By A Correspondent

India has emerged as one of the world’s fastest growing fashion markets over the years. Traditional brick-and-mortar brands are increasingly adopting digital channels for engaging with and selling to Indian consumers while maintaining their competitive positioning. In order to help these brands understand and eliminate reasons for consumer drop-outs in their path to purchase of apparel and fashion accessories, late last month, Facebook released the next installment of the research report under its Zero Friction Future programme titled “Eliminating friction in Fashion path to purchaseâ€. The third in the series, the reports are authored by KPMG, based on primary research and insights basis the survey conducted by Nielsen for various industry verticals, across different cities in India.

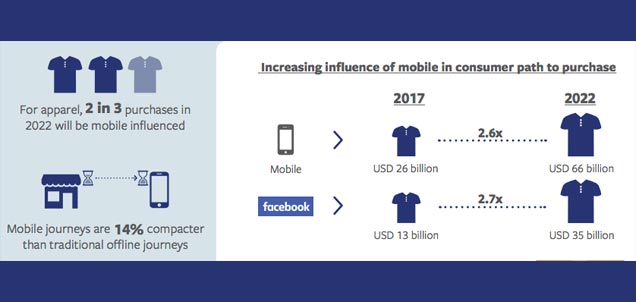

According to the findings of the report, friction accounts for 19% of consumer dropouts, in apparel category, and more than two-third of this friction is caused by media. In accessories category, friction accounts for 22% of consumer dropouts, and around two-third of this friction is caused by media. It further highlights that by 2022, seven in ten fashion accessory purchases in 2022 will be mobile influenced, nearly half of which will be driven by Facebook, amounting to a USD 110 billion sales opportunity. Additionally, mobile will influence two in three apparel purchases, amounting to USD 66 billion opportunity for brands, half of which will be driven by Facebook.

Commenting on the launch of the report, Pulkit Trivedi, Director, Facebook India, said: “Fashion spectrum in India has evolved so considerably, that the apparel and accessory market is projected to reach USD 102 billion and USD 155 billion individually, by the year 2022. Today, mobile has become central to the way brands market and sell their products and engage with customers end-to-end. With our Zero Friction Future report, we aim to help fashion brands adopt relevant marketing strategies and reduce friction in consumer journeys across multiple touch-points, leading to improved conversion rates and increased revenue opportunity.â€

The study reveals that mobile enabled purchase journey is 14% and 25% shorter than offline journeys of apparel and fashion accessories respectively. The friction faced by consumers can be reduced with the higher use of mobile in the media mix, creating ~USD 14 bn worth of potential revenue for fashion brands by 2022. It also suggests that mobile can reduce media friction by 3 percentage points for apparel category and 4 percentage points for accessories, allowing the brands to tap into ~USD 5 & 9 billion market opportunity respectively.

Speaking on the report findings, Sreedhar Prasad Partner & Head –E-Commerce and Internet, KPMG in India remarked: “The fashion consumption story of India is evolving and demand for quality fashion products is on the rise. This phenomenon is not limited to Tier 1 markets, but also Tier 2 and below towns, on account of growing per capita income, mass urbanization and increasing access to digital content. Rising affluence of the middle income group is creating demand for aspirational brands. In order to capture a larger share of mind, time and wallet of their target customers, fashion and e-commerce brands should continuously evaluate their marketing mix to ensure presence where the customer is. The report aims at exploring the customers’ path to purchase and associated friction throughout their journey.â€

Added Ashish Karnad, Executive Director – Marketing Effectiveness, Nielsen India: “We wanted to measure the influence and impact of media touch-points on consumers’ path to purchase route – right from the time they have a need to buy an apparel or fashion accessory, to finally buying it. We designed the study to get a zoomed-in view on how buyers are now interacting with various media touch-points. Unsurprisingly, mobile is playing a key influencer in the entire journey. While other touch points have their own roles to play in a buyer’s journey, Mobile helps in reducing friction at each stage. We hope this study will give a strategic view on the opportunities being missed by marketers due to media friction and bring in further optimization.â€

According to the research, top friction areas for different demographic cohorts vary and hence marketers need to customize their marketing strategy accordingly. Some key consumer friction areas across touch points include:

:: Gender based: Both men and women display different drivers for entering the purchase funnel. Men seek clear next steps after watch and advertisement. On the other hand, women are more susceptible to ignore ads if they fail to either capture their attention or provide relevant information. As they both ahead in the purchase journey, credible information and better ‘value for money’ become important decision making parameters for both men and women. While buying fashion accessories, women are more sensitive to price and lack of trust at point of sale. Men, however, are more likely to ignore an advertisement at top of the funnel, but seek lucrative offers and detailed information for evaluating their shortlisted products.

:: Age specific: 35-49 year old are more sensitive to inaccurate targeting of ads, or lack of clear call-to-action. However, younger age group of 18-24 year old have a higher propensity to drop-out at the intent stage. Highest friction is accessory purchase across age groups is observed at the top of the funnel. Across age groups, more than 1 in 3 consumers shopping at retail stores are likely to change their purchase decision. Consumers from all age groups discontent for lack of options to compare and choose from, lack of attractive offers and expectation mismatch at point of sale. This creates an opportunity for e-commerce players to deploy full-funnel marketing strategies by addressing these friction points. Brand’s communication strategy implemented in tandem with e-commerce strategy could capture leads at top of the funnel and facilitate their movement through the purchase funnel.

:: Socio-economic: Both NCCS A and NCCS B consumers display comparable tendency to enter and complete the apparel purchase journey. However, more than three fourth of prospects abandon apparel purchase at either awareness or intent stage. NCCS B consumers are more likely to abandon an accessory purchase after entering the purchase funnel as compared to NCCS A, and half as likely as NCCS A to transact online. Contextualization of content and call-to-action mechanism could extend the proposition of online medium to NCCS B consumers.

By Indrani Sen

By Indrani Sen

While increasing importance is being given to Hindi GECs and sports broadcasting in India, a genre that has been steadily pushing itself up the growth chain is children’s entertainment. Accounting for nearly 7 per cent of the growth pie, kids’ channels in India have been throwing up interesting growth trends over the past few years.

While increasing importance is being given to Hindi GECs and sports broadcasting in India, a genre that has been steadily pushing itself up the growth chain is children’s entertainment. Accounting for nearly 7 per cent of the growth pie, kids’ channels in India have been throwing up interesting growth trends over the past few years.