Boston Consulting Group (BCG) and Confederation of Indian Industry (CII) have unveiled a report, ‘Lights, Camera, Action…and the Show Goes On’. The report seeks to evaluate the impact of 2020 on the Media and Entertainment industry and highlights key imperatives for increasing the industry’s resilience in the face of adversity. Said K Madhavan, Chairman, CII National Committee on Media & Entertainment and Managing Director, Star & Disney India: “The pandemic outbreak created many unique challenges to the Media & Entertainment sector. It was commendable to see the entire industry rise to the occasion to engage and entertain millions of viewers while they were confined at home. It’s the sheer willpower and persistence showcased by the stakeholders that have helped convert adversities into opportunities.”

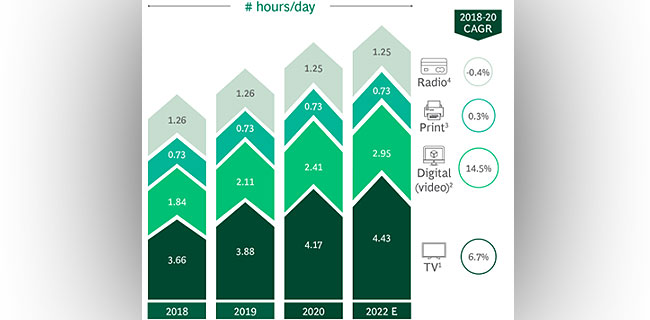

According to the report, 2020 has seen a massive surge in TV and smartphone video viewership during the weeks of lockdown and beyond as people spent more time at home, and OTT witnessed its presence increase in Tier 2-4 cities due to the high quality, original, and local content marketed using free trials. Covid-19 has had a major impact on how we consume content, both in-home and outside and some of these will have long term implications for the industry. Added Mandeep Kohli, Partner, Boston Consulting Group India: “India continues its unique multimodal growth. TV consumption surged ~40% during lockdown due to an increase in non-prime time viewing. Smartphone video consumption is up as well, with a 50-60% increase in subscribers over last year. Going forward we expect the digital trend to intensify, OTT adoption to continue rising, and the emergence of new business models better suited to the new reality. The share of digital in advertising will also continue to grow, having reached 15% in 2020, a full 2 years before its pre-Covid forecast.”

Said Kanchan Samtani, Managing Director & Partner, Boston Consulting Group India: “Recent developments such as the resumption of operations and recovery of ad campaigns has resulted in optimism in the industry” explains

One of the major themes in this year’s report is the potential economic impact that the Media & Entertainment industry can create. This is especially important in the context of the ambitious GDP target of $5 trillion that has been set by the government. The report demonstrates how in economies such as South Korea, the Media & Entertainment industry form a large and growing part of GDP due to concerted efforts by stakeholders to take Korean culture global. The report also highlights opportunities in attractive parts of the value chain such as Visual Effects and Animation, and also calls out imperatives that will need to be acted upon to seize these opportunities. “Countries are developing media hubs to drive impact of M&E – Spain has setup a content city in Madrid to tap into the growing global demand for Spanish content. This gives a boost not only to the M&E industry but also to the tourism and India should aspire to do the same. Continued focus on customer value, increasing our presence in areas such as VFX and animation, and concerted investment in skilling and technology can lay the groundwork needed to help Indian M&E achieve greater heights,” said Samtani.