By Indrani Sen

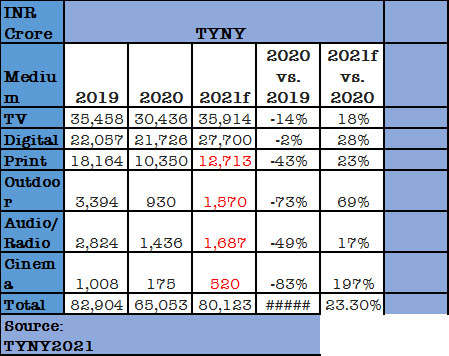

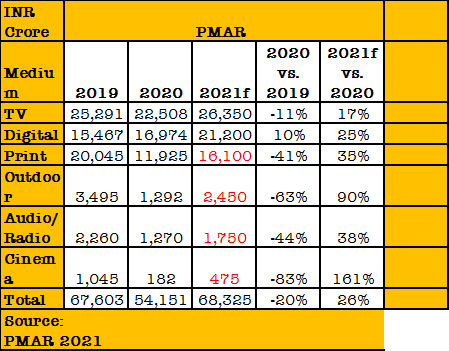

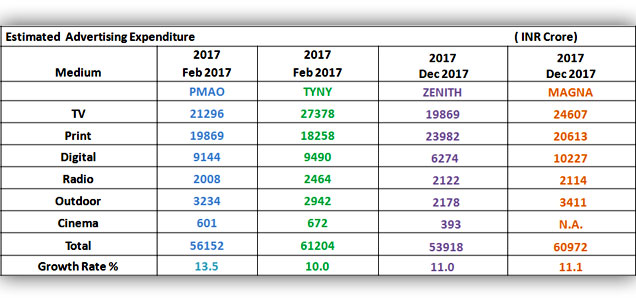

Like every year, last week we saw the release of both This Year Next Year 2021 (TYNY2021) by GroupM and Pitch Madison Advertising Report 2021 (PMAR2021) by Madison Media. Both agreed that the pandemic year 2020 was a disastrous one for the Indian Media and Advertising Industry, when the overall AdEx dropped by 20% (PMAR2021) to 21.5% (TYNY2021) from the 2019 level. Both have predicted better days in 2021 with the overall AdEx growing by 23.3% (TYNY2021) to 26% (PMAR2021). According to PMAR2021, the predicted AdEx INR 68,325 crore in 2021 will touch the AdEx INR 67,603 crore in 2019. According to TYNY2021, the forecast for 2021 is INR 80,123 crore, which falls short by 3.35% from the AdEx in 2019 which was INR 82,904 crore.

Like every year, last week we saw the release of both This Year Next Year 2021 (TYNY2021) by GroupM and Pitch Madison Advertising Report 2021 (PMAR2021) by Madison Media. Both agreed that the pandemic year 2020 was a disastrous one for the Indian Media and Advertising Industry, when the overall AdEx dropped by 20% (PMAR2021) to 21.5% (TYNY2021) from the 2019 level. Both have predicted better days in 2021 with the overall AdEx growing by 23.3% (TYNY2021) to 26% (PMAR2021). According to PMAR2021, the predicted AdEx INR 68,325 crore in 2021 will touch the AdEx INR 67,603 crore in 2019. According to TYNY2021, the forecast for 2021 is INR 80,123 crore, which falls short by 3.35% from the AdEx in 2019 which was INR 82,904 crore.

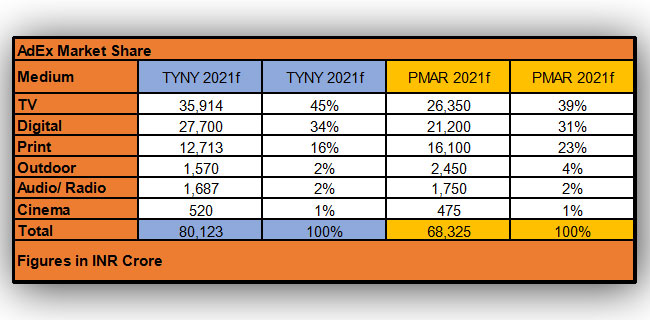

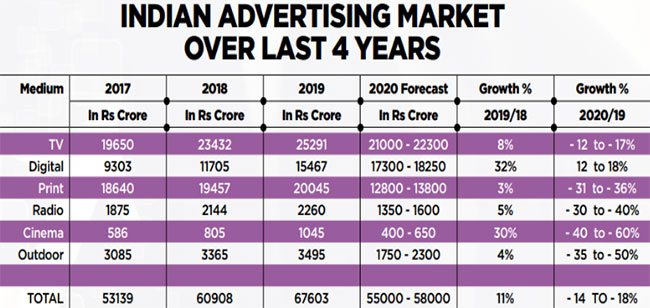

In spite of the huge gap in the overall AdEx estimates by the two agencies, it is relieving to find that the trends predicted by both of them are similar. The gap in the estimated size of the Indian AdEx between the two reports has been existing over many years and the Media and Advertising Industry has learned to live with the differences. TYNY2021 has estimated both TV and Digital AdEx at much higher levels than PMAR2021. On the other hand, PMAR2021 has estimated Print AdEx at a much higher level than TYNY2021. The following two tables show the details of the two reports by medium for making easy comparisons.

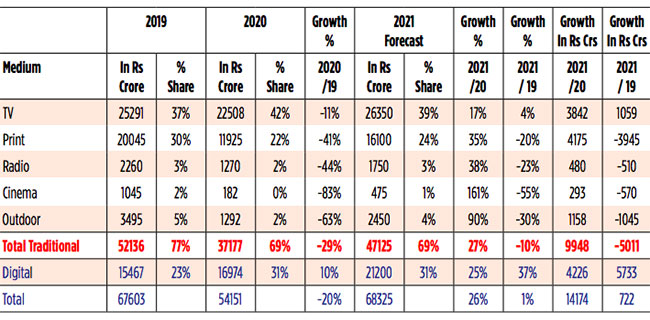

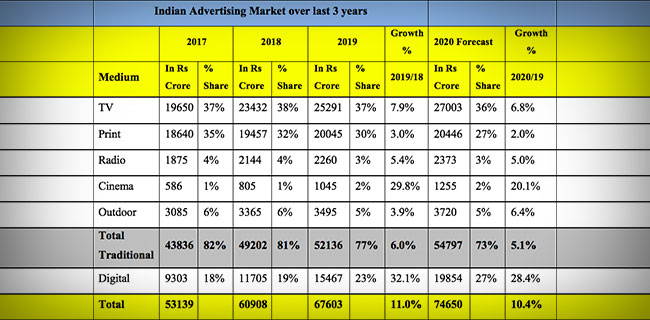

According to PMAR2021, the pandemic year 2020 will go down in the history of Indian Media and Advertising as the year when Digital overtook Print and became #2 in terms of market share of overall AdEx. However, TYNY2019 showed Digital as the #2 and Print in the #3 positions in terms of market share. In 2020, GroupM estimated a 2% degrowth in Digital from 2019 level, while Madison Media estimated a 10% growth in Digital over 2019 level. Both the reports show Print AdEx in 2021 would be below the 2019 levels, while Digital AdEx would be crossing the 2019 levels in 2021. So, we can now conclude that Digital has the second highest market share in overall AdEx and it is unlikely that Print would be able to regain that position in 2021 or later.

TV which holds the #1 position in Indian AdEx in both the reports, had degrowth of 11% (PMAR2021) to 14% (TYNY2021) last year, but is expected to grow at higher rate 17% (PMAR2021) to 18% (TYNY2021) in 2021 and touch or cross the 2019 AdEx levels.

Both the reports show the huge loss which was suffered by the other traditional media, Outdoor, Radio and Cinema during 2020. In spite of the overall growth of AdEx predicted for 2021, these three media would be far below their 2019 benchmarks. The combined market share of these three media continues to be less than 10% in both the reports. A difference in reporting between TYNY and PMAR has been noticed this year regarding Radio. While PMAR2021 has reported only on Radio, TYNY2021 has changed the nomenclature to Audio. It is however not very clear what other audio component apart from Radio has been included under that definition.

It is encouraging to find from the two reports that the worst effect of pandemic is over; Media and Advertising industry is on the path of recovery; the process of digitisation has been accelerated; we are expecting a robust GDP growth and globally India will continue to be the second-fastest growing AdEx market among the top ten countries in 2021. At the same time, it is also frightening that the economic effects of Covid-19 have manged to wipe off two years of overall AdEx growth (2020 & 2021) and many media-owners and some media agencies still have to fight battles for survival.

By Indrani Sen

By Indrani Sen