By Indrani Sen

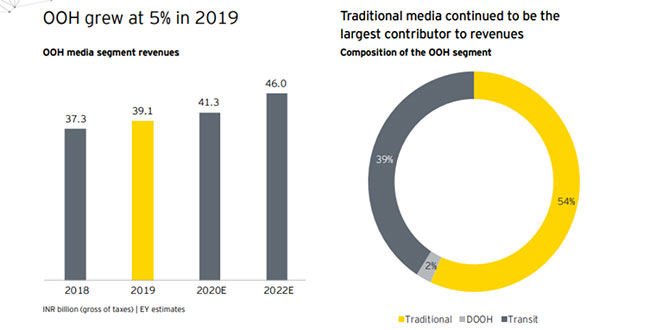

The EY-FICCI 2019 Media & Entertainment Industry Report estimated that the Indian OOH industry grew by 5% in 2019, taking the industry size to Rs 37.1 billion. The traditional OOH formats, driven by increased advertising opportunities in tier-II and tier-III cities, contributed 54% to the overall revenue. However, according to the report the main driving factor behind the growth is recent development of infrastructure network, including upcoming airports, smart city projects, malls, metros, bus shelters, public utility, coffee shops, etc.

The EY-FICCI 2019 Media & Entertainment Industry Report estimated that the Indian OOH industry grew by 5% in 2019, taking the industry size to Rs 37.1 billion. The traditional OOH formats, driven by increased advertising opportunities in tier-II and tier-III cities, contributed 54% to the overall revenue. However, according to the report the main driving factor behind the growth is recent development of infrastructure network, including upcoming airports, smart city projects, malls, metros, bus shelters, public utility, coffee shops, etc.

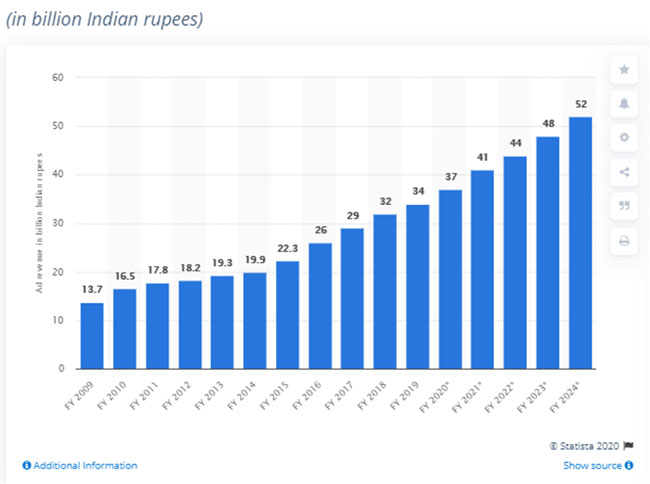

A couple of years back, www.statistia.com published an estimate of out of home advertsing in India from 2009 to 2024 as shown below. It is interesting to note that overall size of OOH industry estimated In the FICCI EY report is higher than shown in the chart for 2019 (Rs. 34 billion).

The growth of the OOH industry has been stalled completely as an effect of Covid-19. In the ‘FICCI Frames 2020’ virtual conference, WPP’s CEO Mark Reed remarked that OOH was the most impacted medium due to Covid-19. While we are seeing some signs of revival in digital, TV and print media, the trend has not yet been seen in OOH media under the gradual process of unlocking. While we are still waiting for FICCI EY to release a revised estimate for M&E industry in 2020, the mid-year review of the Pitch Madison Advertising Report 2020 has estimated 35% to 50% de-growth in OOH advertising revenue in 2020.

At the early stage of lockdown, IOAA also estimated that their annual revenue may see a 50% drop in 2020 and appealed for financial relief to the various state governments who have not yet responded positively. The association also requested the central government to declare the pandemic as natural calamity which is covered under ‘force majeure’ clause of all OOH contracts which also has not received any definite response. In US and couple of other countries, OOH industry registered as small business has received some financial relief, but we have not seen any such relief measures for the OOH industry in India.

An article published on August 10, 2020 has predicted four key trends for OOH medium in 2020 and beyond (https://www.advendio.com/4-key-ooh-advertising-trends-2020-beyond): 1/ build brand awareness with smart creatives; 2/ adapt value for money messaging approach; 3/ the evolution of touch screen OOH advertisements and 4/ curbside pickup and digital OOH are here to stay. Apart from the first trend, there is hardly any scope seeing of the other trends happening in India. It is high time that our outdoor advertising agencies take stock of their inventories and consider disinvesting in traditional formats and channelize their attention to building up standardised digital OOH formats as per the global trends.