KPMG India and Eros Now launched the report, ‘Unravelling the digital video consumer: Looking through the viewer lens’, to check the consumption habits of Indian OTT viewers and their content preferences, across 16 Indian cities.

Said Girish Menon, Partner and Head Media & Entertainment, KPMG in India,: “The online video consumer in India has evolved in a significant way in the last couple of years. With consumption now going mass and viewers spending close to 8.5 hours a week on online video, we see a homogenous pattern of consumption emerging cutting across age groups, income levels and professions. Our report also touches upon the future of this consumption evolution, and how online video could potentially disrupt traditional distribution in the coming years. This represents a large opportunity for platforms to tap into the ever expanding universe of digitally connected Indians.”

Added Rishika Lulla Singh, Chief Executive Officer, Eros Digital: “India is one of the fastest growing entertainment and media market globally and is expected to keep that momentum. As data and digital infrastructure has become exceedingly accessible even in small cities of India, the market for OTT has widened enormously. At Eros Now, we strive to constantly engage the existing consumers and expand our reach by offering new and innovative services.”

Key insights from the Indian online video consumer-survey include:

:: The Indian OTT viewer spends more approximately 70 mins/day on online video platforms, with a consumption frequency of 12.5 times a week i.e. more than once a day. Viewers are also accessing ~2.5 platforms at a given time. While the customer sets are fairly heterogeneous, there is a trend of homogeneity that was observed in terms of consumption frequency and duration across age groups, income levels and genders.

:: Indians continue to love their movies and movie related content; 30% of the respondents prefer watching movies on OTT platforms.

:: Original content is fast emerging as an important category, with close to 10 per cent respondents alluding to preference for the same. This is significant given the limited supply on original content on platforms at present, as compared to library content.

:: Long-form content is gaining traction, while short form content continues to remain relevant, especially to cater to the millennial audience.

:: 30 per cent of the respondents prefer watching content in languages other than Hindi and English. The preference for content consumption is significant in the native languages across large parts of the country, with south India observed to be the most loyal to their native tongue.

:: 87 per cent of the respondents consumed content on their mobile phones, with nearly 28 per cent of the respondents consuming content during the traditional office hours of 10 – 6pm. Online video in India is truly an ‘Anywhere Anytime’ phenomenon.

:: Three out of 10 users are watching online video on telco platforms, outlining the importance of the medium in terms of distribution. Integrated telco billing is one of the factors that is likely to help drive VOD subscriptions in the future

:: Freshness and uniqueness of content the key determining factors for installation and uninstallation of apps, as well as respondents subscribing to platforms; 87 per cent of the respondents install an app considering the quality of content

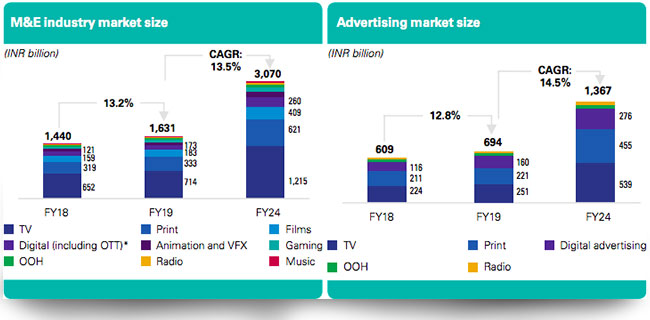

The M&E industry in India posted a solid growth of 13 per cent during FY19 to reach a size of INR 1631 billion with a CAGR of 11.5 per cent over FY15-FY19. KPMG India launched the 11th edition of its Media and Entertainment (M&E) report titled ‘India’s Digital Future: Mass of Niches’. Digital has been a recurring theme across all segments of M&E causing disruption in TV and print and fueling growth in digital advertising and gaming. The digital market is poised to become the second largest segment in India after TV, and also attract the maximum advertising spend by FY22.

The report examines the evolution of India’s digital demography to 2030. It also covers the industry’s performance across segments, along with the key underlying themes and growth drivers.

The study notes that there are favourable factors for both digital access (smartphone penetration and low data costs) and content supply (investments in original and regional digital content), which together will continue to drive up online consumption. The investments in regional content is an outcome of the growing importance of regional language markets in India, which is another key theme of the report this year. With the digital migration of English-speaking audiences almost complete, most new users coming online – and there are expected to be 500mn of them by 2030 – will access the internet in a local language.

The 500mn new users by 2030 present digital businesses with an unparalleled market opportunity but not without some complexity. Segmentation will become important as the market evolves into a mass of niches. The report examines major consumer archetypes that together provide a framework to better understand the socio-economic profile as well as media and entertainment consumption patterns and preferences of the projected billion internet users.

Said Girish Menon, Partner & Head Media & Entertainment, KPMG in India: “The theme of the report this year is India’s digital future – and although the term ‘digital revolution’ has become somewhat of a cliché, there can be no other way to explain the extent of digital integration in our lives today. With no major constraining factors, digital is expected to be a dominant force going forward and in FY23, it is likely to be the second largest segment after TV and attract the highest marketing spend among all media formats. In 2019, as digital behaviour evolves, there seems to be a growing consensus that in the future, subscription models will have a greater role in monetisation of digital platforms. Further, evolving technologies are also presenting opportunities for companies in the media and entertainment industry to achieve greater operational efficiencies.”

Added Menon: “In the coming years, it will be hard to ignore the pessimistic signals emerging from global economies but they will not have long term impacts on the industry and are unlikely to alter the strong fundamentals and momentum of M&E consumption, especially digital, in India. As an industry, we will remain upbeat on the prospects for both.”

Said Satya Easwaran, Partner & Head Technology, Media and Telecom, KPMG in India: “By 2030, we estimate that there will be a billion people in India who are connected to the internet. Our initial hypothesis is that the user will primarily be a non-English speaking, mobile phone user, from a developed rural area/ non-metro urban setting who is increasingly willing to pay for content online. But why is the profile of India’s digital demography relevant? The digital disruption has forced a pivot of business models in media and entertainment from an erstwhile B2B2C model to a D2C one. And therefore, segmentation and demographic, psychographic and behavioral profiling will all become increasingly important, as they have historically been in other consumer businesses.”

KPMG International has launched the second edition of ‘Me, my life, my wallet’, that continues its exploration of the multidimensional customer — what’s truly driving behaviour and choices — and how this is set to change as the customer of tomorrow emerges. This year’s edition is based on ethnographic interviews and an online survey, conducted during 2018, by GLG and Foresight Factory on behalf of KPMG International. The survey included nearly 25,000 consumers across Brazil, Canada, China, France, India, the UAE, the UK and the US.

The research explores six key themes of critical importance to organizations and institutions around the world, namely; trust, data, wealth and retirement, generational surfing, the customer of the future and the B2B customer. It also provides an in-depth look at STEP (Social, Technological, Economic and Political) events influencing consumers and highlights emerging patterns of behaviour around the world.

“The Indian consumer is difficult to understand, and as the online revolution progresses beyond the big cities and starts gaining momentum in the country’s heartland, they are getting more complicated still. The rewards for companies who take time to learn, though, are substantial,â€Â noted Arun M Kumar, Chairman and CEO, KPMG in India.

A few interesting highlights for India include:

:: India, consumers trust technology companies (75 per cent), wealth management companies (62per cent), power & utility firms (62per cent), banking (75per cent) the most. The least trusted entity is the government at 51per cent, a high figure compared to the global average (37per cent).

:: 87per cent would trade their personal data to a company for:

o better customer experience and personalization – 26per cent

o better products and services – 24per cent

o better security – 21per cent

:: 58per cent will most likely view brands on social media that “offer deals or discountsâ€

:: 55per cent would rather lose their wallet than their phone

:: Globally, 66per cent of consumers are interested or very interested in technology – this leaps in the fast-growing economies of China (81per cent), and India (83per cent)

:: Globally, 38per cent of consumers are anxious about unauthorized tracking of their online habits by companies, governments, and criminals; 47per cent in India

:: Globally, 51per cent of consumers are anxious about identity theft; 52per cent in India

:: Globally, almost a quarter (24 per cent) of consumers say they would not trade their data, this falls to 13per cent in India

:: Consumers in India are more trusting with their data than consumers in other markets. Globally, 37per cent of consumers don’t trust anyone with their social media data, in India 13per cent. Globally, 31per cent of consumers don’t trust anyone with their mobile data, in India 10per cent.

Added Harsha Razdan, Partner and Head, Consumer Markets, KPMG India: “Consumers are anxious, with younger generations feeling it the most. They like new technology but are concerned about handing over personal data, and what that could mean for their privacy and security. Our research demonstrates that organizations should be aware of the heightened awareness people have about the value of their data; they want to feel that they are in control at every stage of the business relationship. Many companies haven’t yet fully grasped the concerns consumers have about sharing their data, or how this could affect consumer loyalty. Yet more and more businesses are looking to monetize the data they hold – whether that’s what we put in our shopping basket, how many times a week we exercise, or what we choose to watch. Consumers are more aware of the value of their data, and businesses need to be responding to this new, tech-driven, data-savvy type of customer.â€

In a show of strength, captains of the print media and members of the advertising and marketing sectors have got together to evangelise the print media.

Their view: Yes, television exists and digital is growing rapidly, but print is growing fast too.

Gathered in a central Mumbai hotel, under the aegis of the Audiot Bureau of Circulations, a near-70-year-old organisation that certifies circulation figures of member publications twice a year. The trend of certified circulation figures by ABC show that the print medium (member publications of ABC) is thriving, growing and expanding in India inspite of stiff competition from all other mediums namely, Television, Radio and Digital, notes the ABC.

As on date, ABC certifies 910 Daily and Weekly Newspapers, 57 Magazines and Annuals. Other members of the ABC include media and ad agencies, print media advertisers, government organisations and the DAVP. The total number of ABC members is 967.

Few reasons why print publications are growing in circulation:-

:: Impact of education – Growth in literacy and education have created substantial

headroom for growth of newspapers.

:: Advantage of India’s Economic growth – It is believed that the growth of newspapers in India is directly related to urbanisation leading to higher aspirations, heightened interest in buying assets etc.

:: Reading newspaper a part of daily routine combines well with ease of reading at your own time.

:: Easily accessible and available at home – newspapers are home delivered in India, unlike in the West

:: Competitive pricing – newspapers are the cheapest source of news.

::Customised sections and pull outs cater to various segments of readers together

with localized content.

:: Power of the written word – Newspapers have continued their strong traditions over the years to provide accurate and reliable news to their readers.

As compared to the world print market, India is one of the brightest spots in the print media: India one of the few countries where print advertising revenue is growing,India’s paid-for daily circulation is growing whilst most other countries are declining, Number of paid-for titles in India highest in the world and growing while number of titles in other countries declining

Print is growing at an incredible 4.87% increase in CAGR over a 10-year period. As many as 2.37 crore copies were added in the last 10 years accompanied by an increase of 251 publishing centres. Largely regional language newspapers have contributed to the growth, we were informed.

Leading the presentation made by ABC was Shashi Sinha, CEO, IPG Mediabrands, India. While highlighting the above along with Girish Agarwal, Director, Dainik Bhaskar group, he quoted KPMG India figures to show that in terms of advertising revenues, print is thriving (see table above).

For the past few years we have hearing that ‘Digital has arrived’. That ‘Digital is the future’ etc. But how has it arrived and more importantly how will it be our future? So, on Wednesday (July 27) some top executives from the India’s motion picture and digital industries concluded that accessibility, affordability, quality content and online content protection will be the key drivers to sustain growth in India’s digital economy.‘Fast Track India: Bolstering Growth in the Digital Content Economy’, a knowledge series forum by the Federation of Indian Chambers of Commerce (FICCI) in association with the Los Angeles India Film Council (LAIFC), assessed the extent to which screen content acts as a key driver of the digital economy in India. The industry experts assessed the current regulatory and infrastructural challenges, reviewed future growth trends and underlined innovative ways of monetising digital content to stimulate growth in India’s digital economy.

Noted filmmaker and Co-Chairman, FICCI, Entertainment division, Ramesh Sippy started the conference by highlighting the fact that increased connectivity, technological innovation and new content delivery platforms all combine to increase growth. He said that government’s role is pivotal to enabling legitimate content delivery platforms to protect and monetise their content in order to achieve their full potential in a rapid changing marketplace. Digital India has the potential to create opportunities for businesses, promote innovation and create jobs. However online content theft, varying levels of broadband access and affordability in terms of data tariffs continue to present challenges for providers to deliver value to consumers. These factors will have a significant impact on how digital media evolves in the future.

Girish Menon, Director, Transaction Services, KPMG India moderated as well as introduced the first panel discussion. The first panel ‘Making Sense of the Economics of Digital Media’ featured a keynote presentation by KPMG. Menon said, “The advent of the OTT services and on-the-go content aided with competitive tariffs and falling average retail price of smartphones has helped to drive video consumption in India. However, profitability still continues to be a major challenge coupled with infrastructure and affordability of data tariffs and payments models. It is imperative for the OTT players to address these concerns through innovative means to achieve the medium’s full potential.†Speaking about the future of OTT content services, Ajay Chacko Co-Founder and CEO, Arre said, “As in the case of broadcast TV in India, the relatively infant digital content economy is showing signs of secular, organic growth driven by an increasingly young India. We already have more than 120 million consumers of digital content. As with every paradigm shift, audience shifts will be followed by a shift in advertiser preferences and finally consumer monetisation. So I am quite hopeful that the digital content economy will see the exponential growth that has been witnessed in the 2000-2010 decade in TV, in the next three to five years.†While film producer Vishesh Bhatt, expressed his concern about serious content makers still not understanding the digital ecosystem. However, Karan Bedi, COO, Eros Digital, was optimistic about the future and gave the example of Pokemon Go, about how the game has caught the attention of the consumers. He said: if consumers are compelled by content, they will eventually pay for subscription as well. Said Archana Anand, Business Head, dittoTV: “In light of the accelerated digital media consumption across the country, it is wonderful that FICCI and the LA India Film Council provides this much needed platform to discuss the market potential of this space and the innovations and challenges thereof.â€

Moving on from the concerns about monetising digital content, the other looming concern is around the rules and regulations of the digital media. The second panel discussion on ‘Regulatory and Infrastructural Challenges for Digital Media’, Abhishek Joshi, Head, Marketing and Analytics, Digital Business, Sony Pictures Networks India Pvt Ltd. said “The OTT industry has graduated from the innovators stage to the early adopters stage within the innovation diffusion curve, based on distinguished product strategies by players in the market. However to cross the chasm to gain the majority market, policy makers will have to play a very big role. Infrastructure and regulatory policies are going to be the biggest differentiators for industry growth for the next 18 months.†Akash Banerji, Head, Marketing and Partnerships, VOOT was very hopeful about the future. According to him, even though the industry is still learning, the consumers will be in a demanding position in the future and eventually mobile data will also come down. Siddharth Roy, COO, Hungama.com, stressed on the fact that branded IP (Intellectual Property) will be one of the key drivers of content regulation. But Rajeshree Naik, Co-founder, Ping Networks, had other concerns. She said that it is the collective responsibility of the industry is to see to it that government stays out of digital media regulations. This session was moderated by journalist and author Mayank Shekhar.

The final panel discussion was on ‘Building a Robust Enforcement Model to Protect Content In a Digital Economy’ and was moderated by Uday Singh, Managing Director, Motion Pictures Association, India Office. Oliver Walsh, Regional Director, Online Content Protection, Motion Picture Association- International(MPA-I) said, “The Indian film and TV industry supports 1.8 million jobs which are at risk because of rising online content theft. The future of legitimate content delivery platforms depends on effective enforcement measures supported by Indian State Governments. The Telangana Intellectual Property Crime Unit (TIPCU) is a great example of a dedicated law enforcement unit to tackle organised online film piracy and will set a gold standard approach to significantly reduce online infringement of films and television shows. I hope it is the first of many such enforcement units across India.†Rajkumar Akella, Honorary Chairman, Governing Council, Anti Video Piracy Cell, Telugu Film Chamber of Commerce said, “As we have been witnessing in recent days, the problem of online piracy is most urgent. The greatest threat now has become the pre – movie release leakages. Without real time interventions from the government and industry, it will go out of control. In this scenario, the latest initiative – TIPCU by the Government of Telangana, the Telugu Film Industry & the Motion Picture Association, India office, is a very significant step in tackling Movie Piracy, particularly Online Piracy. It is a collaborative, dynamic model,where the Government works seamlessly with the Industry and all stakeholders. The unit will be making optimum use of Technology besides policy, enforcement and outreach. This is a step in the right direction to root out piracy in India.†The General Counsel of Viacom 18, Sujeet Jain suggested the formation of digital courts to deal with piracy and protect online content. Anupam Sharma, Director, Film and Casting Temple, Australia was of the opinion that educating the consumers was the first step in stopping illegal downloading of content. He showcased a short video where the cast and crew of his movie are shown to be thanking the audience for not watching pirated videos and acknowledging the fact that the audiences are also a part of the film industry. This video was made to create awareness against video piracy.

Biren Ghose, Country Head, Technicolor India, in his concluding remarks, said, “Content is assuming new life in the emerging digital economy. Technology enables innovations in imagery that could hitherto neither be produced nor consumed. FICCI and LA India Film Council need to be complimented on encouraging the conversation for the Indian agenda in this space.†Panelists concluded that a combination of government and private initiatives would need to be rolled out to achieve the ambitious goal of a truly Digital India.

Snapdeal released a first-of-its-kind study in partnership with KPMG titled ‘Impact of Ecommerce on SMEs in India’. The study examines the macro-impact of e-commerce sector on growth of SMEs in India and identifies remaining gaps in the eco system needed to be plugged to facilitate adoption of e-commerce by SMEs.

The report compares the e-commerce led growth trajectory of SMEs in India vis-Ã -vis other emerging and developed economies. Additionally, it outlines different roles that various participants like the government, industry bodies and ecommerce companies themselves can play in making the SME ecosystem more robust.

Speaking at the release of the report, Kunal Bahl, Co-founder and CEO, Snapdeal said, “At Snapdeal, we are working towards building the most impactful digital commerce ecosystem in the country and SMEs form the foundation of this ecosystem in many ways. With over 200,000 sellers operating on our platform, we felt the need to conduct a systematic unbiased study to identify opportunities and challenges to further accelerate the growth of the sector. We have taken a number of initiatives like seller training programs, seller financing program- Capital Assist and Snapdeal Seller Advisor Program, with an aim of creating life changing experiences for over one million sellers in the next three years. This study has given us deeper insights into what more we can do to enable small businesses become more successful online.â€

Richard Rekhy, CEO, KPMG India said, “The fast paced growth of the e-commerce industry in India represents an unprecedented opportunity for SMEs. We hope that the findings of this report will assist policymakers, industry bodies and e-commerce companies to strengthen the support ecosystem, which enables SMEs to ride the e-commerce growth wave successfully.â€

This report is the first in a series of initiatives that Snapdeal has undertaken for creating an ecosystem for MSMEs and leveraging ecommerce for their growth.

L to R: Jehil Thakkar (KPMG), DD Purkayastha (ABP), Ravi Dhariwal (BCCL, INMA) and Santosh Desai (Future Brands)

By A Correspondent

The second day of the International Newspapers Marketers Association (INMA) South Asia 2012 conference in Delhi threw light on the complexities and challenges of the print newspaper media. The first session of the day was ‘Media 2020: A future backward kaleidoscope’. The session focussed on how the newspaper industry is readying itself to face the challenge from digital media usage.

Mr Jehil Thakkar, Partner, Head-Media & Entertainment, KPMG India made some interesting observations about the levers that are changing the Indian newspaper industry. He pointed out how empirical studies prove that there exists a positive relationship between the wealth of a nation and newspaper readership: “There also exists positive correlation between growth of economies and technology adoption, which has significant potential to disrupt media consumption.”

“The rapid proliferation of new-age devices and growth of alternate media has reduced newspaper consumption by 40 per cent with audiences preferring to access paper via their mobile phones,” added Mr Thakkar. According to him, technology would alter the workings of newspaper industry as coverage would become electronic, delivery would become faster; collaboration would become the key; cloud-based service would become a norm; interactivity through QR and barcodes would see an upsurge.

DD Purkayastha

If you are having trouble in viewing this video, see link

Talking of how things will shape up in 2020, DD Purkayastha, MD & CEO, ABP Pvt Ltd said that the future belongs to newspapers who become hyperlocal as cities reach the saturation point. He said: “Regional publications will grow. And consolidation will happen at a much faster pace.”

Mr Ravi Dhariwal, President, INMA Worldwide and CEO, The Times of India, noted how newspaper of 2020 will undergo a dramatic change. He noted: “Three critical things will emerge in 2020: what brand you own will become important as there will be many more brands on the digital media; curation of the product will become more important as the role of a journalist will shrink and need for analytical news pieces will arise; and business model will change as ad revenue will become a critical source of revenue. As technology improves, and people get more comfortable with using technology, the ad rates would only increase.”

Mr Santosh Desai, MD & CEO, Future Brands India, remarked: “The larger issue that would emerge would be the tension between decentralisation of news media and fragmentation.” The panel, however, coherently agreed that despite the changes and challenges that the newspaper would undergo, it would still exist with the digital media.

The session on ‘Increased circulation; dwindling readership: Is it time to measure ‘access’?’ saw panellists discuss the much-debated measurement metrics available. ‘Newspaper distribution channel: How best to nurture it for the future’ and threw light on the vendors and agents who distribute the newspapers. Moderating the session, Mr Sanjeev Vohra, Executive Vice-President – Audiences, BCCL, said: “The vendor currently exists as an independent businessman and as an investor in newspaper business.” His view was supported by Mr PS Venkat, Vice-President, Circulation, The Hindu, who said that changes are needed in distribution model to enable the vendors to become partners in progress.

Mateen Khan

If you are having trouble in viewing this video, see link

Mr Mateen Khan, Product Head of Lokmat Samachar pointed out how the distribution channel in rural areas is still a problem, while it may not seem so in a metro. Taking the discussion ahead, Mr Rakesh Sharma, CEO, Aaj Samaj & ITV Group said: “There should be distribution points every three kilometres, and more distribution points.” He, however, noted that the vendors will remain the key to distribute newspapers in India beyond 2020. Mr OP Rajgharia, Chairman & MD, Overnite Express Ltd appreciated the effort put in by newspaper vendors to ensure the timeliness of delivery.

‘Needed to be sector-neutral’

If you are having trouble in viewing this video, see link

Bhaskar Das, President & Principal Secretary to MD, The Times of India Group, talks to MxMIndia on curating the INMAÂ South Asia 2012 conference

When I was talking to the organisers, and was given the task of preparing the content architecture of INMA, I told them very clearly that it is not about newspaper industry -it is about business. So, we have to be sector-neutral since principles of business are same. Newspaper is a sub-set of business. This was the first consideration.

Secondly, in my case, the delegates were my guiding point. Why should people attend the conference? Are we going to be just another conference? How do I make it distinctive?

The distinctiveness of the conference is that it creates fluid knowledge; knowledge that one can import when they go back. So, I had to ensure that they learn from each session. That led to the subject. In most of the conferences, people state the obvious. I thought why we don’t address the fact that there are complexities, there are challenges. Being an incumbent player, I realised that if we talk about problems, it is not solved. We should then talk about how we can leverage that problem or challenge. This led me to look for various industries. I scouted the internet, books, academic journals, about what happens when an industry goes through huge challenges, air pockets. There are initial signs of a problem, which I came to know of while researching, such as ‘butterfly effect’ that led to complexity science. This became the theme. The theme has to be intriguing to people rather than being a newspaper conference. The theme was then decided as ‘complexity advantage’. Now that complexity is a given, why not leverage it.

On the audience mix:

This time it has been a record attendance. I am not very happy but you to also have to market it that way. If one can maintain this level of content architecture, attendance will grow. For an event that happens once a year, I will have to sustain noise throughout the year. The community needs to talk about it, so that you can have user-generated content architecture next time. Then, there are regional peculiarities that may not be only one; there are eastern and western peculiarities.

We also have to be industry- or sector-neutral in our audience mix. Why should they be from newspaper industry? Why not from television industry or from client side to discuss business? When people know what you are delivering, I am sure diversity will happen in the audience.

The session was followed by speakers from Pakistan and Bangladesh who spoke on ‘Managing complexity in South-Asian markets – A Pakistan and Bangladesh Experience.’ The session saw interesting insights about newspaper industry in the two neighbouring countries.

Industries across the globe are increasingly learning from other industries to improve their operating efficiencies and innovation capabilities across various spectrum of businesses. ‘Media learning from other industries’ saw three specialists from sectors such as retail, telecom and finance discuss the wisdom that newspaper industry could imbibe, given the onslaught of digital media. The panel discussed how the evolution could gain from the exploration of the new path.

Mr Jaideep Ghosh, Partner, Management Consulting, KPMG pointed out that print media continues to remain the second largest medium in the Indian media and entertainment industry. He also pointed out the key challenges of talent, operational cost, monetizing digital media and fragmentation that the industry faces currently. He said: “Media can leverage data analytics to strengthen the understanding of its customers and build brand loyalty, much like the way telecom, retail and finance sector have done.”

Drawing from the e-retail experience, Mr Rajiv Prakash, ex-CEO, FutureBazaar.com, said, “The audience is increasingly turning Clomosol, which is an aggregation of Cloud+Mobile+Social+Local. Thus, the digital consumer is a channel omnivore, and should be serviced at every touch-point.”

Mr Jairam Sridharan, Head, Retail Banking, Axis Bank said that the newspaper organisations should focus on getting their product on mobile, rather than internet as, “the consumer is leapfrogging the internet and becoming increasingly mobile-savvy.”

The closing session of the two-day INMA conference saw Prof Rishikesha T Krishnan., Chairperson, Corporate Strategy and Policy Area, IIM Bangalore talking about sustainable and thriving media business model that can successfully withstand the vicissitudes of business environment.

He said, “The internet tends to dampen bargaining power of newspaper channels by providing direct avenues of access to customers. But the other hand, it will help the industry to create new substitutes, and new geographical markets will emerge.” He further noted, “The internet has and would result in targeted advertisements, disappearing role of editor as decision maker; fall in advertising revenues and young people moving away from printed newspaper.” The key decision variables, according to him, were how to embrace internet, and change strategy. Giving the example of Schibsted, Norway, he said that the paper now brings readers to its webpage through the front page and even Google was denied the permission to crawl its pages. “This helped them to monetise the banner ad on its front page,” Mr Krishnan said, adding, “Huffington Post has enaged in user-generated content, and its ad revenues are growing. Axel Springer/Bild has extended its brand to other media.”

As Indian newspaper industry struggles with low cover price, growth of paid news, entry of non-traditional players, investment to establish presence in non-metros, the panel at INMA South Asia conference tried to address issues as closely as possible. Whether the industry would learn, and implement the learning remains to be seen.

Snapdeal released a first-of-its-kind study in partnership with KPMG titled ‘Impact of Ecommerce on SMEs in India’. The study examines the macro-impact of e-commerce sector on growth of SMEs in India and identifies remaining gaps in the eco system needed to be plugged to facilitate adoption of e-commerce by SMEs.

Snapdeal released a first-of-its-kind study in partnership with KPMG titled ‘Impact of Ecommerce on SMEs in India’. The study examines the macro-impact of e-commerce sector on growth of SMEs in India and identifies remaining gaps in the eco system needed to be plugged to facilitate adoption of e-commerce by SMEs.