By Indrani Sen

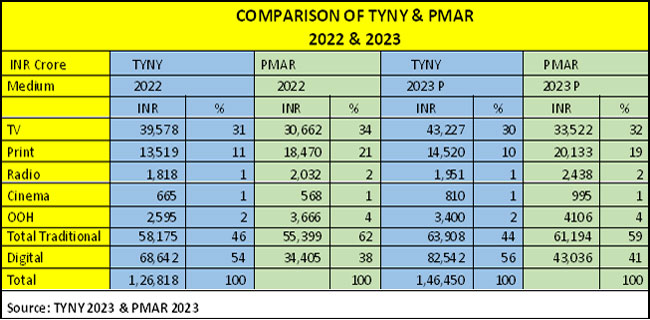

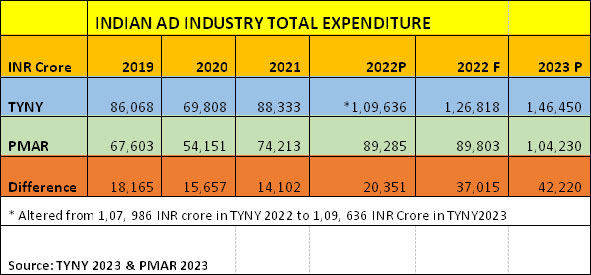

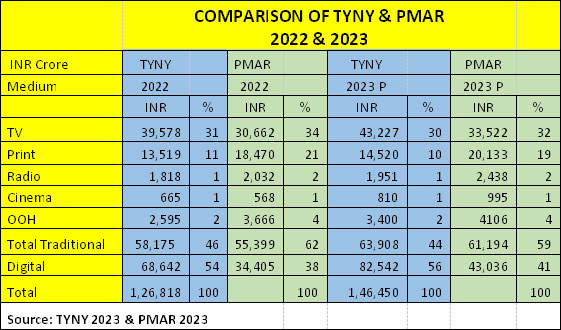

It is time to celebrate as the TYNY (This Year Next Year) 2023 report released by GroupM last week declared that the total value of Indian AdEx in 2022 has crossed the 100K crore mark touching INR 1,09,636 crore and in 2023 is estimated to grow at a healthy rate of 15.5% over 2022 towards another milestone of 150K crore (predicted as INR 146450 crore in 2023). Digital AdEx with an estimated 30% growth rate is expected to power the overall growth. India continues to be the fastest growing advertising market and as per the TYNY report has moved up from 9th position to the 8th position among the Top 10 countries with a share of 2% of the global adspend.

It is time to celebrate as the TYNY (This Year Next Year) 2023 report released by GroupM last week declared that the total value of Indian AdEx in 2022 has crossed the 100K crore mark touching INR 1,09,636 crore and in 2023 is estimated to grow at a healthy rate of 15.5% over 2022 towards another milestone of 150K crore (predicted as INR 146450 crore in 2023). Digital AdEx with an estimated 30% growth rate is expected to power the overall growth. India continues to be the fastest growing advertising market and as per the TYNY report has moved up from 9th position to the 8th position among the Top 10 countries with a share of 2% of the global adspend.

As per the tradition set up over the last few years, the PMAR (Pitch Madison Advertising Report) 2023 was also released last week with a prediction that Indian AdEx will cross 100k crore mark in 2023 (predicted as INR 104230 crore) with a growth rate of 16% over 2022. Digital AdEX with an estimated 25% growth rate provide momentum to the growth.

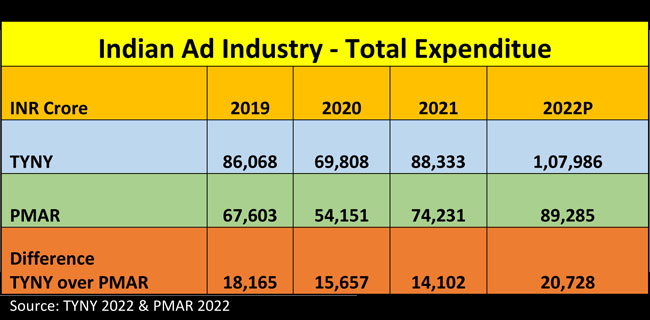

Both the TYNY and PMAR have been predicting in the same line over last few years with the gap between their estimates of the size of Indian AD Industry becoming wider year on year. By 2023 the size of the gap in the two estimates will be 40% of the total Indian ADEX size estimated by PMAR and by 2025 the size of the gap may become 50% of the Indian ADEX estimated by PMAR!! Globally is quite common to have difference in the estimates of the AD Industry size / AdEX estimated by different organisations, but if the difference becomes huge then it causes serious concern.

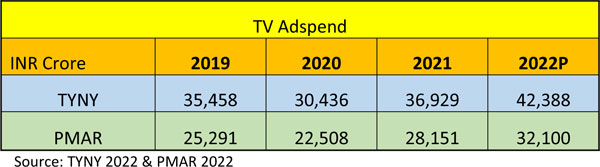

Six years back, I wrote here an article comparing the estimates of TYNY 2017 and PMA 2017 https://www.mxmindia.com/2017/02/what-is-the-real-size-of-indian-ad-industry/. In that year, the estimates for Digital AdEx by the two agencies were almost the same, INR 7000+ crore in 2016 and INR 9000+ crore in 2017. However, the TV AdEx estimated by TYNY was considerably higher than the TV AdEx estimated by PMAO and hence the total Ad Industry expenditure estimated by TYNY was around INR 6000 crores higher than the that of PMAO.

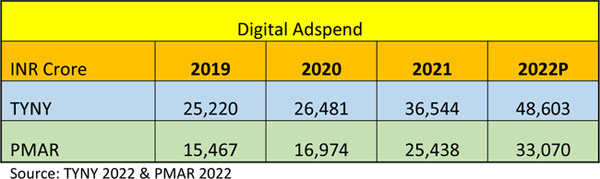

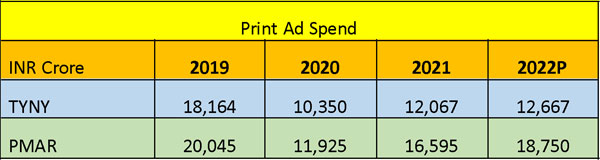

It is interesting to note that over the last six years, Digital AdEx has increased at a much higher rate in the TYNY reports than in the PMAR reports. In 2022, the Digital AdEx INR 68,642 crore reported by TYNY was double the estimate INR 34,405 crore shown by PMAR. AS per the TYNY report, Digital ADEX now has more than 50% share of the total AdEx, while in the PMAR report total traditional media is still enjoying around 60% share of the total AdEx as shown in the table below.

The various industry websites including www.mxmindia.com and financial/ business publications have already reported on the findings of the two reports. Digital did not suffer during the three waves of Covid-19, among the traditional media TV was the first to recover its pre pandemic revenue, outdoor recovered in 2022, print, radio and cinema are expected to recover in 2023. On the whole. 2022 was a good year for Indian Advertising and the immediate future looks bright.

In spite of the widening rift between the TYNY and PMAR estimates, their leaders agree on the future directions. Prasanth Kumar, South Asia CEO, GroupM has said “As technology redefines interactions between consumers, brands and businesses the ad industry must navigate thru this changing environment.” Sam Balsara, Chairman and Managing Director, Madison World has advised the advertisers “to take advantage of the evolved digital infrastructure for distribution and advertising to prepare for the future growth and to invest in building their own D2C channels.” Only if the two agencies could stop the widening rift between the two reports, we would be in a happier situation.

Indrani Sen is a veteran industryperson and educator. This is a new season of her Monday column on MxMIndia. Her views here are personal.

By Indrani Sen

By Indrani Sen