tab on the website’s top navigation bar.

On the second working day of this rather short post-Diwali week, here’s a question uppermost in our minds. If you wish to access the archives, please go to the Das Ka Dum tab on the website’s top navigation bar.