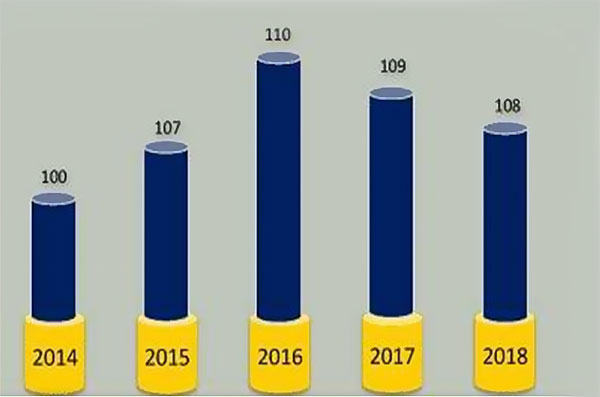

According to a report published in Brand Equity on February 27 based on TAM AdEx data based mainly on display ads, print advertising volumes are up by 8% from 2014 to 2018, though after 2016 there has been a decrease in print advertising volumes in the next two consecutive years. (https://brandequity.economictimes.indiatimes.com/slide-shows/print-advertising-volumes-up-8-between-2014-2018-tam-adex/68172547).

Source: TAM AdEx/ ET Brand Equity

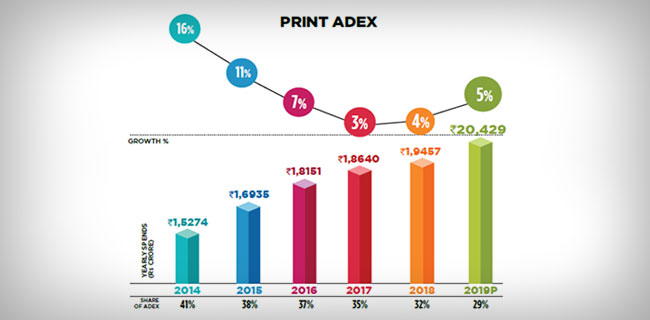

If we compare this growth in volume with the growth in value as reported In PMAR 2019, we find that though there has been a growth in the print advertising Value by 27%Â from 2014 to 2018, the share of print Advertising in the total advertising pie has been decreasing steadily.

Source: PMAR 2019

As shown by PMAR 2019, from 2014 to 2018, the share of print advertising in the overall advertising pie reduced from 41% to 32%, a 9% drop in 5 years. In another five years, the share of print advertising in rupee value may come down to below 20% in India. The writing is clear on the wall as reflected in the diminishing/ stagnant growth rate of print advertising value.

If we compare the above two charts, then we find that in terms of value, print advertising has grown by 27% from 2014 to 2018 as against only 8% increase in volume. Over the next five years, there may be still a growth in value of print advertising, but in terms of volume it may show a diminishing trend as reflected in the TAM AdEx comparative analysis of ad volumes across media in 2017 and 2018 where we find that magazines have lost 6% of ad volume from 2017 to 2018.

Source: TAM AdEx/ ET Brand Equity

So, print media needs to work out a strategy for survival which lies on one hand in promoting and monetising their online editions and on the other hand in innovative ways to tie up with other media which are still showing growth in both volume and value.

In another recent article, Vanita Keswani, CEO of Madison Media Sigma, suggested that “Print ads will be more effective if they complement digital campaigns and entice readers to interact with brands online†(https://brandequity.economictimes.indiatimes.com/news/business-of-brands/what-print-media-needs-to-do-to-win-back-advertisers-faith/67959125). This solution however requires active support from the creative and media agencies which may not work out across categories and brands. It may be worthwhile for the newspapers to look at categories like Two-Wheelers, Cars & Jeeps and Services which are the leading contributors to the Print AdEx volume and experiment with strategic integrations.

Last week, the advertising and media industry probably had an overdose of data and information to chew, both GroupM and Madison released their annual reports on industry AdEx “This Year Next Year†(TYNY) 2019 and “Pitch Madison Advertising Report†(PMAR) 2019; Dentsu Aegis Network’s arm Posterscopre released a forecast for only OOH industry followed by the TAM AdEx Report and the results of the DD Free Dish e-auction held from February 11 to 14, 2019. It will not make any sense to discuss the implications of all the reports together. Let me today take a look at TYNY 2019 and PMAR 2019 released by GroupM and Madison.

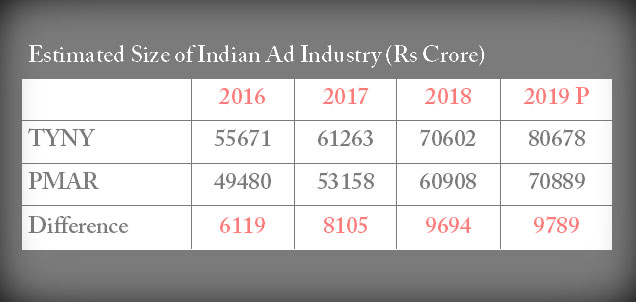

By now, industry professionals are reconciled to the reality that there is a big gap in the estimation of the size of the Indian Ad Industry by the two agencies. However, as an academic I find it difficult to explain the reasons of the same to my students. I was alarmed to find earlier that since 2016, the gap in real terms increased year on year till 2018 as shown in the chart below. It is reliving to find from the recent reports that the same is not increasing further in the estimates made for 2019 by GroupM and Madison. We can probably hope that in another few years the difference between the two estimates will be reduced to 4% to 8%, the acceptable statistical margin of error at the 95% confidence level.

Estimated Size of Indian Ad Industry (Rs Crore)

2016

2017

2018

2019 P

TYNY

55671

61263

70602

80678

PMAR

49480

53158

60908

70889

Difference

6119

8105

9694

9789

A comparative analysis of the 2018 adspends by media made in the two reports show that the main bone of contention between the two is in the estimated size and share of TV media. Apart from TV, the differences in the estimated size in rupee value of Print, Digital and Radio fall within the acceptable margin of error ranging from 4% to 8%.The estimated size in rupee value are very close for OOH and same for Cinema. The detailed analysis is given below:

Indian Ad Industry 2018: Estimated Size (Rs Crore) & Share (%)

Rs. Crore

2018 f

Â

2018

Â

Media

TYNY

%share

PMAR

%share

TV

33577

48

23432

38

Print

17970

25

19467

32

Digital

12337

17

11706

19

OOH

3202

5

3365

6

Radio

2709

4

2144

4

Cinema

806

1

805

1

Total

70602

100

60908

100

Growth over last year

11%

Â

12%

Â

In terms of forecasts for 2019, the growth rates predicted by TYNY for different media are lower than the growth rates predicted by PMAR, apart from Radio where TYNY has predicted a higher growth rate than PMAR. Both the reports agree that the highest growth rate will be in Digital media fuelled by mobile, online video and social media, followed by Cinema though on a very small base. In terms of overall growth, TYNY has pegged it at 14%, 2.4% lower than the prediction of PMAR at 16.4%.

Indian Ad Industry Forecast

2019p

2019p

Rs Crore

TYNY

% Â Share

Growth %

PMAR

% Share

Growth %

TV

38612

48

15

27649

39

18

Print

18368

23

2

20442

29

5

Digital

16038

20

30

15612

22

33

OOH

3536

4

10

3750

5

11

Radio

3116

4

15

2401

3

12

Cinema

1008

1

25

1047

1

30

Total

80678

100

14

70889

100

16.4

Both the agencies have cited upcoming Parliamentary elections and ICC Cricket World Cup 2019 as major contributor to the growth in ad spends in 2019. While Madison have cited increase in government spending to showcase its achievements, the growth of OTT, increased spending in rural sector and India moving to a consumption society as the other reasons for predicting a high growth for the ad industry, GroupM has highlighted major trends like emerging technology, availability of data, content creation and distribution, etc. as factors contributing to the growth in advertising expenditure. There is no doubt that after two bad years in 2016 and 2017, Indian advertising industry has turned around in 2018 and is poised for further growth in 2019.

Let me turn around and play the role of Devil’s advocate musing over what can disrupt the rosy dreams of advertising industry during next year. Over the last four days all of us are reeling under the effect of the terrorist attack in Pulwama killing 40 CRPF jawans. The entire nation wants revenge and our expectations have increased since the last surgical attack. Such attacks and counter attacks may lead to unforeseen developments affecting our economy and business.

After the results of the last round of state elections, many political analysts think that BJP may have to depend on coalition with other political parties to run the Government in Centre after the next General Election which may affect smooth functioning of the Government. The gross overspending (Rs. 99610 crores over approved expenditure) by the Union Government as reported recently by CAG may have a diverse effect on various government approved projects in future as well as rural development.

If RBI falls in line with the directives of the Finance Ministry, then India’s financial ratings may suffer globally and rupee may face further devaluation in its foreign exchange rate. There could be changes in the domestic as well as foreign policies of US which will have far reaching effect on the entire world and India will not be an exception. To sum up, we are living in very uncertain times when any significant change in internal or external political situations or foreign/ economic policies can adversely affect the growth of our advertising industry. Let us keep our fingers crossed and hope that the predictions for the growth in advertising in 2019 made by TYNY and PMAR will be realised without any major disruption.

List of my articles related to this topic over last three years:

Feb 20, 2018 Mind the TV AdEx Gap

Feb 20, 2017 What is the real size of the Indian Ad Industry

Nov 21, 2016 Post Demonetisation, it’s boom to doom for ad spends

Feb 15, 2016 Boomtime for Media: A Review of Pitch Madison Advertising Report 2016