By Our Staff

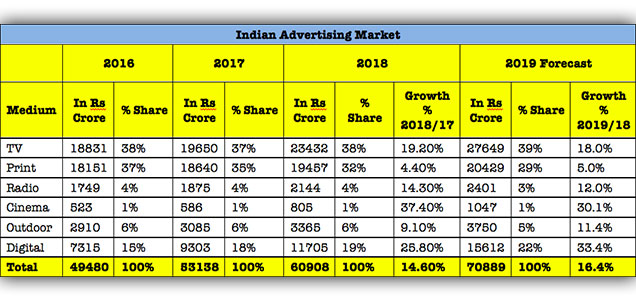

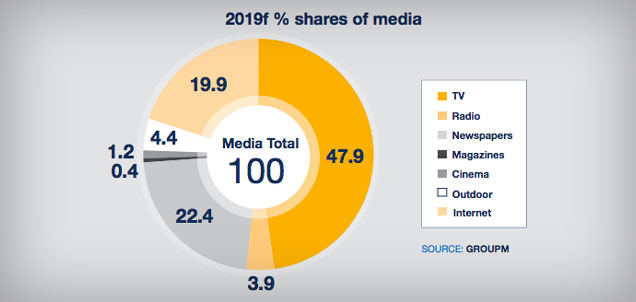

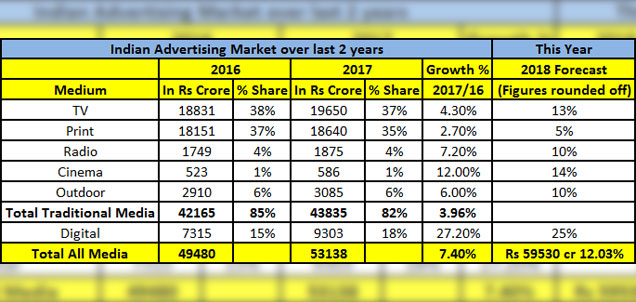

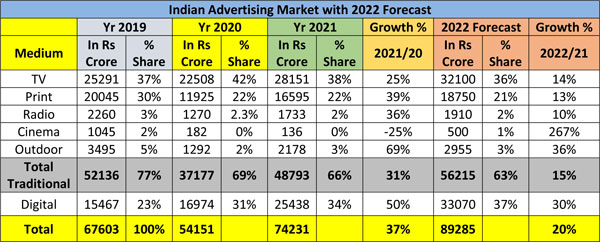

Madison Media predicts adspends (AdEx) will increase 20% in calendar year 2022. The highlights of the Pitch Madison report were released on Wednesday by Sam Balsara, Chairman, Madison World. According to Madison Media, AdEx is expected to grow by 20% in 2022 and reach Rs. 90,000 crore. This growth is on the back of a dramatic Rs. 20,000 crore increase in 2021 inspite of Covid wave 2. In 2021 Digital grew by 50% and in 2022 is expected to pip television to become the largest contributor to Adex with a share of 37%, compared to TV’s 36%. Print, too has grown dramatically by as much as 39%, retaining its share of 22% in Adex.

Said Sam Balsara, Chairman, Madison World, “Advertisers seem to be returning to advertising with a vengeance. After Covid year 2020, Global Adex has registered a whopping 21% growth in 2021 and 18% versus pre-covid 2019. Compare this with a compounded annual growth rate of just 5% over 10 years from 2010 to 2019. India infact leads this return, with a growth of 37%, compared to a last 10-year compounded annual growth rate of just 10.4%.”

Key findings of the Report:

1. Overall:

1 • In 2021 total Adex grew by 37%, Traditional Adex by 31% and Digital Adex by as much as 50%.

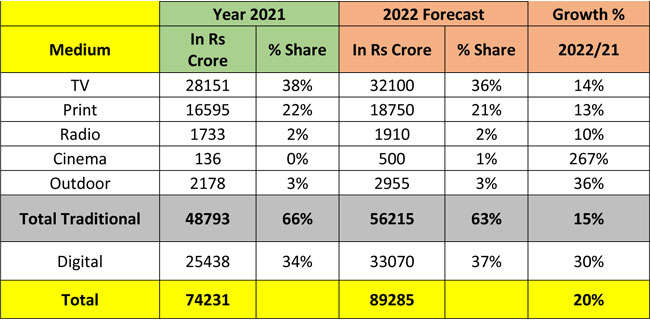

2 • In absolute terms, ADEX has grown from Rs. 54,151 crore to Rs. 74,231 crore and comfortably surpassed the 2019 figure of Rs. 67,603 crore by 10%.

3 • Traditional Media contributes 66% of total Adex, whereas the global figure is 35%. Despite a growth of 31% in 2021, Traditional Media at Rs. 48,793 crore, has not reached its 2019 figure of Rs. 52,136 crore.

4 • Digital Adex has now reached a share of 34% and is in striking distance of TV, the leader of the pack which ended the year with a share of 38%. TV and Digital Adex now account for 72% of Adex.

5 • Q3 and Q4 2020 contributed to 60% of Adex. Q4 registered a whopping 49% increase over Q4 2019.

6 • FMCG continues to be the main category, but its share moved down from 38% in 2020 to 34% in 2021.

7 • Ecommerce emerged as the 2ndbiggest category of Adex and the largest contributor to its growth, doubling in size from Rs. 3,000 crore to Rs. 6,000 crore.

8 • 15 new-age Companies / start-ups have entered our list of Top 50 advertisers namely, Dream 11, BYJU’s, Phone Pe, Upstox, My 11 Circle, CRED, Netmed, MPL, Policybazaar, Unacademy, WhiteHat Jr, Swiggy, Netflix, Coin Switch Kuber and Coin DCX.

2. Television

1 • TV registered a high growth of 25% to reach Rs. 28,151 crore, following a 11% de-growth in 2020. TV is the only traditional medium that has comfortably surpassed the 2019 number of Rs. 25,291 crore, by as much as 11%. TV’s market share is at 38%, down from a high of 42% last year but one percentage point higher than 2019.

2 • TV Adexwitnessed a 25% spike in Ad volume or FCT in 2021 over 2020 and a 11% increase against 2019. Significantly ad volume in 2021 is higher than 2020 in all four quarters.

3 • FMCG continues to be the largest contributor to TV Adex with a share of 46%, but lost as much as five percentage points from a high of 51% in 2020. Ecommerce, the 2ndlargest contributor to TV Adex, increased its share from 11% to 18%, followed by Edtech which increased its share from 4% to 6%.

4 • News as a genre has registered a high growth of 19% over 2019 and 29% over 2020. Marathi and Tamil Regionals have also grown dramatically by 36% and 24% respectively over 2019. Second line GECs de-grew by a massive 18% and mainline GECs de-grew by a negligible 3%. Hindi GEC continues to be the largest segment, followed by Sports and then News.

5 • TV Adex is expected to grow by 14% in 2022 to reach Rs. 32,100 crore, 27% higher than 2019.

3. Digital

1 • Digital grows by 50% in 2021 to reach Rs. 25,438 crore and has emerged as a strong No 2 for the 2ndconsecutive year, at 34% share, a little short of TV at 38%. Digital has achieved a CAGR of 27% over last 10 years.

2 • Q4 was the largest quarter, where Digital Adex touched almost Rs. 10,000 crore and contributed 39% to the full year.

3 • Video is the highest contributor to Digital with a share of 29%, followed by Social & Display at 20% each. E-commerce and Search now contribute 16% each to overall digital pie. In terms of growth rate, E-commerce has grown significantly by as much as 50%. Display, Video and Search have also grown substantially at 30%+.

4 • Programmatic has firmly taken route in India and its share continues to be 42%.

5 • Ecommerce advertising revenue is rising rapidly and we estimate ecommerce advertising spends in 2021 to be at Rs. 4,100 crore, mainly on the back of Amazon and Flipkart, but newer entrants like Nykaa, Big Basket and JioMart are also finding favour with a relevant set of advertisers.

6 • Digital is set to grow by 30% in 2022 to reach Rs. 33,070 crore and set to emerge as the single largest contributor to Adex, overtaking TV by almost a 1000 crores.

4. Print

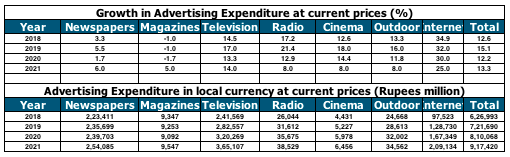

1 • Following a 41% decline in 2020, Print Adex grew by a whopping 39% to reach Rs. 16,595 crore. Despite the high growth rate, Print is still only at its 2015 levels and has registered a 16% drop vs 2019.

2 • With a share of 22% in Adex, India is the Print Capital of the world, along with Germany. Global share of Print is a mere 5%.

3 • Print volume in terms of CC has also gone up by 31%.

4 • 3 categories FMCG, Education and Auto make up 45% of total Print Adex. Both FMCG and Auto have come down in share by 2 percentage points each.

5 • English and Hindi publications put together, contribute to 63% of total Adex volume. English publications grew 40% over 2020. Hindi publications which are the largest volume contributor, also grew by 30%, Telugu by 37%, Assamese & Marathi by 33% and Bengali by 27%. All languages grew, the least to have grown are Kannada, Gujarati and Punjabi by 18-19%.

6 • Print Adex is expected to grow by 13% in 2022 to reach Rs. 18,750 crore, but it will still be at the level it reached in 2017.

5. Other Media

1 • OOH Adex has registered a high growth of 69%, taking the industry to Rs. 2,178 crore, but still way below 2019 level. Conventional OOH grew by 63% and Transit Outdoor by almost 100%. Digital OOH is also beginning to take root and grew from Rs. 50 crore to Rs 300 crore and has a share of 13.77%, far below the global average of 40%. We expect OOH Adex to grow by 36%, to reach Rs. 3,000 crore, the level it had reached in 2017.

2 • Radio Adex has grown by 36% to reach Rs. 1,733 crore, with a share of just 2 %. With this Radio is at the level it had reached in 2016. We expect Radio Adex to grow by 10% and reach Rs. 1,900 crore.

3 • Cinema has been by far the worst affected medium. Because of 2 years of Covid, it has degrown by a further 25% over 2020 to reach 136 crores. We expect Cinema to grow by 267% to reach Rs. 500 crore, almost half of the pre Covid level of Rs. 1050 crore.

Figures at a glance:

By Indrani Sen

By Indrani Sen