By Our Staff

The Confederation of Indian Industry (CII) and Boston Consulting Group (BCG) unveiled a report of the media and entertainment sector titled, ‘Blockbuster Script for the New Decade: Way Forward for Indian Media and Entertainment Industry’. The report explores the industry’s status after the impact of the Covid-19 pandemic and highlights key imperatives for achieving its potential over the next decade.

Said K Madhavan, Chairman, CII National Committee on Media & Entertainment and President, The Walt Disney Company India and Star India: “It is delightful to see that the hard work put in by all stakeholders in the face of great challenges, both professional and personal, has paid off and now our industry is back on track. Media and entertainment played a crucial role in helping the country navigate and overcome this crisis and reinforced its role in people’s lives”. The report projects that the industry is set to grow to $55-70B by 2030 at a CAGR of 9-11%, with digital video and gaming being the biggest growth drivers.

Commenting on the report, Chandrajit Banerjee, Director General, CII, added: “CII has maintained its thought-leadership in Media and Entertainment sector over the years through various measures. Industry as well as Government and policy makers value the inputs which CII initiatives add to the knowledge pool of the sector. The Big Picture report, released on the occasion of the CII Big Picture Summit every year, holds a special place in this resource ecosystem. This year’s report, once again put together by BCG with the help of CII Media and Entertainment Committee, looks at the decade ahead, will help businesses chart their growth path and aide the government in framing enabling measures to facilitate further expansion of the sector.”

Said Siddharth Roy Kapur, Co-Chairman, CII National Committee on Media & Entertainment and Founder & Managing Director, Roy Kapur Films: “Film production and film exhibition were amongst the worst affected sectors in the M&E business due to the pandemic. After a long period of shutdown, cinema halls are now back in business with a bang. A record number of big-ticket movies are lined up for release well into 2022. That augurs well for the sector but caps on occupancies, closures of cinemas and modified audience behaviour might impact the speed of recovery. On the other hand, streaming has provided new avenues for screening and broad-based the options available for producers, artistes and technicians. Along with the rise of regional cinema, this marks the start of a truly fantastic decade ahead for the Indian content business. Kudos to team CII and BCG for another enriching edition of the Big Picture report.”

Added Biren Ghose, Vice Chairman, CII National Committee on Media and Entertainment and Country Head, Technicolor India: “This year’s CII – BCG Big Picture report appropriately features the games sector in India captioned the “Future is play”. Despite sporadic regulatory hiccups, in some states, this segment is growing at around 30 per cent per annum which is the highest among the animation and visual effects (AVGC) sector. CII is confident that this report articulates the critical inputs to guide future policy thereby creating an enabling environment for industry to grow. The success of India’s media and entertainment will ultimately depend on the ability to scale world-class creative talent in order to capitalize on the global opportunity in this sector.”

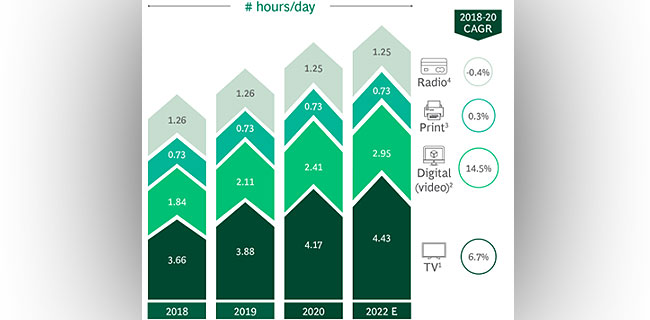

The report highlights the Media and Entertainment industry’s multimodal growth story. The Indian OTT sector is currently in the scaling stage with strong subscription growth and high investment in premium & original content. The sector is one of the most competitive amongst emerging markets with 40+ players representing all types of content providers. “Cord cutting” (cancelling TV subscription and moving to OTT) is in nascent stages and is expected to be limited in the medium term. Said Mandeep Kohli, Managing Director and Partner, Boston Consulting Group India: “The share of traditional media is slowly declining with increased digital adoption but there is still high headroom for penetration with only 54% of Indian households having a pay TV connection compared to more than 70% in China. For many households, TV continues to be the center of the home and a significant part of family time.”

As was the case with other industries, the past year has been a challenging one for the media and entertainment industry. However, the industry has shown remarkable recovery with TV ad volumes bouncing back to pre-COVID levels and expected to continue growing in the future, driven by increased advertising on regional channels & entry of new advertisers. AVOD is now one of the fastest growing ad segments in India driven by interactive ad formats, blending of content and ads and the rise of short form AVOD platforms.

One of the major themes in this year’s report is the industry’s anticipated transformation over the next decade. The Media and Entertainment industry is at a critical juncture of transformation, offering rapid growth in some areas. “To realise this growth, companies must tweak their strategies to take advantage of the current market situation. In addition to investing in content and technology to improve user experience, companies should also leverage suitable distribution models to enhance reach, focus on providing integrated ad solutions and offer innovative marketing formats to enhance the value proposition to advertisers,” explained Kanchan Samtani, Managing Director & Senior Partner, Boston Consulting Group India.

Setting the tone for the coming years, Madhavan added: “Our industry has always been at the forefront of disruption and we will continue to innovate over the next decade. We will now need new answers and will need them fast, even on the most fundamental things like talent pool to run our companies and methodology for measuring the impact we are delivering to advertisers on our platforms. We will need to continue to embrace change going forward to create the most value for consumers as well as our partners.”