By A Correspondent

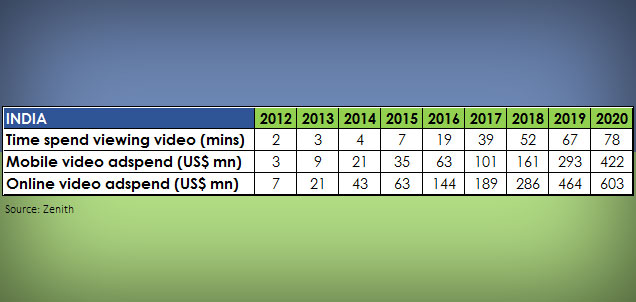

Online video viewing will leapfrog to 52mins a day in 2018 from a lowly 39 minutes in 2017, report media agency network Zenith.Global consumers will spend an average of 67 minutes a day watching online video this year, up from 56 minutes last year, according to Zenith’s Online Video Forecasts 2018, published today. By 2020 the average person will be spending 84 minutes a day watching videos online. In that year, China will have the keenest viewers, with the average person spending 105 minutes a day watching online video, followed by Russia (102 minutes) and the UK (101 minutes). This rapid rise in consumption is leading to a shift in the way brands plan campaigns across both television and online video. India-specific numbers are in the table above.

This is the fourth edition of Zenith’s annual Online Video Forecasts report. It contains historical data and forecasts of online video consumption and advertising, together with commentaries on the development of individual markets by local experts. This year’s edition covers 59 key markets. By online video we mean all video content viewed over an internet connection, including broadcaster-owned platforms such as Hulu, ‘over-the-top’ subscription services like Netflix, video-sharing sites, e.g. YouTube, and videos viewed on social media.

Global online video consumption grew by 11 minutes a day in 2017, and we expect it to grow by an average of 9 minutes a day each year to 2020. It accounts for almost all the growth in total internet use, and is growing faster than media consumption overall, so it is taking consumption time from traditional media. Although some of this extra viewing is going to non-commercial platforms such as Amazon Prime and Netflix, plenty of it is going to commercial platforms, so the supply of commercial audiences is rising rapidly.

Zenith estimates that online video adspend grew 20% in 2017, to reach US$27bn. Growth peaked at 36% in 2014 and has fallen steadily since then, but still remains very high. “We forecast 19% growth in 2018, and an average of 17% annual growth to 2020, when online video adspend will reach US$43bn. Video’s share of online display advertising is rising steadily: it accounted for 27% of display adspend in 2017, and we expect it to account for 30% in 2020,†the report notes.

More from the report:

The supply of online video audiences has been growing ahead of demand in recent years: online video viewing grew 91% between 2015 and 2017, while adspend grew 52%. The cost of online video advertising has therefore come down substantially. As the growth of video consumption grows we expect prices to stabilise, with mild increases from 2019 onwards.

Online video advertising is still only a fraction of the size of television advertising, but because television is stuck at 0% to 2% annual growth, this fraction is rising rapidly. The online video ad market was 10% of the size of the television ad market in 2015, and 14% in 2017. By 2020 we expect online video adspend to be 23% of the size of television adspend.

Online video and television complement each other well, with most brands initially using online video to add incremental reach to their existing television campaigns. But with the rapid growth of online viewing we are now seeing more brands plan television and online video together to optimise frequency.By cutting out television spots that lead to very frequent exposure among heavy television viewers, andusing online video to target – and retarget – light television viewers, brands are using television and online video together to cut out both overexposure and underexposure within the target audience, maximising recall at a reduced price.

Online video advertising began by emulating television advertising, with most ads appearing within other video content that the viewers were really interested in as interruptive ‘in-stream’ ads. But over the past few years ‘out-stream’ ads have become common. These are stand-alone video ads that appear within text or images, or within a social news feed. Thanks mainly to the rapid adoption of video content and advertising by social media platforms, out-stream video is rapidly becoming the dominant form of online video advertising. In the UK, for example, it overtook in-stream advertising to account for 56% of online video adspend in 2017. This is changing the structure of online video creative. Because a viewer can simply scroll past them, out-stream ads need to grab the viewer’s attention from the very first second, either with an arresting image or with a celebrity with a dedicated following. They do not have the narrative leeway available to interruptive ads.

“Online video is driving growth in global media consumption, as smartphones with high-speed data connections make high-quality video available to people on the move, and smart TV sets give viewers unparalleled choice in the living room,†said Jonathan Barnard, Zenith’s Head of Forecasting and Director of Global Intelligence. “The rapid rise in video viewing makes online video the world fastest-growing advertising format, creating new strategic and creative opportunities. Brands that do not currently have a strategy for online video need to think about getting one.â€

Among the more significant findings, print media continues to be the largest sector in advertising, and is expected to grab a 40% share this year. Brand advertising in print is likely to exceed Rs 16,000 crore. TV is next in line, and expected to touch Rs 15,500 crore. Digital, which has grown phenomenally in the last five years, is now larger than Outdoor, Cinema and Radio put together, will corner 12.6% of the market.

Among the more significant findings, print media continues to be the largest sector in advertising, and is expected to grab a 40% share this year. Brand advertising in print is likely to exceed Rs 16,000 crore. TV is next in line, and expected to touch Rs 15,500 crore. Digital, which has grown phenomenally in the last five years, is now larger than Outdoor, Cinema and Radio put together, will corner 12.6% of the market.