By Our Staff

Pause for a moment. Look to the left or right of the screen. Or text in a different colour. This is no marketing initial or promotional exercise done at the behest of one of the competing platforms. It’s the main finding of an Axis My India survey of 10,034 people surveyed, 66% of who are from Rural India while 34% are from Urban India. This is part of the India Consumer Sentiment Index (CSI), a monthly analysis of consumer perception on a wide range of issues. The April report highlights that 19% of families have reported a rise in media consumption. Moreover, the survey reveals that urban areas and male viewers are leading the surge in media viewership. The enthusiasm for IPL is expected to increase further, with both TV & mobile contributing to viewership. The study also delved into the key factors that influence consumers’ buying decisions, revealing that product quality and brand name remain important considerations. Additionally, the survey sheds light on the role of celebrity endorsements in driving product purchases, with younger age groups being more susceptible to their influence.

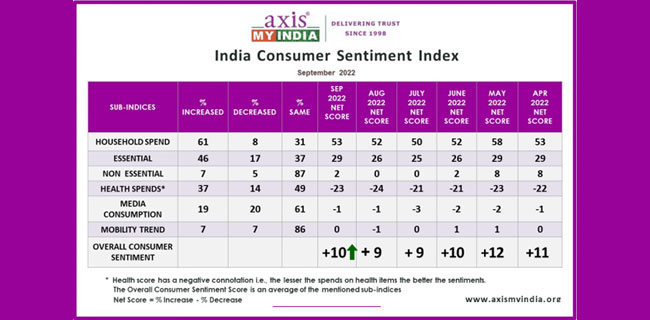

The April net CSI score, calculated by percentage increase minus percentage decrease in sentiment, is at +8, which is the same as last month. The corresponding net score last year was +11.

The sentiment analysis delves into five relevant sub-indices – Overall household spending, spending on essential and non-essential items, spending on healthcare, media consumption habits, entertainment & tourism trends.

The survey was carried out via Computer-Aided Telephonic Interviews with a sample size of 10,034 people across 33 states and UTs. 66% belonged to rural India, while 34% belonged to urban counterparts. In terms of regional spread, 25% belong to the Northern parts while 26% belong to the Eastern parts of India. Moreover, 28% and 21% belonged to Western and Southern parts of India respectively. 63% of the respondents were male, while 37% were female. In terms of the two majority sample groups, 29% reflect the age group 36YO to 50YO and 29% reflect the age group of 26YO to 35YO.

Commenting on the CSI report, Pradeep Gupta, Chairman & MD, Axis My India, said: “Closely examining the findings of our latest survey, it is clear that media consumption habits are not uniform across demographics, with variations emerging among different age and gender groups. It is noteworthy that younger age groups are showing a greater appetite for media consumption, with a particular interest in watching the Indian Premier League. Digital is expected to contribute significantly to the rise of IPL viewership. As we delve deeper into consumer behaviour, it is evident that product quality and brand name remain key considerations, but we are also seeing a significant impact of celebrity endorsements on purchasing decisions, especially among younger age groups. These insights highlight the need for brands to stay attuned to the evolving consumer preferences and tailor their marketing strategies accordingly to drive engagement and enhance customer loyalty.”

On topics of current national interest

• :: • This month Axis My India’s CSI survey further deep dived to understand citizens’ sentiments towards the 16th edition of Indian Premier League. As per the survey 42% would watch IPL this season, out of this 19% would watch all the matches whereas 22% would only watch matches where their ‘favourite’ teams will play or critical matches like eliminators and finals. About 26% of youngsters (18-25YO) wants to watch all the matches as compared to older age group highlighting their younger spirit and interest in IPL. In addition, male viewers and urban areas show more interest in watching the tournament.

• :: • Further investigating sentiments, the study discovered that 57% would watch the matches only on cable/DTH Television sets while 30% will watch it only on mobile – Jio Cinema. 8% said they would watch on both TV and mobile. 3% plans to watch the tournament physically from the stadium. About 32% from rural areas show more interest in watching IPL on mobile given the free telecast of IPL matches. Middle age groups, of 26-50 YO would prefer watching more on television than younger age groups.

• :: • In an attempt to understand product purchase behaviour, the survey found out that 52% considers product quality and 33% considers brand name as important factors. 60% of 18-25YO puts weightage on the product quality whereas 35% of 36-50YO considers brand name as important factors. Price is overall considered as the third most important factor with a vote of only 22%.

• :: • The survey also unveiled that advertisement in which celebrities feature, influence product buying decisions of 30% to some extent. Of this, about 35% of them are youngsters (of age 18-25) and 27% are middle-old and older age group.

• :: • With summers approaching, the survey highlighted that overall 15% plans to buy durables like AC or Refrigerators in the next 2-3 months. Moreover 19% of youngsters (18-25 YO), highest amongst all age groups are considering to buy durables like AC, fridge etc. this summer season.

• :: • The survey also threw light on consumer travel plans this summer season. Overall 24% plans to travel of which 23% said they are planning for a domestic holiday while 1% is planning for an international vacation. Plans of travel is higher in the younger age group of 18-25 years at 30%.

• :: • On employment opportunities the survey revealed that 50% believe that there are more openings/opportunities as compared to last 10 years. 53% of the female population have a positive outlook regarding the same highlighting the raise in the number of jobs available for the gender. In addition, younger age group (18-25YO) also thinks job opportunities have increased overtime.

• :: • Moreover, the survey discovered that among the top professions in the country 25% would prefer their children to enrol in the Govt service, 16% would prefer them to be in medical profession while 10% would prefer them to work in fields related to Engineering, Computer application, IT. A majority of 35% are of the view that their children should do whatever they want to do.

Key findings

• :: • Overall household spending has increased for 56% of the families, this reflects a decrease of 2% from last month and 6% from April’22. The net score, which was +51 last month and +53 in April’22 has reduced to +49 this month. The two states, which reflected the highest increase, are Telangana with 70%, followed by Andhra Pradesh with 66%. The age group between 26-50 showcased the highest increase (58%).

• :: • Spends on essentials like personal care & household items has increased for 33% of the families, which reflects a dip by 3% from last month and 15% from April’22. The net score, which was at +23 last month and +29 in April’22, has decreased to +21 this month. Essential spends has increased more for rural segment (33%) as compared to the urban counterparts (31%). Karnataka and Tamil Nadu reflects the highest essential spends with 50% and 49% respectively. The age group between 36-50 showcased the highest increase (36%).

• :: • Spends on non-essential & discretionary products like AC, Car, and Refrigerator have increased for 4% of families, which is the same as last month and reflects a dip by 9% from April’22. The net score, which was at 0 last month, remains the same.

• :: • Expenses towards health-related items such as vitamins, tests, healthy food has surged for 32% of the families. This reflects a decrease in consumption by 3% from last month and 6% from April’22. The health score which has a negative connotation i.e., the lesser the spends on health items the better the sentiments, has a net score value -22 this month. Health related products consumption increased more in rural areas (33%) and among age group of 26-35 (about 34%). Karnataka with 49% and Bihar with 43% reflect the highest spends in health-related products.

• :: • Consumption of media (TV, Internet, Radio etc.) has increased for 19% of the families, which is the same as last month and reflects a dip by 3% from April’22. The overall, net score is at 0 this month. Media viewership has increased more in urban areas (21%) and among males (20%) while it is only 17% among females. In addition, media consumption is more among 18-25 YO which (29%) as compared to older age groups.

• :: • Mobility has increased for 6% of the families, which reflects a decrease by 1% from last month and same as April’22. The overall mobility net indicator score, which was at 0 last month, is at -1 this month. 10% of the youngsters from the age group of 18-25, has gone out more in the last month as compared to other age groups.