By Indrani Sen

The right thing at a wrong time is a wrong thing.

The right thing at a wrong time is a wrong thing.

Taking liberty with the words of Charles Dickens, one can say this is not the best of times; this is probably the worst of times in the twenty-first century when we are fighting with the deadly Coronavirus, the total number of COVID 19 positive cases and death caused by the pandemic are going up every day in India, the Indian economy is in recession and Media & Advertising Industry has just seen a huge drop of 65% in advertising revenue in Q2 of 2020 (Source: Pitch Madison Advertising Report 2020 Midyear Review). What a time for TRAI to press for the 12% ad cap on Television by pushing for a hearing of the case at the Delhi High Court!

Dust has not yet settled on NTO 2.0. Indian TV Industry and the Regulating body have been discussing the possible implications of implementation of NTO2.0 over the last few months. It has come as a rude shock to the TV industry that TRAI has pushed the Delhi High Court for an early hearing of the case on 12 min cap per hour on television advertising. The final hearing has now been fixed on 28th September, 2020. If Indian television industry is forced to accept the 12% ad cap during this difficult time, then many TV channels, particularly the free to air channels and news channels may be forced to close their business.

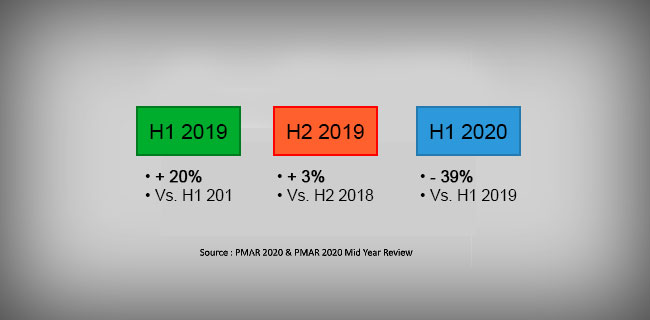

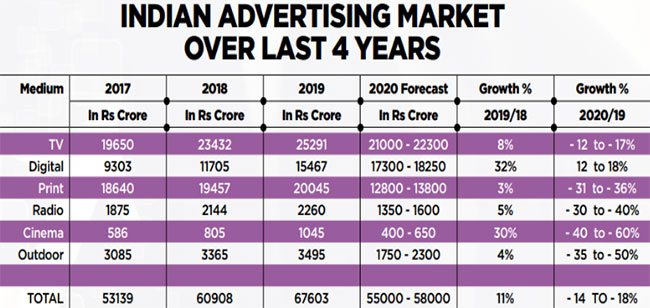

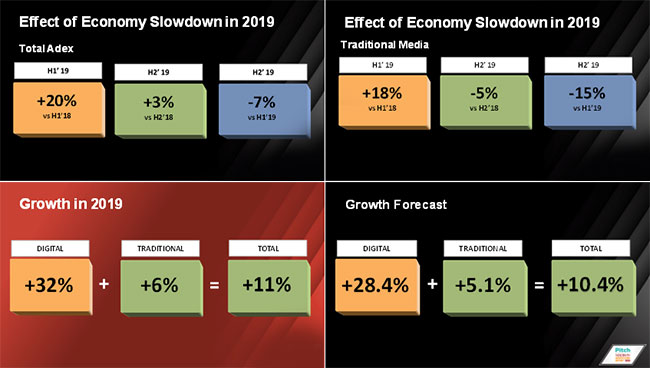

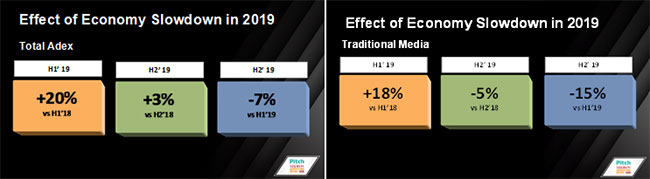

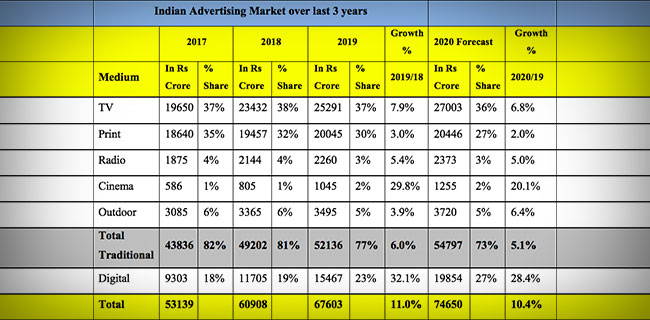

Let us take a quick look at the effect of the pandemic on TV advertising. The Pitch Madison Advertising Report 2020 Midyear Review released last week has shown that against a 65% loss of total advertising in Q2 2020, loss of TV advertising was 61%. The chart below shows the TV advertising market in April, May, June TV advertising revenue over last 3 years. Across all categories, advertisers have spent less on TV during the first half of the year with 25% of the regular advertisers not spending on TV advertising. Even after the boosting of as spend in the second half of the year due to the festive season, IPL, big ticket properties on TV like Big Boss, KFC, the TV industry is expected to end the year 2020 with 12% to 17% de-growth.

Based on consumer complaints in 2012, the TRAI first announced the regulation on 12% Ad cap in 2013. I wrote an article on 12th October, 2015 here comparing the systems of regulations on TV advertising across various countries (https://www.mxmindia.com/2015/10/mediasense-by-indrani-sen-to-cap-it-all/) and requesting TRAI to look beyond the regulatory system of UK to other countries across the world. Since 2015, some of the countries cited as example in my article, have changed their own regulatory frame works and have made it more user friendly for the TV channels. For example in Europe instead of 20% of advertising in every hour, it has been relaxed to overall 20% advertising between 7.00 to 23.00 hours with broadcasters’ own promotions, sponsors’ announcements and product placements not counting under the 20% stipulated time.

As per the last FICCI EY report we had 918 TV channels in 2019 of which 65% were free to air channels. Out of the registered TV channels in India 386 (42%) are news channels of which many are in the FTA category. These channels depend solely on advertising revenue and will be really badly hit if the 12% ad cap per hour is imposed at this unprecedented time. The eco system of Doordarshan’s Free Dish will also be affected in the process and the viewers will end up getting a raw deal in terms of the channels available on the Free Dish.

It is obvious that it is not possible to attract advertising for the repeat shows after 12 midnight till 6am in the morning when the country goes to sleep. Many TV channels have already petitioned for changing the ad cap per hour to an overall ad cap per day. By relaxing the 12 min per hour cap to 12 minute overall cap during 24 hours, TRAI can allow the TV channels the flexibility to distribute the total commercial time of 288 minute per day in a more profitable manner. Alternatively, TRAI’s purpose of providing better content to the consumers would be self defeating as consumers will get less variety of content with many FTA channels going off the air or will have to pay additional cost for viewing better content with more established GEC channels introducing more ‘pay & view’ content.

Finally, there is a time for taking all actions. If a right action is taken at a wrong time, then it can become a wrong action. After procrastination of 7 years, TRAI can surely wait for normalcy to return to our economy at large and the media and advertising industry in particular before enforcing the proposed ad cap on TV advertising.