By Indrani Sen

Covid-19 has transformed the media consumption trends in India. Globally, streaming platforms gained in a big way since the pandemic struck and India is no exception. The report published by Dentsu Agies Network – “Now Streaming: The Indian Youth OTT Story” – is a study conducted among urban India’s Gen Z & Millennial reconfirms this trend. These trends could be reflecting behavioural changes of the two younger generations which are likely to last even after the cloud of pandemic shifts from the Indian sky. The highlights of the findings from the report are shown below:

As many as 74% of the respondents came from the Top 8 metros with 26% coming from rest of urban India. 47% of the respondents were male and 52.2% were female. 78.5% came from Gen Z (5 to 25 years) and 21.5% came from Millennials (25 to 39 years). The report therefore cannot be taken as uniform trends across urban youths across India but trends which are visible among youths residing in the top 8 metros and mostly below 25 years of age. They are, however, the future targets of marketing and advertising in India.

|

Average daily time spent in hours |

||

| Gen Z | Millennials | |

| On line Gaming | 1.97 | 1.11 |

| Binge Watching | 4.45 | 3.66 |

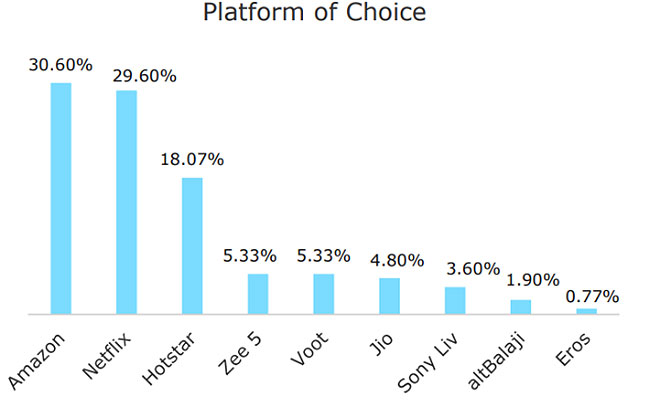

Among the various OTT platforms, Amazon Prime and Netflix lead the pack, followed by Hotstar. The other OTT platforms are yet to build up significant presence among the Indian youths. Gen Z spends more time than Millennials both on gaming and binge watching on OTT platforms.

The choice of genres by the two sections of youth explains the popularity of the top three platforms which offer more content as per their preference. Zee 5, Voot, Jio, Sony Liv, etc have less content to offer in the Comedy, Action, Thriller and Science Fiction genres. Amazon Prime, Netflix and Hotstar have also invested more in production of original content. However, the report has also shown that both in North and South India across different demographics the primary usage of OTT platforms were for viewing TV shows and movies.

During the lockdown north Indian youths invested on an average in three OTT subscriptions than their counterparts in south India who invested on an average in two OTT subscriptions. The Gen Z invested on an average in 3 OTT subscriptions while Millennials invested in 2 OTT subscriptions during the same period. The report does not give details of the demographic profile of the sample, but we can safely assume that the sample was skewed towards higher SECs as indicated by higher spends on OTT subscription by Gen Z, most of whom would not have been financially independent and had to ask their parents for the subscription money. Obviously their parents were not financially affected due to the economic slowdown during the lockdown and could afford to indulge their children. The report therefore captures mainly the trends of OTT consumption of urban youths from 5 to 25 years age belonging mostly to NCCS A and the top 8 metros.

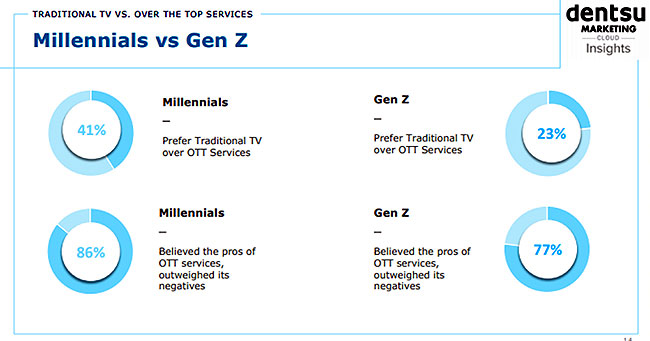

The report has also captured that 73% have no concern about the content of the OTT platforms. The other 27% have stated obscene content, anti-national content, strong and bold language of the content as well as content hurting sentiments of religion/ caste as causes of concern related to OTT platforms. On the other hand all respondents had concerns about internet connections, pop-up ads and buffering related to steaming of the contents. Both Millennials and Gen Z have shown a clear preference for OTT services and believes that the positives factors outweigh the negatives.

The report concludes that content distribution, attractive marketing, transitioning the gaming industry and personalisation are the key factors which is helping consumption of OTT platforms to dominate over consumption of traditional TV viewing. The analysis does not mention about the tie ups between OTT platforms and Telecom giants like Airtel, VI and Jio, a practice which began in 2017/ 2018 and has been continuing since then.

As per the range of packages offered by the three telecom companies, it appears the leading OTT platforms do not believe in exclusive tie ups with any single telecom company and have created a level playing field for all the service providers by having tie ups with all of them. It seems this survey did not probe into this aspect of free subscription with mobile connection among the Gen Z and Millennials, most of whom would have been enjoying some such free benefits through a single sign in. The findings of the reports outweigh the apparent skewing of the sample and a few gaps and have provided all of us a crystal globe for gazing into the future of media consumption.

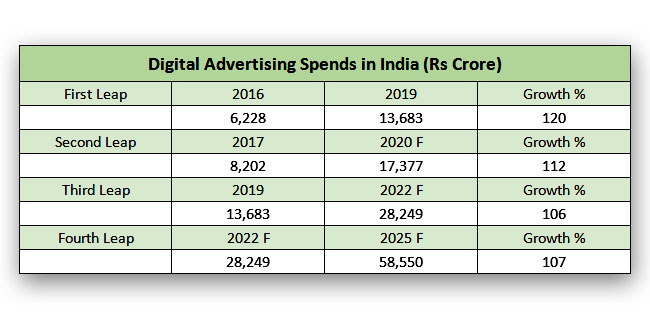

According to the DAN Digital Advertising Reports, spends on digital advertising in India is increasing by 100%+ every three years and is poised to cross the 50,000 crore milestone before 2025. It was only in the second half of the last decade, the Indian advertising industry crossed the milestone of 50,000 crores, so it seems strange that the newest and youngest competitor for the share of the advertising pie will be crossing that same milestone by middle of this decade! We have already witnessed the first giant leap from 2016 to 2019 and it seems quite possible that in three more giant leaps digital advertising will achieve this fantastic growth.

According to the DAN Digital Advertising Reports, spends on digital advertising in India is increasing by 100%+ every three years and is poised to cross the 50,000 crore milestone before 2025. It was only in the second half of the last decade, the Indian advertising industry crossed the milestone of 50,000 crores, so it seems strange that the newest and youngest competitor for the share of the advertising pie will be crossing that same milestone by middle of this decade! We have already witnessed the first giant leap from 2016 to 2019 and it seems quite possible that in three more giant leaps digital advertising will achieve this fantastic growth.

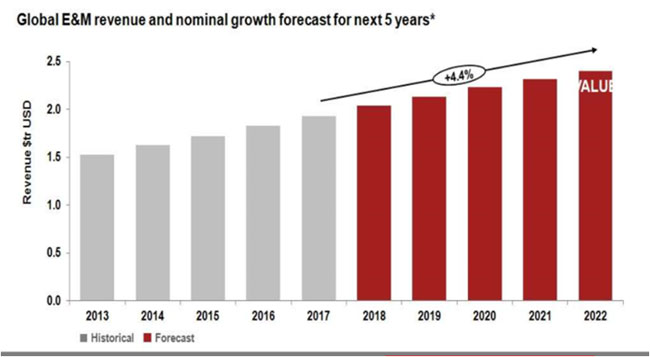

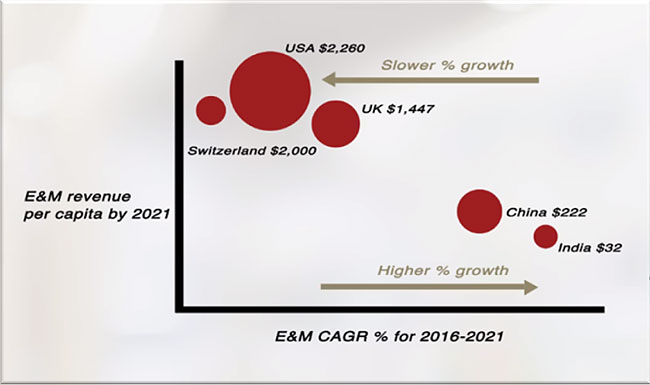

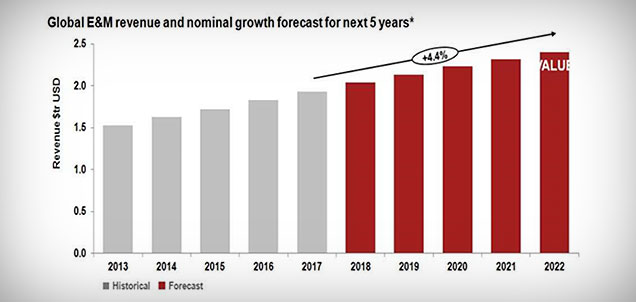

In early June, PWC released their Global Entertainment and Media Outlook 2018-2022 predicting that in India the Media and Entertainment(M&E) industry will grow at a compound annual growth rate (CAGR) of 11.6% growth of between 2018 to 2022 (https://brandequity.economictimes.indiatimes.com/news/media/indias-me-industry-to-clock-over-rs-353609-crore-by-2022-pwc-report/64477039). This growth rate will be 2.5 times the growth rate of 4.4% predicted for the global M&E industry. However, in terms of M&E revenue per capita in US$, the developed countries will be far ahead and in 2021 US M&E per capita revenue ($2260) will be 10 times of China ($222) and 70 times of India ($32).

In early June, PWC released their Global Entertainment and Media Outlook 2018-2022 predicting that in India the Media and Entertainment(M&E) industry will grow at a compound annual growth rate (CAGR) of 11.6% growth of between 2018 to 2022 (https://brandequity.economictimes.indiatimes.com/news/media/indias-me-industry-to-clock-over-rs-353609-crore-by-2022-pwc-report/64477039). This growth rate will be 2.5 times the growth rate of 4.4% predicted for the global M&E industry. However, in terms of M&E revenue per capita in US$, the developed countries will be far ahead and in 2021 US M&E per capita revenue ($2260) will be 10 times of China ($222) and 70 times of India ($32).