By Ashoke Agarrwal

While the Metaverse is just a gleam (fading?) in Zuckerberg’s eyes and Large Language Models is the latest hot tech trend, the Gameverse has, over the past decades, changed, almost unnoticed, the media world.

While the Metaverse is just a gleam (fading?) in Zuckerberg’s eyes and Large Language Models is the latest hot tech trend, the Gameverse has, over the past decades, changed, almost unnoticed, the media world.

The numbers are impressive enough.

The forecast is that consumers will spend USD 185 billion globally on video games – five times more than they will spend on cinema and 70% more than what they will spend on TV streaming services like Netflix. The latest Harry Potter title, “Hogwart’s Legacy” – a video game – took in USD 850 million in two weeks. Gaming concepts are spawning TV and movie spin-offs- “The Last of Us” on HBO and the upcoming movie – “Tetris’ – on Apple TV. Increasingly powerful smartphones put gaming consoles in consumers’ pockets, increasing the time spent on games. Smart TVs, streaming and subscription libraries will further accelerate the growth of games. In 2022 3.2 billion people – four in ten worldwide played video games, rising by 100 million annually. Gaming occupies the entire engagement spectrum – from individual absorption to small and large group play to a mass spectator activity that is e-sports. E-sports is now among the big leagues of sport. For example, Riot Games sold the streaming rights of its Chinese league to Huya, a streaming service, for USD 310 million. The Asian Games in September will include digital games.

Besides the growing audience for professional e-sports, there is an equally large audience for user-generated gaming content. With its USD 30 billion ad revenue, YouTube says gaming is its second largest category after music. In addition, Twitch, a user-generated gaming content platform, has over half a million quarterly active streamers. Gaming-As-A-Service (GAAS) is a growing business model. “World of Warcraft” offers a subscription service with regular updates to maps, missions and characters. Grand Theft Auto has blockbuster sequels, and GTA Online offers continuously refreshed content at $6 a month.

What about gaming in India? In value terms, it is small but growing – USD 1.2 billion in 2020 and projected to grow at a CAGR of 26%. However, gaming’s reach in India is already high. Five hundred and ten million people played video games in India in 2022. 94% of Indian gamers use mobiles as their platform, 9% use PCs and 4% play on consoles.

Over the coming decades, will India leapfrog into being an advanced video game market? Perhaps, given the fast pace of technology diffusion as a society transits upwards economically.

Given the preferences of the young and its multi-directional growth, gaming will be the driver of a new media paradigm.

What about advertising in the Gameverse? Does it need a new paradigm?

Advertising strategy and grammar underwent a paradigm shift from the age of print to the age of radio and then TV. Over the last two decades, with the advent of search and social media, performance marketing has driven a seminal shift in advertising grammar. In addition, the age of generative AI will significantly impact advertising processes and economics.

If brands and their advertising are to harness the opportunity that gaming presents, they will have to resonate with gamers’ unique needs and motivations.

A 2020 book – Games: Agency As Art by C. Thi Nguyen – offers insight into why games engage people.

Games engage because they are a motivational inversion of life. In life, means are for the sake of ends; in games, ends are for the sake of means.

People play games because they offer them the chance to assume different roles within a given set of rules. The gamer plays to achieve a particular end, but the engagement and enjoyment are in the playing. The core motivation driving gaming engagement is that it offers the gamer an agency different from his real-life persona. This agency transformation is true not just for video games but even simple games like card games of poker or rummy. Many highly engaged players of these card games assume a game persona that is very different from the real persona. For example, a quiet man transforms into a chatty one at the card table, and a chatty one becomes the strong, silent type.

The highly creative and immersive worlds of modern video games multiply the agency that games offer to unprecedented levels.

The mediums of television, radio and advertising offer convenient spaces where advertising can insert itself without any connection or reference to the content it has interrupted. The creative challenge here is to overcome the irritation caused by the interruption. This challenge multiplied with the arrival of the multi-channel world and the remote control, but the core challenge and the response remained the same.

In the era of performance marketing, the creative challenge of overcoming the urge to ignore remains. However, the grammar has shifted with the arrival of performance marketing; the objective now is action – click a link – and not the amorphous building of brand awareness and equity.

In the Gameverse, interruption is not a challenge; it is taboo, given the intense nature of the engagement. Instead, the advertising’s challenge in the Gameverse is multi-fold:

:: An advertised brand needs to be present as an integral part of the gaming experience and not as an interruption.

:: The brand needs to allow the gamer to remain in their chosen persona.

:: Outside the game, the gamer’s interaction with the game continues by creating and watching user-generated content and e-sports events centred on that game. The brand can maximize its impact by a) enabling the gamer to generate content and b) enhancing the gamer’s experience as a spectator of e-sports or other user-generated content.

The path to profiting from advertising in the Gameverse is to choose a shortlist of games to focus on and build a 360-degree customized strategy for each game. The advertising strategy focused on a specific game that follows the tenet of going with the game’s flow can only be achieved in collaboration with the game creators. Therefore, good advertising within a game is not about buying space and time but about a creative partnership with the game’s creators.

For example, a brand could offer a bonus race in a specially branded car in a car-racing game. Red Bull has done so in some games.

The higher the degree of integration into the game, the greater the impact and, thus, the ROI for the advertiser’s brand. For example, a game-integrated brand could offer players a branded assistant who analyses, offers tips and gives pep talks. With advances in generative AI, such a strategy offers fascinating possibilities. Moreover, this assistant becomes a part of the content creation and e-sports-watching experience outside the game.

Is the Gamverse advertising opportunity category agnostic? TV, press and digital are product category agnostic in that advertising across product categories can be effective with the right creative and media strategy.

Given its unique characteristics, advertising in the Gameverse can be genuinely effective for categories and brands that, at the core, connote a persona and a lifestyle- fashion, personal accessories, cars etc.

The estimate is that in 2020 advertising in the Gameverse worldwide was USD 65 billion. By consensus, the most effective brand with its Gameverse advertising strategy is Red Bull, with a Gameverse budget of nearly USD 600 million. Red Bull’s core brand proposition is that it empowers its consumers – encapsulated in the theme “Red Bull Give You Wings”. This brand proposition resonates in the Gameverse, where the primary motivation driving Gamers is, as Ngyuven’s book proposes, to find a new persona, a new agency – a new set of wings.

To sum up, if your brand is considering the Gameverse as a medium for advertising, first make sure that there is a fit between your brand’s proposition and the essential motivation that drive gamers. The subsequent steps then consist of finding a suitable game or a concise list of games to focus on and building a partnership with the game developers to create a highly integrated brand presence in the game.

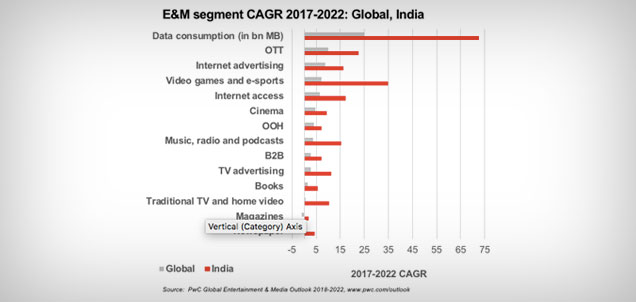

PWC’s 23rd annual Global Entertainment and Media Outlook released on June 23, 2022 shows that globally after a setback in 2020 due to the pandemic, the entertainment and media industry is set on a steady path of recovery with a CAGR of 4.6% during 2021-26 to reach a market size of US$ 2.9 trillion in 2026 as shown in the chart below.

PWC’s 23rd annual Global Entertainment and Media Outlook released on June 23, 2022 shows that globally after a setback in 2020 due to the pandemic, the entertainment and media industry is set on a steady path of recovery with a CAGR of 4.6% during 2021-26 to reach a market size of US$ 2.9 trillion in 2026 as shown in the chart below.

Anand Bhadkamkar, CEO, Dentsu Aegis Network India: “2019 was a challenging year for the Indian advertising industry as well. With the economic slowdown, advertisers decided to cut back on spends, consumers decided to wait-and-watch, market sentiments reached a new low and India’s Ad Expenditure (AdEx) witnessed a consequential fall. But even in the midst of it all, digital continued to grow. Digital is a masterstroke in advertising and Dentsu Aegis Network recognizes this strength. We also recognize the need for an industry level report that can give directions toward which this industry is moving. While with every new edition, the DAN Digital report has been upping its rank in quality, range and comprehensiveness, we welcome sincere feedback and inputs from the entire industry to help establish a robust eco-system for this fast growing and increasingly important industry channel, so that all of us can progress together!”

Anand Bhadkamkar, CEO, Dentsu Aegis Network India: “2019 was a challenging year for the Indian advertising industry as well. With the economic slowdown, advertisers decided to cut back on spends, consumers decided to wait-and-watch, market sentiments reached a new low and India’s Ad Expenditure (AdEx) witnessed a consequential fall. But even in the midst of it all, digital continued to grow. Digital is a masterstroke in advertising and Dentsu Aegis Network recognizes this strength. We also recognize the need for an industry level report that can give directions toward which this industry is moving. While with every new edition, the DAN Digital report has been upping its rank in quality, range and comprehensiveness, we welcome sincere feedback and inputs from the entire industry to help establish a robust eco-system for this fast growing and increasingly important industry channel, so that all of us can progress together!” Ashish Bhasin, CEO, APAC and Chairman, India – Dentsu Aegis Network: “The Media and Advertising industry is shifting at a rapid speed and Digital is certainly taking charge. Consumers are leaving behind huge digital footprints and there is a lot more emphasis on managing data and developing martech capabilities, now. 2020 is expected to witness a major change in advertising in India, with digital becoming a bigger medium. In fact, by 2021, it’s growth should surpass that of print. Yet, despite this progressive swing, the industry has failed to come together to agree upon a common measurement metric for digital. As leaders in digital, Dentsu Aegis Network today stands at the forefront of this evolution and understands the need to have more information on Digital. The DAN Digital report, now in its fourth edition, is exhaustive, systematic, thorough and meets this need gap brilliantly. The report has now become the most credible source of information when it comes to digital in India.”

Ashish Bhasin, CEO, APAC and Chairman, India – Dentsu Aegis Network: “The Media and Advertising industry is shifting at a rapid speed and Digital is certainly taking charge. Consumers are leaving behind huge digital footprints and there is a lot more emphasis on managing data and developing martech capabilities, now. 2020 is expected to witness a major change in advertising in India, with digital becoming a bigger medium. In fact, by 2021, it’s growth should surpass that of print. Yet, despite this progressive swing, the industry has failed to come together to agree upon a common measurement metric for digital. As leaders in digital, Dentsu Aegis Network today stands at the forefront of this evolution and understands the need to have more information on Digital. The DAN Digital report, now in its fourth edition, is exhaustive, systematic, thorough and meets this need gap brilliantly. The report has now become the most credible source of information when it comes to digital in India.”

Last weekend, Union minister Ravi Shankar Prasad gave a press statement, where he cited the combined first-day collections of War, Sye Raa Narsimha Reddy and Joker (Rs. 120 cr) to “prove” that there is no slowdown in the Indian economy. This comment, which can form a case study in a Logic 101 class on how not to construct an argument, has been the subject of many jokes and memes on social media over the last week.

Last weekend, Union minister Ravi Shankar Prasad gave a press statement, where he cited the combined first-day collections of War, Sye Raa Narsimha Reddy and Joker (Rs. 120 cr) to “prove” that there is no slowdown in the Indian economy. This comment, which can form a case study in a Logic 101 class on how not to construct an argument, has been the subject of many jokes and memes on social media over the last week.