With every edition of the annual This Year Next Year report, GroupM also presents its trends for the year. Here’s what it presented to the media and the industry at large on Tuesday.

Moving towards attention planning

With the acceleration of digital media and shifting experiences of consumers, it’s important to understand the impact of attentiveness of the consumer as he engages with media/media assets. We have enhanced our understanding on exactly how many impressions for a single medium or multimedia lead to cross-channel optimisation.

What we haven’t been able to capture is the viewability impact of each impression on intent & purchase. The way forward is an “attention response curve”, which allows for new planning and pricing discussions. New measures like quality cost per thousand [qCPM] are beginning to be explored and traded. We need to ensure q is measured in a way that represents real quality.

Content breaks boundaries and creates new opportunities

OTT platforms themselves are becoming popular enough to be licensed into products and promotions. From a marketing and promotion standpoint, brands are looking at leveraging platform like Netflix and Prime Video across their portfolio to create campaigns using multiple shows, movie library and even popular music from some shows. Today we see audience embracing content from multiple geographies and language. A Kashmiri from Srinagar is watching and appreciating Malayalam or Telugu content. We all have seen the audience pan-India celebrate RRR, Pushpa or KGF. We have content in abundance to suite consumption patterns for eclectic/niche audiences as well as the masses.

Likes of Post Malone (Feeding India), Russ (India Tour), Imagine Dragons & Jackson Wang (Lollapalooza) have come to India in the last 12 months; and on the other end we’ve Diljit Dosanjh performing at Coachella 2023 as part of the festival’s expanded global line up. We will more of this in 2023.

The myth that’s getting broken is the belief that typically Indians don’t pay for content & experiences. As mentioned above, we see that Indians actually do pay and they are willing to pay premium for some curated experiences.

From an advertiser POV, these are highly engaged, high-spending audiences, making these events a perfect platform to capitalise on.

Rise in retail media

Retail media in India is expected to double by 2027.

With demand for accountability on every single rupee of ad-spend, retail media offers an end-to-end solution from discovery to shopping, with the ability to connect data between consumer, the online marketplace and brands.

For publishers, monetisation via retail media amplification with the fusion of data and power of programmatic will be growing demand channel.

In India, the rise of adspends on digital retail media will depend on how the retail media networks are able to demonstrate the value by complementing search efforts and not competing with them.

Usage of effective hyper-localised and personalised creative at each stage of the funnel of retail media will be critical in realising the full potential.

While retail media will be used primarily for CPG, it will also be leveraged by non-endemic clients to find audiences with relevant category usage.

Challenges will continue to exist on measurability beyond end level attribution.

At GroupM, we have launched our retail media product named Discovery Commerce. It connects all dots from marketplace insights, media, creative, programmatic to purchase in one funnel.

Visual search goes mainstream

Visual Search delivers instant relevance to a consumer search. It allows users to get exactly what they want rather than a lookalike.

Visual search also allows for conversion of interest in one specific product (e.g. apparel) to the entire collection – expanding the shopping cart It leads to a huge edge on SEO and how we enhance our marketing ROI. While tagging for search typically needed real people to tag individual products, with Visual search the images are SEO ready and increase the chances of discoverability More importantly, marketers can tap into consumers’ state of “What I didn’t know I want” and increase the ARPU.

New dimensions of omnichannel

The dramatic shifts in consumer behaviour during the pandemic saw most agile brands shift to multichannel retail, with ecommerce getting a huge surge.

Post the Pandemic, we are seeing further shifts in consumer behaviour. While ecommerce continues to grow, the rate of growth is slowing down. We are witnessing re-emergence of physical trade, with high street rentals moving up and consumers opting for the joy of physical shopping, touch & feel, etc. We see a rise in “Experience centers” across both traditional and new age brands. The emergence of Metaverse and the growth in AR/VR will power new shopping experiences for consumers.

Brands will go beyond multichannel to deliver a true omnichannel experience. The first step is to recognize consumers across Physical & Online environments and then give them a seamless, consistent and rewarding brand experience at every touchpoint.

Democratisation of commerce with ONDC

ONDC is promising to be the new jewel from the India Stack. What UPI did to payments, ONDC is expected to do to Commerce.

The momentum gained in 2022 will lead to larger participation from brands and marketplaces to be enabled on the ONDC network.

Currently over 22,000+ sellers are on this open network.

With transparency and level playing field for all partners at the core, ONDC will help businesses have more choices, larger demand spectrum and avoidance of search bias.

To build trust in an unbundled and democratic environment, setting up key elements such as Issue and Grievance Resolution, Scoring and Badging, Reconciliation and Settlement, Cataloguing Services will become important.

In 2023, we will see emergence of hyperlocal marketplaces. Your nearest Kirana shop can possibly be enabled on the ONDC protocols.

Birth of ecommerce services companies will increase as India’s share of GMV online increases across categories.

We see exciting times ahead with screen-to-door commerce enabled by ONDC.

Sporting nation in the making

We see a strong move towards localisation of sports, encouraging local/ regional players and providing opportunities for the nation to become a playing nation rather than just a “watching” one.

While top dollars are being committed at the top of the funnel with IPL and ICC Media Rights, we see apps/platforms democratising sports broadcast space at an amateur level by providing streaming platforms to local sports tournaments and amateur games. It’s essentially developing smaller cohorts of sports enthusiasts who play, watch, support and enjoy their friends and family performing on-field at local, community events. With more Indians becoming fitness conscious and participating in active sports, we see this medium developing further, creating and catering to a niche audience and corresponding set of advertisers

Inclusivity becoming mainstream

Indian sports ecosystem went through a metamorphosis in 2008 with the advent of IPL. Cut to 2022, IPL hit an unprecedented high with media rights crossing 100 Cr. per match! While that’s been the headline for the sporting industry, diversity, equality and inclusion has been slowly making its presence felt in the Indian sports arena. We saw early signs of it with Women’s Kabaddi Challenge as a part of Pro-Kabaddi OR Women’s T20 Challenge towards the fag end of regular IPL season. Come Mar 2023, India is ready to host a full-fledged Women’s Premier League with 5 franchises (sold at a whopping total 4670 Cr.) and matches broadcast on Viacom18 network. We expect more of these in days to come.

Docuseries leading to more immersive sports

GenZ is greatly interested knowing the “inside scoop” when it comes to the sports world and that explains the plethora of sports docuseries making its way into our television sets. We expect this to go a notch up with the shift in content happening from the production house perspective to the athlete themselves reliving the moment to their own fans on their preferred platforms. From an advertiser’s lens, as LIVE sports keeps getting more expensive, docuseries and ancillary content in sports becomes a great asset to leverage and engage with passionate fans in a different context.

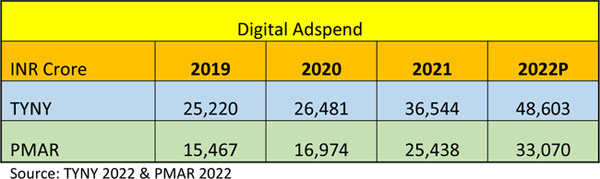

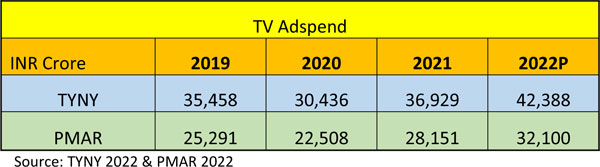

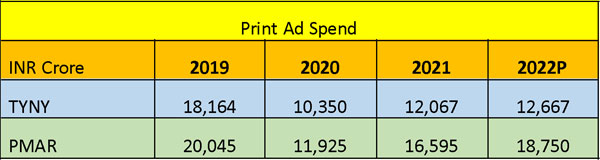

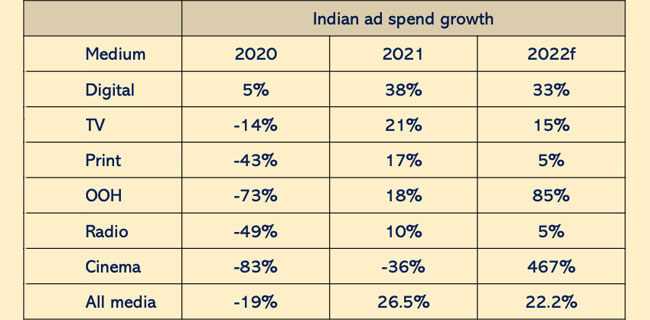

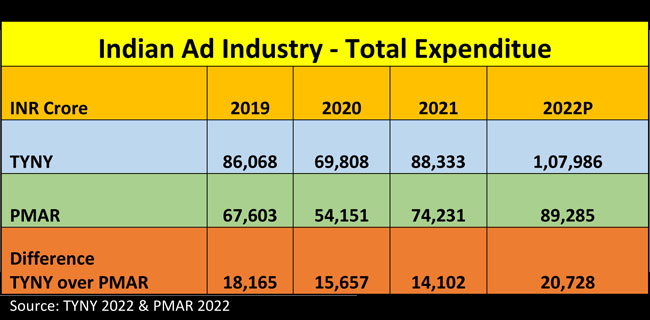

Last week, both GroupM’s This Year Next Year (TYNY) and Madisons Media’s Pitch Madison Advertising Report (PMAR) got released and their basic findings have already been reported by all business and trade media. The general mood in the advertising industry is exuberant as both the reports have confirmed that AdEX zoomed in 2021, by 37% as per PMAR and by 26.5% as per TYNY in spite of the third wave of the pandemic. In 2021, India was the fastest growing market in the top 10 countries, ranking 9 globally and ranking 5 on incremental ad spend predicted for 2022.

Last week, both GroupM’s This Year Next Year (TYNY) and Madisons Media’s Pitch Madison Advertising Report (PMAR) got released and their basic findings have already been reported by all business and trade media. The general mood in the advertising industry is exuberant as both the reports have confirmed that AdEX zoomed in 2021, by 37% as per PMAR and by 26.5% as per TYNY in spite of the third wave of the pandemic. In 2021, India was the fastest growing market in the top 10 countries, ranking 9 globally and ranking 5 on incremental ad spend predicted for 2022.