This is the fourth in a series of six decade-ender lists in this column. The previous lists:

The most-defining Hindi TV shows of the decade

The most-defining Hindi films of the decade

The most successful OTT brands of the decade

By Shailesh Kapoor

The decade of 2010-19 was easily the most uneventful decade in the history of Indian television so far. Each of the previous three decades was dotted with events that unmistakably shaped television in India. The 80s was the golden age of television content, as Doordarshan started to provide primetime programming and engaged with some of the best writing, directing and acting talent in the country for the same. The 90s saw the emergence of satellite television, which widened the options available to the audience multi-fold. The 2000s saw the daily soap movement, led by Star Plus, and then, the rise of the alternative force in Colors, which brought a unique, real and rustic touch to mass entertainment. Each of these decades had a big highlight at the start. The Asian Games in the 80s saw the arrival of the colour TV. The Gulf War telecast in the 90s, albeit niche, introduced us to the fascinating power of satellite television. And Kaun Banega Crorepati ushered in a new era in 2000.

The decade of 2010-19 was easily the most uneventful decade in the history of Indian television so far. Each of the previous three decades was dotted with events that unmistakably shaped television in India. The 80s was the golden age of television content, as Doordarshan started to provide primetime programming and engaged with some of the best writing, directing and acting talent in the country for the same. The 90s saw the emergence of satellite television, which widened the options available to the audience multi-fold. The 2000s saw the daily soap movement, led by Star Plus, and then, the rise of the alternative force in Colors, which brought a unique, real and rustic touch to mass entertainment. Each of these decades had a big highlight at the start. The Asian Games in the 80s saw the arrival of the colour TV. The Gulf War telecast in the 90s, albeit niche, introduced us to the fascinating power of satellite television. And Kaun Banega Crorepati ushered in a new era in 2000.

In contrast, the last decade (2010-19) can only be remembered for what happened ‘off-screen’. The ratings controversies, leading to the birth of BARC India, in the midst of digitisation, headlined the first half of the decade. And TRAI’s New Tariff Order was the big talking point as the decade ended.

Low content innovation and a general sense of inertia became even more apparent as digital and social media grew on the side, becoming a dominant force by the time the decade ended. Yet, some TV channels stood out, challenging the status quo and making a mark for themselves. Here’s my list of the top 5 most successful TV channels in India over the last 10 years, based on how they navigated through this tricky decade, making a mark for themselves, and their parent networks.

5. Sony SAB

SAB’s flagship show Taarak Mehta Ka Ooltah Chashmah (TMKOC) launched in 2008, and kept going strong through this decade. For large chunks of time over the last 10 years, SAB struggled to have a second hit show. But there were strong periods in between, when the channel managed to add fire power to TMKOC to emerge as a strong contender in the Hindi GEC category. 2019 was one such year, and the channel has been on the heels of Star Plus, Colors and Sony for the top spot, and often taken it too. SAB’s success is even more remarkable if you consider than it operates at significantly lower programming costs compared to other top Hindi GECs. TMKOC itself has gone from strength to strength, and SAB’s packaging and family-inclusive positioning are arguably the brightest and the sharpest respectively, in the genre.

4. Nick

In a category that’s essentially commoditised, and one flagship show is all you need to dominate the ratings charts, Nick managed to rule the roost for a large share of the decade, and often by a wide margin too. While its competition found it difficult to extend their portfolio beyond one show (e.g. Chhota Bheem on Pogo and Doraemon on Disney), Nick kept the animation mill running, launching several properties through the decade, with varying levels of success. While its 2012 launch Motu Patlu remains its biggest success story till date, the channel managed to sustain a strong second line, and showed nimble-footedness in experimenting with content shifts between the two sister channels Nick and Sonic.

3. Star Plus

The decade started with Colors emerging as a disruptive force in the Hindi GEC category, throwing Star Plus and Zee TV off their comfort zone with a new programming outlook. After a year or two of trying to figure out what had hit them, Star Plus found its feet back. Its ‘Rishta Wohi Soch Nayi’ campaign in 2010-11 is easily the most effective brand campaign any mass Hindi TV channel in India has ever launched. Unlike the umpteen ‘brand refreshes’ that GECs indulge in, this one was actually backed by content, ushering in a new line of shows like Diya Aur Baati Hum and Pratigya, which put strong women protagonists on the forefront, in relatable, small-town settings. In the second half of the decade, the Hindi GEC category went through a tough phase, losing ratings to regional, news and movie genres. Star Plus innovated here too, launching the ‘Rishta Wohi Baat Nayi’ campaign, signaling its focus on differentiated content that breaks the monotony of sameness. On the side, experiments like Satyamev Jayate continued, even as the channel managed to steer through many highs and lows over 10 long years.

2. Zee Tamil

For the first half of this decade, the Tamil GEC category was a one-horse race. Sun TV led its closest competitor Star Vijay by an embarrassingly-wide margin. The ratio of their viewership was often higher than 10:1. Zee Tamil was in a wooden spoon battle for the second spot with Star Vijay, with no hopes of catching up with the big force at the top. But somewhere in mid-2006, the channel started finding an alternative content space. It took a couple of years, but Zee Tamil became a strong contender, overtaking Sun TV in some prime-time slots, and bringing down the 10:1 ratio to 2:1, even less at times. Importantly, it altered the viewing behaviour of the category, as it made the audience realise there are options beyond Sun TV to consider. Even Star Vijay has gained because of this behaviour change. While Sun TV still ranks no. 1, it has lost about 20-25% of its viewership through the decade, even as Zee Tamil has grown by a whopping 500%+.

1. Star Sports

There’s so much to say about Star Sports’ dominance of the sports scene over the last 10 years that it may need a separate article some time. One can talk about the thought leadership shown in backing Kabaddi (and later soccer), or the front-footed approach towards IPL rights, or the digital strategy for sports with Hotstar, or the championing of Hindi commentary in the early part of the decade to the launch of regional channels in the latter. The long list of Star Sports’ innovations in the sports category provides a silver lining to a dull television decade. Star Sports’ much-underplayed tagline says ‘Believe’. It’s probably more a reflection of how Star looks at the future of sports and sports programming in India, than what they want Star Sports viewers to feel about the channel!

Shailesh Kapoor is founder and CEO, Ormax Media. He writes on MxMIndia every Friday. His views here are personal

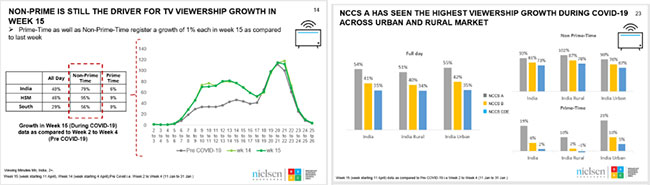

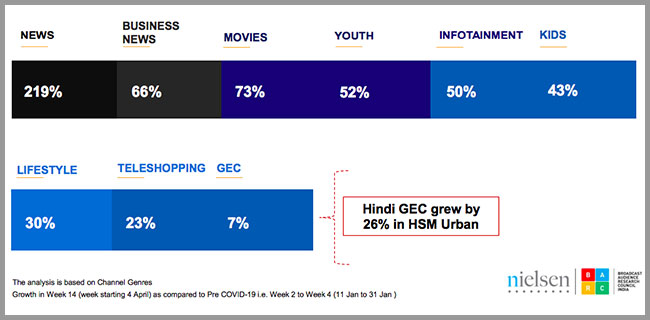

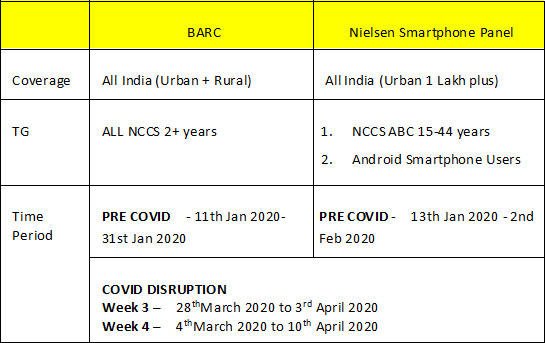

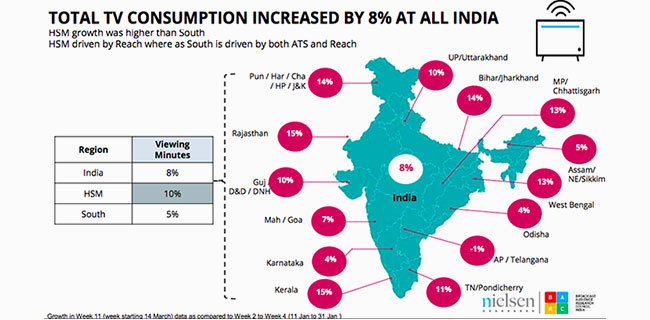

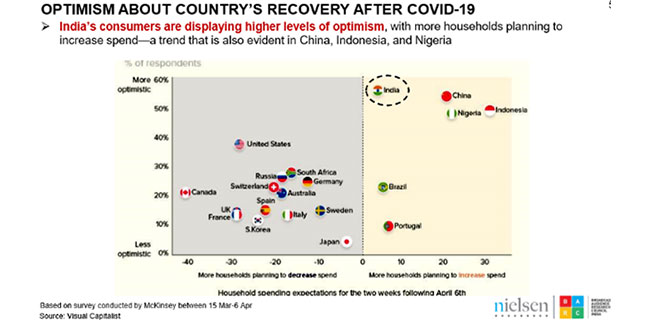

BARC India and Nielsen Media jointly released the fifth edition of the report on ‘Crisis Consumption on TV and Smartphones’ last week. Their presentation before discussing the details of the TV and smartphone consumptions, gave a brief glimpse of a global scenario showing that Indian consumers are more optimistic about their country’s recovery after Covid-19. Similar trait has also been found among consumers in China, Indonesia and Nigeria who have shown higher levels of optimism than Indian consumers.

BARC India and Nielsen Media jointly released the fifth edition of the report on ‘Crisis Consumption on TV and Smartphones’ last week. Their presentation before discussing the details of the TV and smartphone consumptions, gave a brief glimpse of a global scenario showing that Indian consumers are more optimistic about their country’s recovery after Covid-19. Similar trait has also been found among consumers in China, Indonesia and Nigeria who have shown higher levels of optimism than Indian consumers.