By Indrani Sen

By Indrani Sen

While a violent dust storm was sweeping across parts of North India last week, causing destruction, death and havoc in many ways, we saw a digital news storm in terms of the number of reports and announcements breaking on the internet related to the M&E Industry in India focussing on digital. Fortunately for us, the nature of this digital storm has been more constructive and futuristic reflecting the changes expected in India in the short-term and the long-term.

It began on a quite note on May 1, when we read a well-researched article “Is smartphone the new TV†by Gaurav Laghate of Economic Times. It is a must-read for all who are interested in future of digital India). Facebook was holding its annual Facebook Developers Conference, F8 in San Jose, CA on May 1 and 2 and naturally I expected that we will get to see an analysis of the proceedings and new announcements also on Indian websites.

On May 2, www.socialsamosa.com carried the highlights of the first day of the F8 conference, but chose to highlight in a special story the video chat feature getting added to Instagram. Brand Equity also carried a report by Reuters highlighting how Facebook will use AR to draw ads on Messenger App.

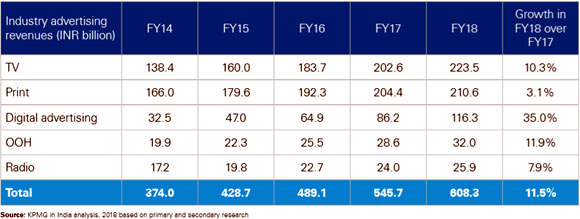

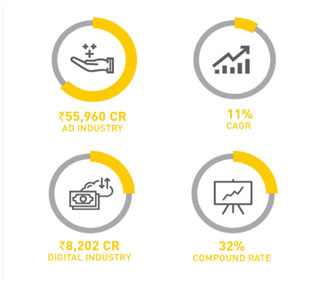

The next day – on May 3 – we were literally floored by news related directly or indirectly to the digital industry. The biggest news of the day was Sameer Singh joining GroupM as CEO, South Asia. An IIM Calcutta alumnus, Singh has fascinating experience of 28 years in marketing and media withleading advertisers and agencies across different markets. His move from Google toGroupM reflects GroupM’s plan for moving towards the digital future. The second important news was that digital advertising in India will touch Rs 12,046 crore by December 2018 growing at CAGR of 30% based on the “Digital Advertising in India 2017†report jointly published by the Internet and Mobile Association of India and Kantar IMRB.

In addition to the above two news, on May 3 we read in Brand Equity about Tim Cook wanting India a larger size of the Apple and stepping up marketing and retail initiatives and declaration of bankruptcy and closure by Cambridge Analytica, the firmlinked with the recent privacy scandal of Facebook. Viacom 18 Motion Pictures announced the new launch of its digital content brand “Tipping Pointâ€which will offer a host of web series, short films and non-traditional formats in collaboration with some leading film directors. Another interesting report was published in www.emarketer.com. Based on a global study by e-marketer,the report predicted that by end of 2018, more than a quarter of Indian individuals of any age will be smartphone users.

The next day, on May 4,GroupM released its publication “The State of Digital†predicting inflation in inventory cost on mobile formats in India where 42 per cent of online ad spend will be on video ads and 12 of all digital advertising will be programmatic. Their Global predictions include continuation of stronghold of the duopoly by Google and Facebook and online time spent overtaking linear TV viewing timein 2018. On the same day we also read the announcementby WPP that the Analytics teams from Kantar and Group M will be combined to form one combined practicein India. These two stories/ media releases were carried in many industry websites.

On May 5 we read in Brand Equity that Facebook is actively conducting market research on its ad-free subscription based version. This version, if launched in India in future, may act as a catalyst for converting the Indian social and digital media users from free users to paid subscribers.

From May 1 to May 5, we saw daily news bulletins on internet about Walmart nearing Flipkart deal, described as the largest cross-border M&A deal involving an Indian business. Flipkart issued a statement on May 5 claiming that it has got 70% share of online smartphone sales. To sum up, this deluge of news on digital media which we saw during last week is probably going to be the norm for future as we move towards a Digital India.

In addition to all the above news, we have also seen the promotion of the second edition of Techमंच, by the exchange4media group as the platform for bringing together advertising, marketing and media fraternity for discussing the digital future of India. This event will also see the presentation of the Digital Marketing Awards.

In most developed countries industry and academia are working together to monitor and understand the changes in marketing communication in the digital age, but in India we are yet to see similar interactions and iterations. I am happy to inform the readers of www.mxmindia.com that Symbiosis Institute of Media & Communication is planning an International Conference on New Media in September, 2018 (http://simcicmac.com/).The SIMC faculty would be delighted if people from the M&E industry join the conference and share their experience and contribute to our academic pursuit of understanding effectively the changes in new media formats locally and globally.

Indrani Sen is a veteran advertising professional and is now Adjunct Professor in Media Management with the Symbiosis International University, Pune. The views expressed here are her own.