By Our Staff

PricewaterhouseCoopers (PwC) tabled its 2023 Global Consumer Insights Pulse Survey, which captured the views of 9,180 consumers across 25 territories.

According to the survey, consumers globally are weighed down by concerns around cost of living and personal finances. Around 74% of Indian respondents say they are concerned about their personal finance situation, as opposed to 50% globally. 63% of Indian consumers are cutting back non-essential spending altogether, according to the 2023 PwC Global Consumer Insights Pulse Survey, which captured the views of 9,180 consumers across 25 territories. In India, the survey included 500 Indian respondents across 12 metros, tier-1 and tier-2 cities of India (Mumbai, Delhi-NCR, Bengaluru, Visakhapatnam, Chennai, Kochi, Kolkata, Nagpur, Jalandhar, Hyderabad, Meerut and Rajkot). Out of these, 57% of the respondents were male and 43% were female.

The survey also found most Indian consumers expecting to reduce their expenditure across all surveyed categories over the next six months, a significant decline in planned spend across all categories since the previous pulse survey in June 2022. Industries, including luxury and premium products, travel, and fashion, expect to see the greatest portion of consumer spend reductions over the next six months, whereas the groceries segment is expected to decline the least.

Sharing insights from the survey, Ravi Kapoor, Partner and Leader – Retail & Consumer, PwC India said: “PwC’s latest Global Consumer Insights Survey for India drives home the key message of ongoing financial stress in the lives of the consumers, where 75 percent of them are very concerned about their financial situation. This sentiment will have a potential restraining effect on spends in highly discretionary categories of electronics and luxury. Consumers will continue to demand world-class buying experiences in both physical and digital channels with work cut out for brands to reduce costs, enhance availability, and for ‘going local’. The silver lining here remains the unequivocal growths in adoption of digital channels and the desire to spend more on travel in the coming months.”

Consumers, globally, are shifting their consumption habits in-store and online as the cost-of-living surges and supply chain disruptions impact product availability and delivery times. As a result, almost half (45%) say they are buying certain products when on offer/promotion, 44% are looking to retailers offering better value, 38% are using comparison sites to find cheaper alternatives, 36% are buying in bulk to save cost, and 33% are buying retailers’ personal brands for better savings.

Supply chain disruption is shifting in-store/online consumer behaviour

Half of the Indian consumers (50%) said rising prices remain the most frequently experienced issue when shopping in-store, supply chain issues also dominate with larger queues and busier store locations (35%), along with product availability (28%), which is also impacting consumer behaviour.

Luxury/premium product industry to see decline in consumer spend

Consumers are planning to reduce their spending across all surveyed retail categories over the next six months, with the greatest decrease forecast in luxury/premium products or designer products (38%), virtual online activities (32%), consumer electronics (32%) and fashion products (clothing and footwear) (31%). However, there remains an appetite for future spend, with 38% indicating they will look to treat oneself/others, whereas 54% view them as better quality. Travel (30%) and groceries (21%) had the least reported planned spend reduction.

Vocal for local (Sustainable products are in demand from consumers)

Despite a planned spend reduction and a challenging economic environment, consumers say they are still willing to pay more for sustainable products. Overwhelmingly, more than 88% are willing to pay higher for a product that is produced/sourced locally, or made from recycled, sustainable, or eco-friendly materials (87%), or produced by a company with a reputation for ethical practices (87%).

Metaverse: Early-stage adoption strong, executives recognise the importance of risk management, cyber security and governance

Adoption of the Metaverse as a shopping channel is still in its early stages, however, the medium remains under-utilised, with only one-quarter (23%) of Indian respondents familiar with the term. The largest portion of these users have primarily employed the Metaverse for virtual reality (VR), i.e., playing games or watching a movie (20%), experiencing the virtual world through the retail environment or a concert (13%), or purchasing a digital product, such as a Non-Fungible Token, or NFT (17%). Millennials (36%) are most likely to use the Metaverse, especially in countries like India (48%), Vietnam (43%), and Hong Kong (42%).

All the while, as online shopping continues to grow in volume, consumers are increasingly weary of data privacy. 65% of respondents are extremely or very concerned when interacting with social media companies, third-party/portal travel websites (54%), healthcare (59%), and consumer companies (58%). As a result, 41% respondents do not share more personal data than they must, 37% opt-out from receiving communications from these companies, and 38% have overall reduced their interaction with these types of companies.

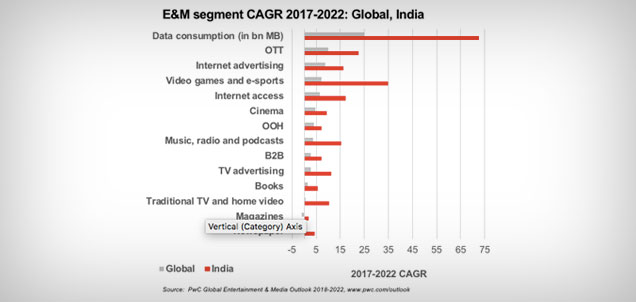

PWC’s 23rd annual Global Entertainment and Media Outlook released on June 23, 2022 shows that globally after a setback in 2020 due to the pandemic, the entertainment and media industry is set on a steady path of recovery with a CAGR of 4.6% during 2021-26 to reach a market size of US$ 2.9 trillion in 2026 as shown in the chart below.

PWC’s 23rd annual Global Entertainment and Media Outlook released on June 23, 2022 shows that globally after a setback in 2020 due to the pandemic, the entertainment and media industry is set on a steady path of recovery with a CAGR of 4.6% during 2021-26 to reach a market size of US$ 2.9 trillion in 2026 as shown in the chart below.