By Sam Balsara, Vikram Sakhuja & Nilesh Bagaria

Key Findings – 2015

1. The Indian advertising industry in 2015 grew by another 17.6%, close on the heels of

LY growth of 16.5%. This growth is 4 percentage pointshigher than our mid-year projections of 13.8%. The Indian Media Industry is BOOMING, like never before. It is interesting to note that it took 5 years (2008 – 13) for Industry to add Rs10586 crores,moving up from Rs21520 crores to Rs32106croresbut only 2 years (2013-15) to add Rs11885 crores to reach Rs43991crores. With this growth, India finally earned the distinction of being the fastest growing Advertising market in the world.

In terms of absolute numbers, the Indian advertising industry has increased by Rs.6,586crores to touch Rs. 43,991crores in 2015. The categories who have contributed most to the overall growth in 2015 are FMCG, E-commerce,Autoand Telecom/DTH. FMCG continues to be the most dominant sector with a 28% share of the total Indian advertising industry followed by E-commerce (10%) & then Auto (9%). Contrary to the general perception that it is E-commerce that has taken the media market by storm, it is good old FMCG that has contributed more than Rs 2050 Crores to the overall growth. E-commerce came a distancefourth with a contribution to the overall growth of Rs793 Crores. E-commerce, though has become the second largest category, a distant second, but second, after FMCG

2. TV has grown by a whopping 22% to reach Rs. 17,261crores and is on track with our mid-year projections of 21% growth. With close to 40% share, television continues to be  the largest contributor to the advertising pie. In terms of absolute numbers, TV advertising has grown by Rs. 3,103crores

- The main categories who have fuelled the overall growth ofRs 3103crores in 2015 are FMCG (Rs1413crores), Telecom/DTH (Rs499crores), E-commerce(Rs 457crores ) and Auto (Rs 326crores)

- E-commerce category grew dramatically by 60% to reach Rs 1223crores. However in absolute terms it contributes only 7% to overall TV market

- 2015’s biggest cricketing event ICC Cricket world Cup contributed approxRs 500 crores tothe overall growth. IPL had another successful year and netted almost Rs 1000 crores in 2015

- In terms of category contribution, the pecking order remains the same with a marginal 2%agepoints shift in contribution from FMCG to E-commerce.FMCG however, continues to rule the roost contributing 52% share of total TV spends (down from last year’s 54%), followed by Telecom / DTH (10%) & Auto (8%).

- Looking at genres, within Television, Hindi GEC contributes nearly 28% of the overall TV revenue and continues to remain the leader of the pack. In terms of growth, Hindi GEC, Sports and South regional show substantial increase.

- With all networks selling HD channels separately for regular as well impact properties, revenue from HD channels has grown dramatically in 2015 although the base is very small still.

- The impact of TRAI’s 10+2 ruling seems to be on the wane, with many channels having telecast more than 12 mins/hr of FCT. This has also been confirmed by TRAI in their latest press release. This increase in FCT has also been a major contributing factor to the dramatic increase of 22% in the TV Advertising Market.

3. Print has also grownsubstantially, by as much as 11% (compared to our forecast of 5.3 %) to reach Rs. 16,935crores and continues to be the second highest contributor after TV to the total advertising pie, with a share close to 39%. While dailies increased by 12% in 2015 over 2014, magazines as a medium failed to gain advertiser interest and has seen anegative growth of 3% in 2015. Nearly 70%, of Print’s growth of Rs 1661 crores is accounted by just 3 categories-Ecommerce (Rs 398 crores), FMCG (Rs393crores)and Auto (Rs360 crores). Another 22% is accounted by Education (Rs 224crores) and HH durables (Rs 144crores) to the overall growth.

In terms of category contribution, the decision of many publishing houses to follow a differential pricing for FMCG has begun to bear results and now FMCG is also the largest contributor to the Print Pie, with a contribution of 15%. Automobiles is second largest contributor at 13%, followed by Education (10%). Also whilst in contribution E-commerce comes way down, it shows the highest growth of 120%.

While only 4 categories account for 75% of Television advertising, it takes as many as 10 categories to contribute the same to print advertising demonstrating that print is less vulnerable to any category degrowth.

In terms of Volume Cc among dailies, Hindi publications continue to be ahead of English Dailies. Hindi publications contribute 35% of the total volume while English publications contribute 25 %.In our estimates, though in terms of growth of volume Ccboth English& Hindi publication have grown at same rate of 7 – 8%. Telugu publications also grown at the same rate.Bengali & Oriya publicationsshows the highest increase of 13 – 14% but Gujarati publications show a decline of 4%.

4. Digital – At 29%, growth in digital media is in line with our earlier expectation. Digital advertising market now crosses the Rs. 5000 crore mark.

Though the absolute spends on Search have increased, its share of the digital pie has gone down due to the fact that video, social and mobile display have grown at a faster rate last year. Desktop display growth has also further slowed down, as mobile is the all –pervasive platform of choice today.

While E-commerce players are by far the biggest spenders on digital, spends are skewed towards Search and Social with Mobile as a key platform. The uplift in Video comes from the fact that more and more FMCG players are using the digital space to reach out to their audiences to support their television campaigns.

5. Radio has grown by 20% in 2015 to become aRs1545 croremarket and has maintained its share of the total Advertising pie at 3.5%.In terms of absolute numbers, Radio advertising has grown by Rs. 260 crores.

E-commerce advertisers have emerged as one of the main contributors to the growth followed by Automobiles category. Revenue from Ecommerce players in facthas almost doubled in 2015 on Radio on account of various offer-based tactical campaigns. Automobile category has grown by more than 36% on radio in 2015 on the back of new launches across segments.

In terms of category contribution, Real Estate &FMCG sector continue to lead the pack contributing to 10% each of total Radio spends followed by Telecom / DTH& Auto sector (both at 7%).E-commerce now shows up as a major contributor at 6%.

The growth has come on the back of higher inventory sold across stations.

6. OOH –Our OOH estimates now include Digital OOH & Malls which are growing quite rapidly and hence we have re-cast OOH revenue figures for last 3 years when this sub segment began to emerge. Digital OOH & Malls revenue are estimated at Rs 300 crores in 2015 (Digital OOH & Malls netted additional 100 Crores in 2014 & 50 crores in 2013). The OOH market has grown by  14%, in 2015. Transit media though grew by 13%.

In terms of absolute numbers, OOH advertising is now a respectable Rs 2665 crores market. Retail, Real Estate & Automotive continue to be thetop 3 categories in terms of contribution.

Highest growth was in E-Commerce category (110%) followed by Automotive (66%), both together, contributing 60% of the overall growth. The usual big spenders- TV Channels, Banks, Print Media, Mutual Funds etc reduced their OOH spends in 2015.

FMCG which is the largest contributor to TV, Print & Radio does not use OOH substantially except perhaps HUL, therefore FMCG contribution to OOH is only 7%

In terms of city wise spread, Mumbai continues its lead as a major contributor (22%) followed by Delhi (19%). Bangalore replaces Kolkata as the number 3 city with a contribution of (10%).

OOH has maintained its contribution to the total media pie, at 6%.

7. Cinema

We recognize that we have under-reported cinema advertising in our earlier estimates. Cinema advertising from various government agencies and many local / retail advertisersusing static slides are  a substantial contributor and growing quite rapidly. Therefore we have included spends by these advertisers for this year and also in our estimates of previous years.

This has led Cinema to grow by 21% and now contributes 1% to the total advertising pie with total revenue of Rs. 465 crores in 2015. The multiplex boom in smaller towns, digitization of single screens, and substantially increased activity on marketing of movies (both Bollywood & Hollywood)has created interest around the medium thathas attracted new advertisers.

8. Top Advertisers of India.This year in response to many requests from the advertising & media professionals, we are releasing approximate spends of top 50 advertisers of India for the year 2015.

Advertising continues to be a game of the big boys. Top 50 advertisers account for 36% of the advertising market. This number is significant considering that there are over 2 lakhs advertisers in Print and over 12000 advertisers in TV. Top 10 advertisers account for as much as 17% of the total market and contribute to 47% of the total 50 list. By the time you reach rank 50, you are down from 2300 – 2500 crores to a 100 – 150 crores. A note of caution, some advertisers who in our list  rank between 50 – 60 may well be in reality in the top 50 list or vice-versa.

HUL continues to lead the pack with  spends of about Rs. 2500 crores followed by Amazon India, Procter& Gamble,  Flipkart,Maruti Suzuki, Mondelez, Godrej,ITC, Snapdeal and Reckitt who has spends  between 400 – 1000 crores and who make up our Top Ten list.

We may mention that many Madison clients feature in this list but we hasten to add that we have not used confidential information that we are privy to in arriving at this list. The list has been arrived at using a standard structured process.

HUL also leads the pack of top advertisers in OOH media for the year 2015

2016 Forecast

Our prognosis for 2016 is that it is going to be yet another GOOD YEAR for Media. In arriving at the numbers we are conditioned by the fact that the Indian economy has become the fastest growing economy of the world; our GDP growth rate at 7%+ is the envy of the western world, now looking at India in new light; our BJP govt tells us that it has made a number of structural interventions to prepare the economy for high growth and continues to remind us that they are strongly focused on stimulating the country’s economic growth for which pro- business policies are essential; at the same time not ignoring subsidies for the poor, which should also add to purchasing power of Rural India and finally Commodity prices including that of Oil are likely to remain soft throughout 2016. Although Indian businesses have expressed concern that all the positive actions taken by the Govt. have not resulted in growth on the ground, we feel that India Inc. remains very optimistic about India’s future and they will once again invest heavily in advertising to protect and gain market share of their brands and also launch  a number of new brands and variants and ecommerce platforms and apps to capture the imagination and meet the requirements of modern India.

All this will help the advertising market cross the Rs. 50,000 croremark.

1. We expect the market to grow by more than Rs. 7300 crores to reach a total size of Rs. 51365 crores, which represents a growth of 16.8% over 2015. India will also retain the distinction of being fastest growing advertising market in the world for the second consecutive year.

On the supply side a big contributor of this growth will be the ICC Cricket T20 World Cup and the busy schedule of India Cricket for next 6 months. TV will continue as the largest contributor to the overall advertising pie with a share of 40% gaining a further one percentage point. Share of digital spends will increase to a respectable 13% of the overall advertising pie.

2. TV: Paradoxically, as India races to have 500 million users on the Net, we expect TV, most Brands’ all-time favourite medium to grow by another Rs 3450 crores or 20% in 2016 to reach a total figure of Rs. 20,713 crores.

Factors that will lead to this high growth are:

- Organic growth coming from the largest contributor to TV Market, FMCG.

- Entry of new Chinese manufacturers that will enter India specially in Electronics and Mobile Handsets like Vivo, Xiomi, Le-Eco and many others.

- Big bang launch of Reliance 4G services Jio anytime soon, and the defensive efforts of existing telecom operators.

- Â 30 new car and 25 new two wheeler launches expected in the Auto industry.

- Continued emergence of new E-commerce advertisers, covering more and more categories and new services.

- Election campaigns of Political parties, given that 5 State assembly elections in Tamil Nadu, West Bengal, Assam, Pondicherry & Kerala are scheduled in  2016.

New channel launches from existing networks will increase inventory supply to absorb this growth, as also the inevitable rate increases.

3. Print: We expect the Print advertising market to grow by a further 10% in 2016, mainly from dailies, taking the total print market close to Rs. 18,600 crores. Most of this growth will come from language publications and new editions by regional publishers that will attract new Retail advertisers.

Other factors contributing to growth of Print advertising market are likely to be:

- Election campaign in the 5 States heading for Assembly Elections this year

- Organic growth from various Print loyalists  like Auto, Durables and Education.

- Big Bang launches, using Front page jackets by new Mobile apps and stream of tactical offers by Ecommerce and Retail companies

- Multiple launches across both 4-wheelers and 2-wheelers from all leading auto companies

4.      Digital

We expect Digital to gain momentum and grow by about 30% in 2016 to reach close to Rs 6,650 crores. Search spends are likely to stabilize and Desktop Display would see a further downward trend in terms of share of pie.

Programmatic Buying has seen some traction in 2015; this is likely to get further strengthened in 2016. With more users on mobile, spends will be strongly focused on this platform; and whether it is Search, Social or Video, about 80% of all ad impressions will be delivered on the mobile device.

As the reach of digital crosses 400mn, digital will start coming into its own; some advertisers will begin to use it  as a reach and awareness building medium; it will, however, not lose its importance as a ‘conversion’ or ‘performance’ medium and as a strong support medium to TV.

FMCG, telecom, consumer durables, real estate, apparel and BFSI will continue to be growth drivers; E-Commerce will remain the backbone of the industry.

5. Radio: We expect Radio to grow by 18% in 2016 taking the total Radio Advertising market close to Rs. 1,800 crores

Factors contributing to this growth will be:

- Election campaigns in the 5 States heading for Assembly Elections this year.

- Multiple launches across both 4-wheelers and 2-wheelers from all leading auto companies

- Many new radio stations emerging  after winning bids in the recently held Phase 3 auctions.

6. Outdoor: We expect Outdoor to grow by 13% in 2016 Â taking the total Outdoor Advertising Market to more than Rs. 3000 crores.

Many of the factors outlined for Print and Radio will also be responsible for driving the growth of Outdoor. We see also a higher adoption of Digital and Technology and greater usage of Transit Media at Airports and Metros .

7. Cinema: We expect cinema to grow by 15% in 2016 taking the total Cinema Advertising revenue to Rs. 535 crores.  Digitisation of single screens, presence of multiplex screens in tier-II and III towns & increasing popularity of Hollywood & Regional films in India are expected to fuel the growth of Cinema advertising.

In conclusion, 2016 promises to be yet another high growth year for the Indian advertising market. Perhaps no market anywhere in the world has grown consistently across last 3 years to achieve a growth of 60 %from 2013 to 2016.In the previous 3 years from 2010 – 2013, the growth has only been 28%.

Paradoxically the market enablers are growing at a faster rate than the markets they hope to stimulate. Not many categories in the past 3 years would have grown by 60%.

Â

A sure sign that India Inc. has confidence in India’s future.

Source: Madison World

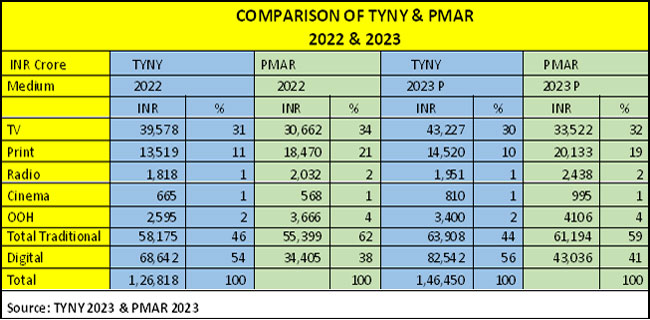

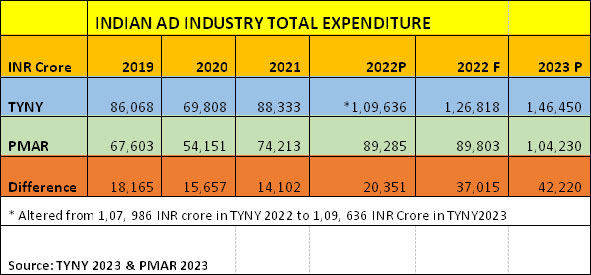

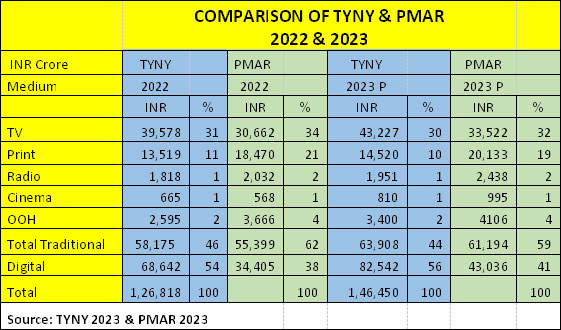

It is time to celebrate as the TYNY (This Year Next Year) 2023 report released by GroupM last week declared that the total value of Indian AdEx in 2022 has crossed the 100K crore mark touching INR 1,09,636 crore and in 2023 is estimated to grow at a healthy rate of 15.5% over 2022 towards another milestone of 150K crore (predicted as INR 146450 crore in 2023). Digital AdEx with an estimated 30% growth rate is expected to power the overall growth. India continues to be the fastest growing advertising market and as per the TYNY report has moved up from 9th position to the 8th position among the Top 10 countries with a share of 2% of the global adspend.

It is time to celebrate as the TYNY (This Year Next Year) 2023 report released by GroupM last week declared that the total value of Indian AdEx in 2022 has crossed the 100K crore mark touching INR 1,09,636 crore and in 2023 is estimated to grow at a healthy rate of 15.5% over 2022 towards another milestone of 150K crore (predicted as INR 146450 crore in 2023). Digital AdEx with an estimated 30% growth rate is expected to power the overall growth. India continues to be the fastest growing advertising market and as per the TYNY report has moved up from 9th position to the 8th position among the Top 10 countries with a share of 2% of the global adspend.

By Indrani Sen

By Indrani Sen